The cotton market picture keeps changing, but you wouldn’t know it from the March WASDE report from USDA. Looking at the world numbers, the old crop balance sheet saw modest tightening compared to USDA’s February forecast. The main source of these adjustments was in India. USDA increased historical Indian consumption by 0.5M bales (19/20) and 1.5M bales (20/21), while lowering subsequent carry-in accordingly. Old crop Indian production was lowered by a half-million bales, which was partly offset by a 150,000-bale increase in Mexican production. Lastly, Indian exports were lowered by 200,000 bales, as were Brazil’s. Those two big cuts were partially offset by a bunch of small month-over-month increases in a handful of other exporting countries. The net effect on world exports was a 180,000 bale decrease in world exports, which was almost matched by a 160,000 bale decrease in world imports compared to last month. The only category not impacted by Indian revisions was old crop world domestic consumption, which was raised a modest 111,000 bales, month over month. The bottom line of all these world adjustments was a 1.74M bale reduction in world ending stocks.

The March WASDE left the U.S. old crop supply and demand forecasts unchanged from the previous month. For what it is worth, the pre-report trade guesses were only looking for small changes in U.S. ending stocks. It was not surprising to me to see no change on the supply side. The outlook for the U.S. export category depended on whether one thought that the recent export shipment recovery was sustainable.

However, such early-season forecasts are always subject to late-breaking weather or price developments, of which we have both in abundance. The drought conditions have been spreading, and the official projected cotton prices for crop insurance are historically high.

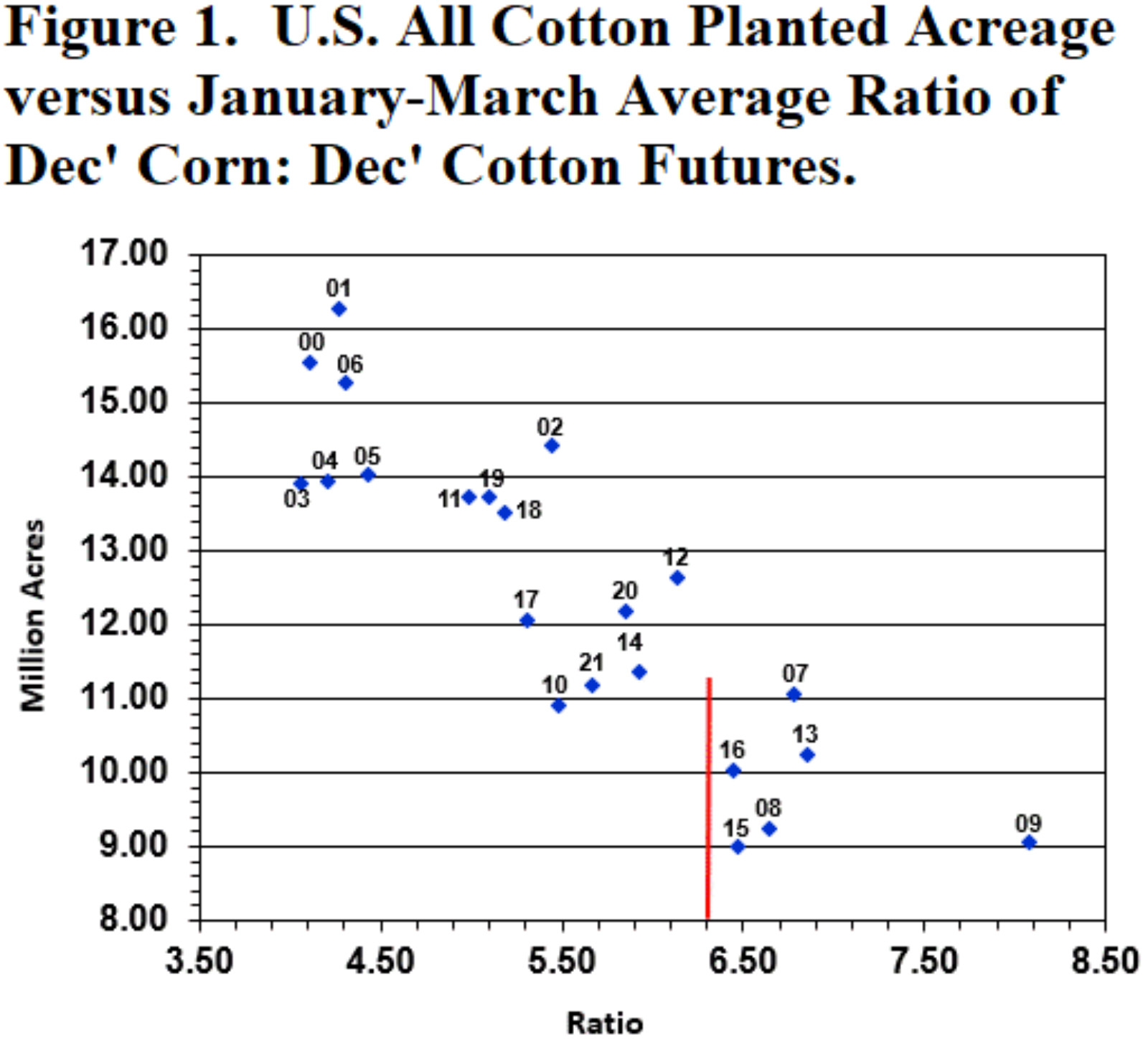

And with international events spurring grain prices, the corn-to-cotton price ratio has risen from 5.7 to 6.3 (see Figure 1 below). This higher price ratio implies a downshift in predicted cotton plantings, down into the 11-to-12-million-acre range.

To this new, lower baseline of planted acreage, I would tack on 500,000 to 750,000 more acres in the southern plains as a drought effect. That tightens up the new crop balance sheet and could support prices even more, while feeding the in-season weather market lasting through the summer.

UPDATE: With USDA’s Prospective Plantings at 12.2 million acres, this fits a scenario of a lower baseline plus the extra drought-effect acreage.

For additional thoughts on these and other cotton marketing topics, please visit my weekly on-line newsletter at http://agrilife.org/cottonmarketing/.

Source: farmprogress.com