Executive Summary

Highlights from the June 2022 Cotton This Month include:

- With two months left in the 2021/22 season, cotton consumption has overtaken and exceeded production

- Global area for the 2022/23 season is estimated to decrease by 1% to 32.78 million hectares

- Global production for the 2022/23 season is projected to be 26.13 million tonnes

- Global consumption for the 2022/23 season is currently projected at 26.09 million tonnes

- Prices will be influenced by multiple, hard-to-predict events including governmental policies

Cotton Production and Consumption Invert as the Season Comes to a Close

Decreases in the crop size of some top cotton-producing countries — including India, Argentina and South Africa — have resulted in consumption outpacing production as the 2021/22 season comes to a close. They were closely aligned through most of the year but given these smaller-than-expected crops, consumption is expected to exceed production by about 265,000 tonnes.

As the 2021/22 season comes to a close:

- Global area is estimated to decrease by 1% to 32.78 million hectares

- Global production is projected to be 26.13 million tonnes

- Global consumption season is currently projected at 26.09 million tonnes

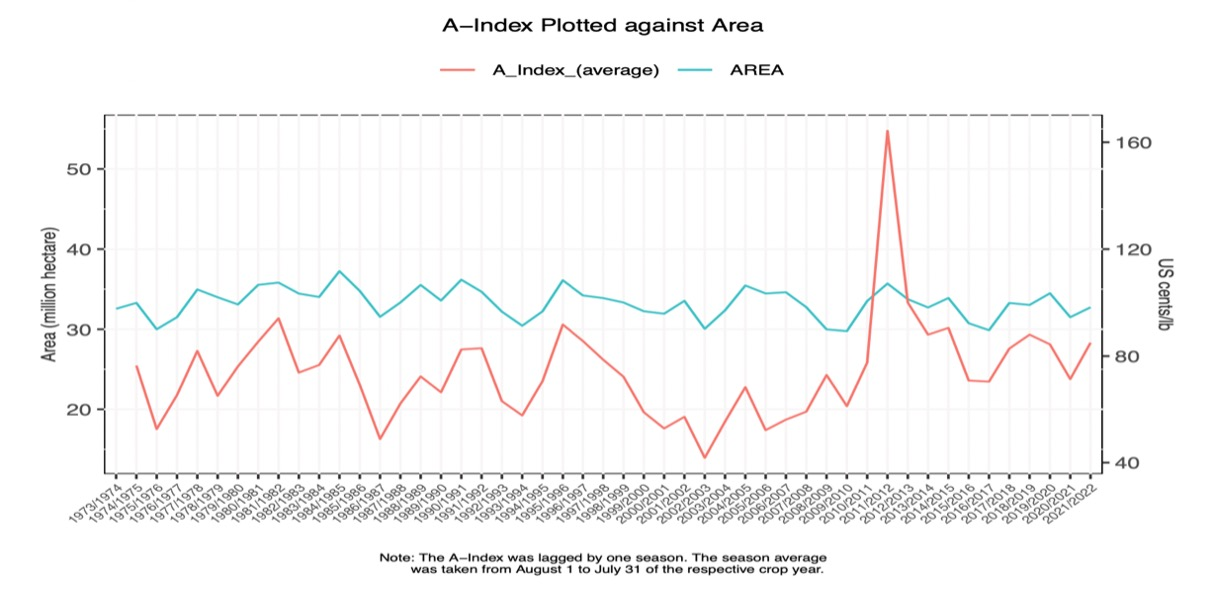

To asses the impact of those figures on prices, the stocks-to-use ratio — which measures the available cotton stocks as a share of cotton mill use — can help quantify the relationship between cotton supply and demand. When supply is tight compared to demand, the ratio is lower. A lower stocks-to-use ratio could indicate higher prices. In contrast, when supply exceeds demand then the ratio increases putting downward pressure on cotton prices. Planted area also can have a major impact on prices, as shown in the graph below:

Given so many variables and unknowns, the Secretariat is temporarily suspending publication of the price projections. We will reevaluate the price situation in August and determine if we should resume price forecast projection modelling. High volatility and extenuating circumstances in global markets make it difficult for any modelling framework to produce accurate and useful information. Please note that this is only a temporary pause and as soon as we are confident in the model data we will release projections. From a historical perspective, the only other time the price model was suspended was during the 2010/11 season of unprecedented high price and volatility. -