John Robinson, Extension economist, cotton marketing

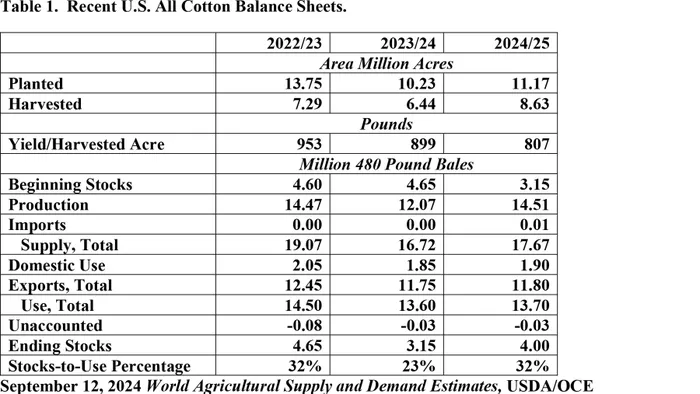

USDA’s September WASDE showed mixed adjustments to the 2024/25 U.S. cotton balance sheet compared to the prior month (third column of numbers in Table 1 below). Beginning stocks were unchanged, as were 2024 planted and harvested acres. Thus, the abandonment rate remained at 22%.

However, USDA cut yield per harvested acre from 840 in August to 807 pounds in September. This resulted in a 596,000-bale reduction in forecasted U.S. production, month over month. This reduction was spread over nine states, led by Texas (-404,000), Georgia (-100,000) and Oklahoma (-80,000). On the demand side, U.S. exports were cut two million bales, month over month, because of fewer exportable surpluses.

The bottom line of these mixed adjustments was a net 500,000 cut in U.S. ending stocks, to 4.0 million. The monthly adjustment would historically be modestly price supportive while the resulting level is probably neutral.

Similarly, USDA’s month-over-month adjustments in the September WASDE report reflected more tightening of 2024/25 world cotton balance sheet. On the supply side, beginning stocks were cut 170,000 bales, mostly in India (-400,000), and partially offset by Pakistan (+200,000). World production was lowered 1.2 million bales, mostly in the U.S. (-600,000), India (-500,000) and West Africa (-110,000), and partially offset by China (+300,000).

The world imports categories continued to be cut with 640,000 fewer bales compared to last month, mostly in China (-500,000) and Vietnam (-200,000), and partially offset by India (+300,000).

On the demand side, world exports were reduced by 550,000 bales month over month, mostly in the U.S. (-200,000), India (-200,000), and West Africa (-130,000). World domestic use was also cut 460,000 bales, month over month, mostly in Vietnam (-200,000), Turkey (-100,000) and Bangladesh (-100,000).

The supply side cuts of roughly two million bales dominated the roughly million bale reduction in demand, resulting in a 1.12 bale reduction in world-ending stocks, which is historically bullish in both the adjustment and the resulting level.

For additional thoughts on these and other cotton marketing topics, please visit my weekly on-line newsletter at http://agrilife.org/cottonmarketing/.