May 13, 2022

- Inflation Readings are Still Coming in Above Expectations

- U.S. Export Sales Finally Seemed to Slow Down

- May WASDE Report Released

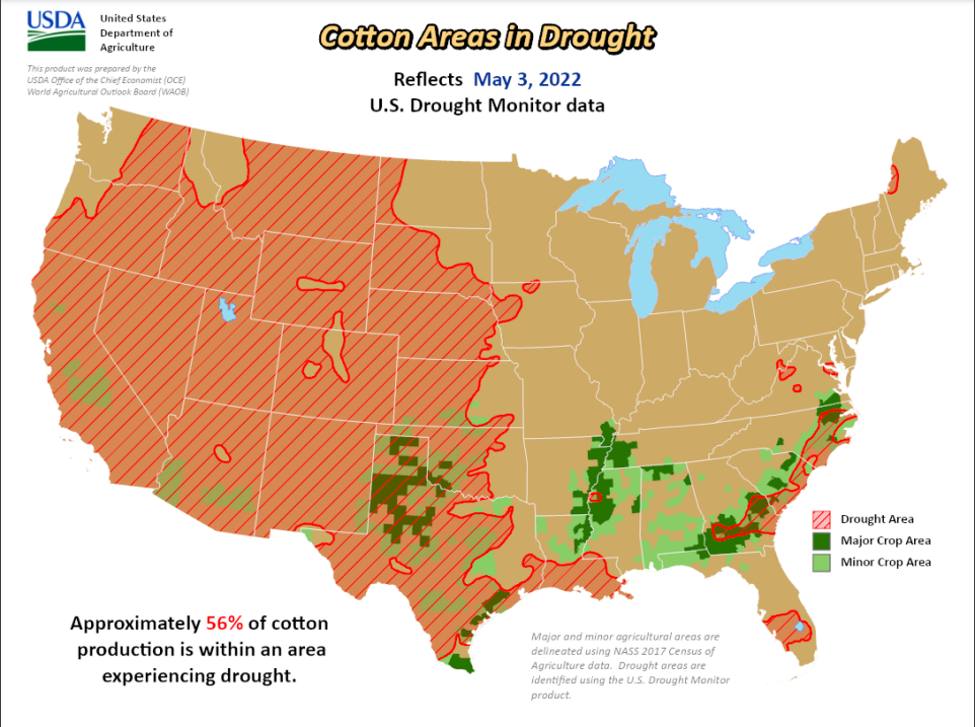

- While Precipitation was Helpful, Drought Conditions Still Continue to Prevail

July futures continued to move lower last Friday and on Monday, but seemed to find support on Tuesday and were able to recoup some of the week’s losses from there. The nearby contract settled at 145.53 cents per pound on Thursday, down 323 points for the week. December futures followed July’s pattern but were able to find support earlier and make a full recovery. December settled at 127.67 cents Thursday, up 123 points for the week and at its second-highest life-of-contract close. Trading volumes were on the lower end of normal for the past few months, and open interest declined 4,573 contracts to 202,762.

Outside Markets

Markets have continued to grapple with the most abrupt shift from loosening to tightening money supply perhaps ever. Despite some month-over-month deceleration, inflation readings are still coming in above expectations and there is no sign of a slowdown in the jobs market. Overheated prices give the Fed even more leeway to continue their tightening policy, which means that interest rates are set to continue rising for quite some time. Assets that were attractive in zero-yield environments such as technology start-ups and cryptocurrencies have been some of the largest losers. Bitcoin, for example, has fallen 57% from its recent highs and it is not the worst performer either. The flight to safety continues and the USD Index continues to touch fresh 20-year highs. Although the U.S. Dollar strength is usually a major headwind for commodities, the genuine shortage of many agricultural goods has kept prices from falling from the last few months’ highs.

Export Sales

It is hard to tell whether it is high prices or a lack of supply that did it, but U.S. Export Sales finally seemed to slow down for the current marketing year. For the week ending May 5, U.S. shippers made net new sales of just 27,500 bales. India bought the lion’s share of that at 19,800 bales. New crop sales were more encouraging with global mills booking 90,600 bales of Upland. Large buyers included El Salvador (28,400 bales) and Guatemala (25,300). Shipments continued at a healthy pace, totaling 372,800 bales of Upland and Pima combined.

WASDE

The May WASDE report gave markets the first glance at the USDA’s base case for the 2022/2023 marketing year in addition to updating the 2021/2022 balance sheet. There was little change to the US side of the 2021/2022 balance sheet. The outgoing crop was reduced 100,000 bales which were in turn removed from the ending stocks because the USDA made no revisions to its expected exports (14.5 million bales). The U.S. 2022/2023 balance sheet is therefore expected to have a carry-in of 3.4 million bales. The initial production guess was 16.5 million bales, based on Prospective Plantings acreage, 5-year average yields, 10-year average abandonment, and an adjustment to Southwest abandonment because of the drought. With world demand expected to remain high next season, the USDA started its export and use estimates at 14.5 and 2.5 million, roughly matching this year’s disappearance. The end result is 2.9 million bales of U.S. ending stocks, which is just 17% of the total use (Domestic Consumption plus Exports). Needless to say, the outlook is tight and every bale is needed.

The world balance sheet for 2021/2022 was actually loosened slightly. A large decrease to the Indian crop estimate was offset by several cuts to consumption, the largest of which was within China where the economy is dragging from heightened regulations and anti-pandemic lockdowns. For the 2022/2023 balance sheet, the USDA expected world production to rise to 121.06 million bales vs 118.45 this year. Consumption is expected to decline slightly from 122.94 million bales this season to 121.91 next year. Despite higher production and lower consumption, the supply gap still leaves a million bales to be covered and world stocks are therefore expected to continue to decrease in 2022/2023. World Less China stocks are forecast to decline from 47.17 million bales to 46.40.

Weather and Crop

West Texas and the Texas Panhandle received desperately needed rain early in the week. While the precipitation was beneficial, drought conditions continue to prevail throughout the area and actual coverage was more scattered than we had hoped it would be. Summer-like weather is predicted to be around the rest of May and June. Scattered, severe storms have a possibility of forming next week but will be few and far between. Along with these scattered storms, serious heat and continued dryness are expected. Any kind of moisture will be accepted and all is needed to ensure a timely start for the growing season.

The Week Ahead

With a new WASDE in hand, traders’ minds will be turning back to the weather and crop progress next week. Both the drought conditions in the Southwest and the speed of planting in the Mid-South and Southeast matter. The Export Sales Report will continue to figure prominently, of course.

In the Week Ahead:

- Friday at 2:30 p.m. Central – Commitments of Traders

- Monday at 3:00 p.m. Central – Crop Progress and Condition

- Thursday at 7:30 a.m. Central – Export Sales Report

- Thursday at 2:30 p.m. Central – Cotton-On-Call