Written by Darin Newsom for Barchart

- These days, I find it easier to talk about commodities in terms of long-term investment potential given investors see the value in a bear market.

- That being said, Dec24 cotton may have posted a seasonal low, a move that could lead to a long-term change in trend.

- One of the more bullish factors is the recent increase in the noncommercial net-short futures position, opening the door to a round of short-covering over the coming weeks and months.

The older I get, the more I look at commodities as investment opportunities rather than through the rose-colored glasses commonly associated with hedging and production agriculture. As I’ve said many times across the various venues, if you want to be “popular” in this industry, you have to say everything is always bullish, even when it isn’t. That isn’t the case when talking to global investors as they are interested in one thing and one thing only: Making money. It doesn’t matter if this comes from being long or short, as the investment side understands one can make a good deal of money, faster (usually), in a bearish market. With that in mind, I want to take an updated look at Cotton.

Any time the subject of cotton comes up I’m reminded of a speaking engagement I had many years ago in southeast Texas. My hosts were a cotton cooperative and provided me a tour of their cotton gins and storage fields. Coming from a grain cooperative background and having spent most of my career talking about corn, soybeans, and wheat, I found the tour fascinating. The fact my trip occurred less than a year after a major hurricane hit the area made it that much more interesting.

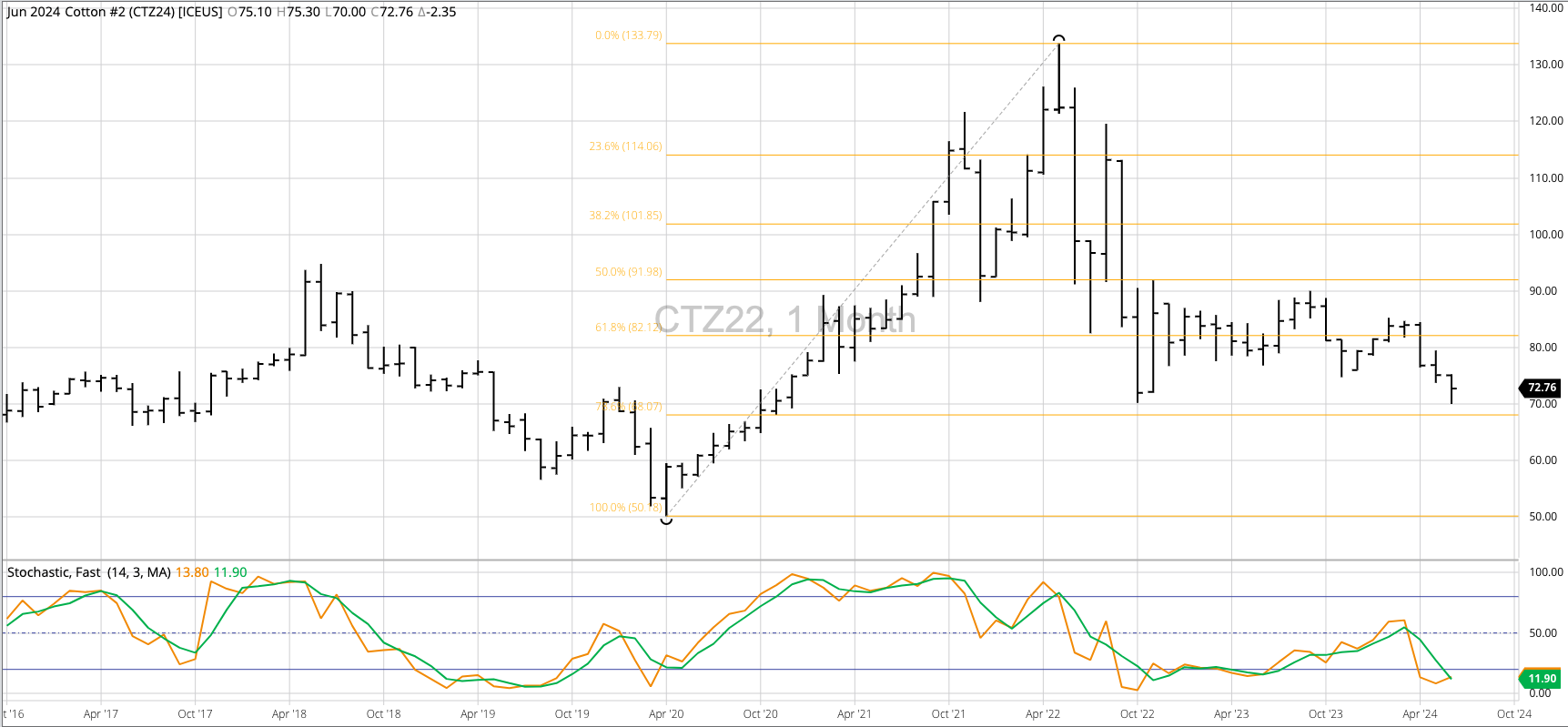

Last time, back in March, I talked about the usual list of market factors I track, starting with trend (price direction over time). Looking at the market as a long-term investor, the price chart I’m most interested in is the continuous monthly for the December futures contract only[i]. As we turn the corner into late June, the December 2024 contract (CTZ24) still looks to be in a long-term sideways-to-down trend. This month has seen Dec24 post a new major low of 70.00, taking out its previous mark of 70.21 (October 2022) before rallying to close Tuesday at 72.76. If Dec24 is to post a bullish reversal this month, one of the key steps is to close back above its May settlement of 75.11.

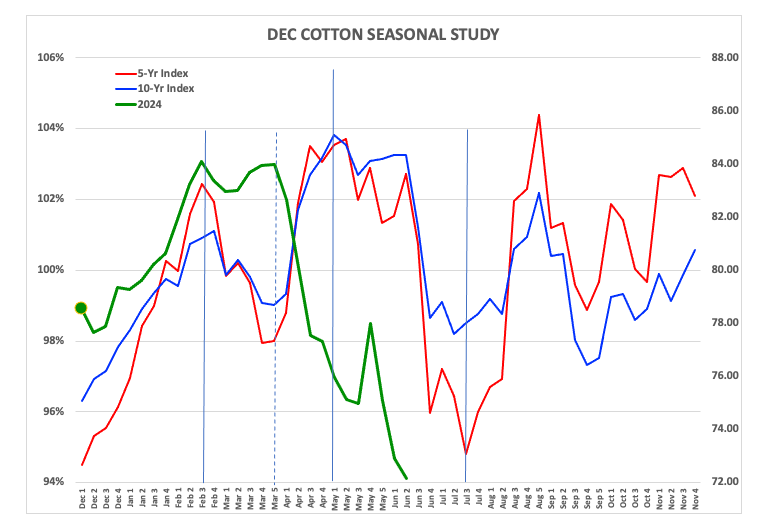

Seasonally, should we expect this to happen? Dec cotton’s seasonal tendency is to fall from the first weekly close of May through the third weekly close of July, losing an average of 9% in the process. Dec24 posted a high weekly close of 83.99 the last week of March and has since seen its value decrease by 14% through last Friday’s settlement of 72.14. Here’s where seasonal analysis gets fun: The Dec24 issue has traveled more than the average distance (14% versus 9%) over the same amount of time (12 weeks), just earlier than it normally does. This tells us Dec24 could be nearing its seasonal low.

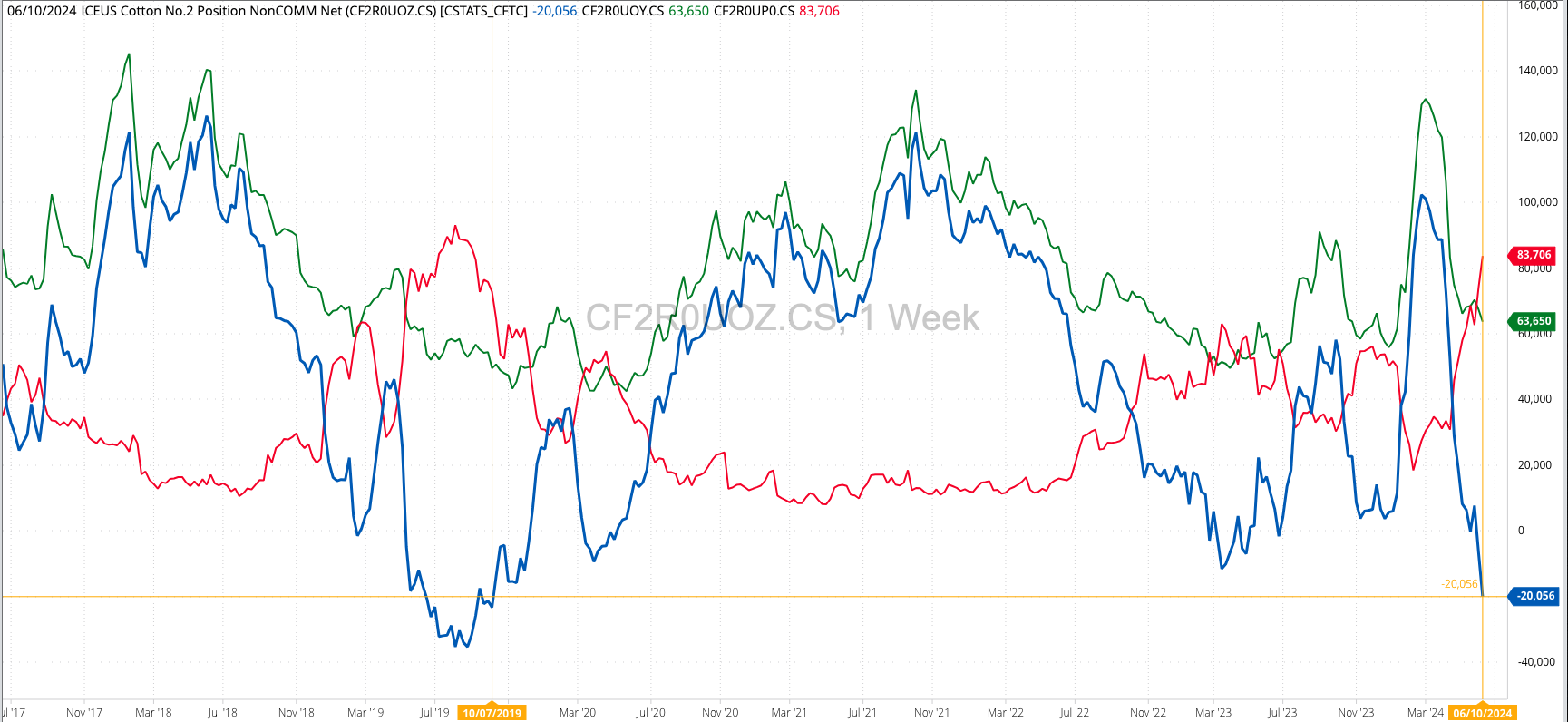

- What about market fundamentals? The December-March futures spread continues to show a carry, closing Tuesday at 1.29 cents. This was unchanged from last Friday’s settlement, which itself was weaker than the previous Friday’s close of 1.75 cents carry. Generally speaking, the Dec-March spread is indicating commercial traders are providing support, but I don’t know if we can call long-term fundamentals “bullish” yet. On the other hand, the noncommercial side added 13,365 contracts to their net-short futures position, as of Tuesday, June 11, putting it at 20,056 contracts. This was the largest noncommercial net-short futures position since 23,316 contracts the week of October 8, 2019. This tells us if the commercial side continues to buy, the potential for a noncommercial short-covering led rally grows stronger.

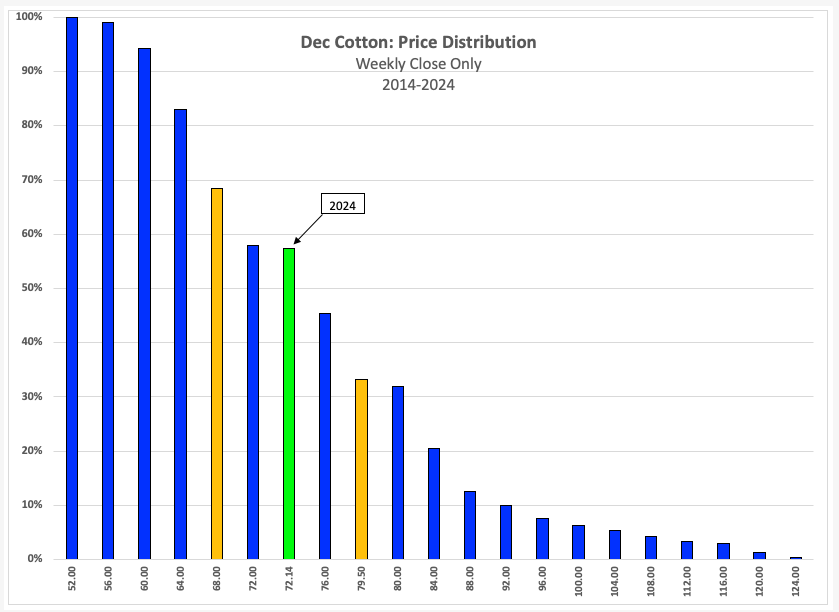

Is there a price incentive for funds to start covering short futures and possibly go long, long-term? At last Friday’s close of 72.14, Dec24 was priced in the lower 43% of its 10-year distribution range[ii]. This could still be viewed as neutral but getting closer to the bullish threshold at the lower 33% price near 68.00. Additionally, implied volatility for Dec24 was still high, running above 22%, so long-term investors familiar with the Speedo Situation[iii] may have sold Dec24 72.00 puts for 4.0 cents or more as this week got rolling. If these positions eventually get exercised, then these same investment traders would theoretically have long futures positions near 68.00. These would likely offset long-term short futures, possibly held since the close of May 2022, or establish a new long-term long futures position which would then be rolled to Dec25 (CTZ25).

Let’s see how this plays out.

[i] You may recognize this type of analysis as I do the same thing for long-term investment in corn, using the December futures contract only.

[ii] Based on weekly closes only for December futures.

[iii] Being short options isn’t right for everyone.