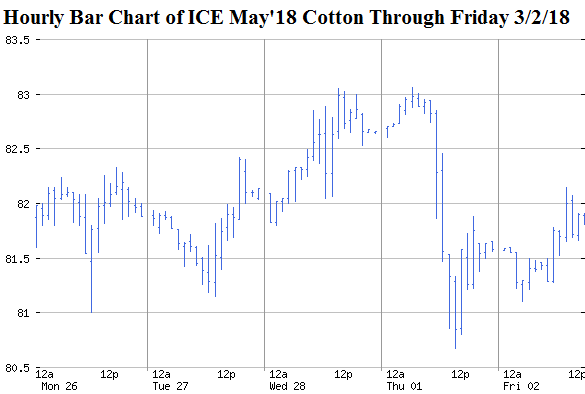

The week ending March 2 saw most active ICE cotton futures trade sideways on Monday-Tuesday, climb a cent on Wednesday, dip two cents on Thursday, before stabilizing at week’s ends. Trading this week continued in above average volume and a slight uptick in open interest, i.e., a reversal of the liquidation seen in mid-February. The latter was also evident from a rebuilding of the hedge fund net long position, week over week. Fundamental news this week included continued lower (but still good) export sales, week over week, reflecting the expected price-quantity demand relationship. Other outside financial news included announced U.S. tariff’s on foreign steel and aluminum that was associated with Thursday’s decline in ICE cotton futures as well as a general risk-off reaction for U.S. stock and and the U.S. dollar.

Mar’18 cotton on the ICE settled the week at 82.72 cents per pound. The May’18 and Jul’18 contracts settled 63 points and 35 points lower, respectively, on Friday. These futures spreads are obviously not covering the cost of storing cotton, e.g., Jul’18 would need to exceed May’18 by at least 150 points, and Friday’s spread was one sixth of that. There remains no strong market signal to store 2017 bales in hopes of higher prices, except for contingency purposes (what an egghead economist would call “convenience yield”).

The old crop contracts remained inverted above Dec’18 which settled at 77.05 cents per pound on Friday March 2. Chinese and world cotton prices futures were mixed this week.

A sample of option prices on ICE cotton futures saw some changes from the previous week because of the rise in the underlying futures. On Thursday March 1, in-the-money 73 call options on Jul’18 ICE futures were worth 9.66 cents per pound; lesser-in-the-money 79 calls on Jul’18 were worth 5.21 cents. A near-the-money 75 put option on Dec’18 cotton cost 3.28 cents per pound on Thursday, while deeply out-of-the-money 65 put on Dec’18 cost 0.61 cents.

This market is being supported by continued speculative buying a continuing good demand, as evidenced by the strong pace of U.S. export commitments and large mill fixations. But there is also a risk to see futures weaken further if the remnant of hedge fund longs get spooked by some risk-off event, and/or if seasonally high U.S. exports turn out to be more of a front-loaded pattern of what USDA has already been expecting. Remember, the current fundamental picture painted by USDA still implies price weakness by virtue of a large year-over-year increase in ending stocks. In the short run, the potential for a price reversal is also there because of the fickle fuel of speculative buying that underlies the rally since November.

Given all these uncertainties, growers should consider taking advantage of present (or future) rallies, and protect themselves from sudden sell-offs. Forward contracting, immediate post-harvest contracting, and/or various options strategies can be used to limit downside risk while retaining upside potential. In hindsight, contracted 2017 bales could have been combined with call options on the deferred futures contracts. New crop put spread strategies to hedge the 2018 crop are a straightforward approach. I have also heard of bale and acre forward cash contracts being offered in West Texas on competitive sounding terms, e.g., 2.5 cents and 3.5 cents off Dec’18, respectively. While similarly competitive to early 2017, I understand the discounts for low micronaire are higher in these recent offerings.

Source: The Cotton Marketing Planner