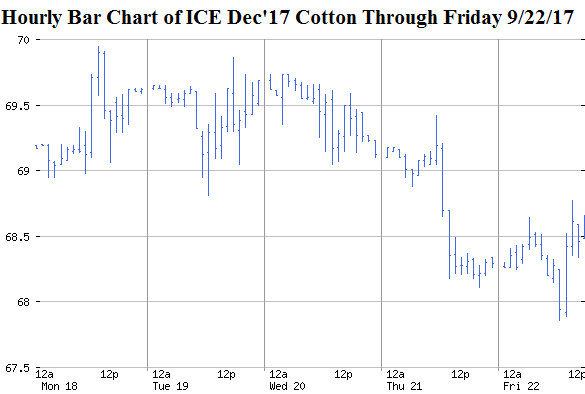

The week ending September 22 saw continued weakness in ICE cotton futures. The Dec’17 contract traded in a tight range above 69 cents through Thursday morning before downshifting a cent and recovering slightly at week’s end. The fundamental news this week included strong export sales, ideally warm weather for cotton maturation, some preliminary damage estimates from Hurricane Irma (also reflected in NASS’s condition ratings for Georgia), and possibly the non-event of Hurricane Maria. A mid-week rally in the U.S. dollar may have been a catalyst to the slide in cotton futures, as well as the modest recovery at week’s end. Dec’17 ICE cotton futures settled the week at 68.46 cents per pound. This level represents a continued inversion over Dec’18 cotton which has narrowed from 3.59 to 1.06 to 0.67 cents per pound over the last three weeks. In-the-money 73 put options on Dec’17 cost 5.16 cents per pound, while a higher 75 put was 6.90 cents per pound on Friday. Near-the-money 66 and 67 strike Dec. puts cost 0.96 and 1.32 cents per pound, respectively, on Friday. Out-of-the-money 73 call options on Jul’17 ICE futures cost 2.36 cents per pound on Friday; a further out-of-the-money 79 call on Jul’18 cost 1.29 cents per pound on Friday.

With the post-Hurricane Harvey rally, we may have seen the last opportunity for futures over 70 cents. There may, however, be a greater risk within six months to see futures under 60 cents. But since that is all uncertain, growers should remain poised and ready to take advantage of unexpected rallies, and protect themselves from sudden sell-offs. Forward contracting and/or various options strategies can be used to limit downside risk while retaining upside potential. Physical bales that have been forward contracted or recently sold post-harvest could also be combined with call options on the deferred futures contracts.

Source: The Cotton Marketing Planner