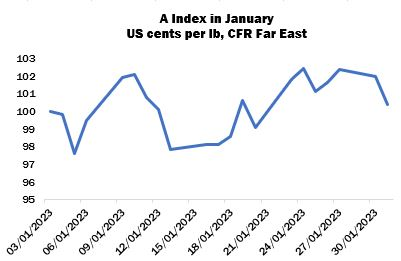

International cotton prices, as measured by the Cotlook A Index, moved either side of the dollar mark in January. Movements were on occasion volatile, in reflection of changes in the ICE futures market, which nonetheless remained within the range established in early November. The Index’s low point of 97.6 US cents per lb was recorded on January 5, while a high point (102.45) was reached almost three weeks later. The price ended January on a weaker note, to close just 40 cent points above its opening level.

The slightly more active level of mill enquiry that emerged in late 2022 continued throughout most of January, though any optimism prompted by the improvement in demand was tempered by the acknowledgement that business was generally only possible either at discounted rates, or at the lower end of the prices in circulation. In consequence, shippers’ basis levels showed a downward bias throughout the month. Mills also continued to concentrate primarily on their nearby requirements, with few exhibiting the confidence required to make additions to their forward commitments.

In those markets experiencing a shortage of US dollars, most notably Pakistan and Bangladesh, the execution of import contracts remained a source of frustration to both mill buyers and trade sellers. Energy supplies were also a worry, particularly in the latter country, where a government announcement confirmed a further rise in the cost of gas from February 1 that was met with dismay from the cotton and textiles industry. The volume of business concluded on the Indian subcontinent was therefore limited.

In Egypt, too, the need to generate dollars prompted some aggressive reductions in export offers, in the face of poor demand from the customary destinations. Cotlook’s Giza 94 quotation was reduced substantially as reports surfaced of business considerably below the levels previously in force.

Nevertheless, some spinners in the Far East showed a greater willingness to make purchasing decisions ahead of the Lunar New Year holiday (beginning January 22), ostensibly to ensure the continuity of their supply following return from the break at the end of the month, as well as in response to a tentative broadening of demand for cotton yarn that many hoped would continue to show improvement in February and beyond.

Meanwhile a modest revival of demand from Chinese buyers, who had earlier been virtually absent from the international market, engendered further optimism in international trade circles. Reports surfaced that importers in the country were showing interest in overseas origins to a greater degree than had been witnessed for some time.

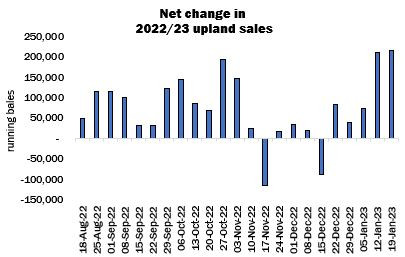

That optimism was consolidated somewhat by the United States’ export sales reports released in the second half of January, which represented the greatest weekly increases in the season so far. The aggregate addition to the upland sales figure during the two-week period in question was over 420,000 running bales, over half of which were destined to China. The total (upland and Pima) commitment stood by the end of January at around 9.4 million bales, equivalent to roughly 80 percent of USDA’s forecast for the season (reduced to 12 million statistical bales in the latest WASDE report).

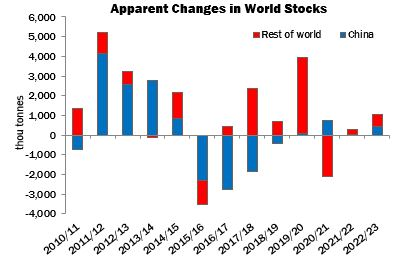

Cotlook’s forecast of world cotton production during the 2022/23 season was reduced only modestly on the month, to stand at 24,862,000 tonnes, but some major changes were made for individual countries. In China, reports of very good yields contributed to a significant increase, while our number for the United States was also raised, to bring it in line with the latest estimate released by the Department of Agriculture. Conversely, doubts persisted over the eventual size of the Indian crop as seed cotton arrivals remained well behind the pace of previous years. A reduction was made to our estimate for that country, and to our assessment of collective output in the African Franc Zone, where severe insect pressures and erratic availability of inputs have impacted yields.

On the consumption front, only one adjustment was made during January, as the figure for China was raised by 200,000 tonnes, bringing our global number to 24,723,000 tonnes (indicating a decline of 3.6 percent from the 2021/22 season). The recent lifting of Covid restrictions in China was credited for an uptick in yarn orders and market sentiment showed a considerable improvement, with operating rates increasing and inventories being depleted.

As a result of the above changes, world stocks are forecast to increase by 1,023,000 tonnes by the end of the current season, down from 1,258,000 put forward at the end of December.

Planting intentions for 2023/24 will come into sharper focus over the coming months, and Cotlook’s initial forecast of world production and consumption next season will be published in the February 23 issue of Cotton Outlook.

Source: Cotton Outlook