July 16, 2021

- December Prices Settle at 89.81 Cents

- Data Shows Inflation in U.S. Economy

- New Marketing Year Sales go to Turkey and Pakistan

- WASDE Highlights

- Cotton Conditions Improve

There was a higher-high every day this week, and December prices finally broke through the heavy resistance that the market has faced each time it attempted to move above 87 cents. The heaviest trading came Wednesday as prices moved steadily through prior market highs, and December settled at 89.81 cents per pound, which is its life-of-contract highest settle. Prices moderated on Thursday, following somewhat tepid Export Sales Report, but still managed to post the December contract’s second highest life-of-contract settle price at 89.05 cents, up 217 points for the week. Open interest gained 10,324 contracts to register 233,963 on Thursday, which is its highest level since early March. The gains were mostly in Tuesday and Wednesday’s trading, implying that new buyers were responsible for the move to new highs.

Outside Markets

Federal Reserve Chairman Jerome Powell gave congressional testimony this week, assuring markets that the Federal Reserve’s most important figure still sees the need for accommodative monetary policy. The public stance of the Fed may have been expected, given that Monday and Tuesday’s price data continued to show rampant inflation in the U.S. at both the consumer and producer levels. While supply disruptions do seem to blame key driver categories such as automobiles, there is not much sign that the supply constraints are as transitory as expected. Stocks have edged back up toward recent highs, despite increased likelihood that the Federal Reserve will taper its bond purchasing sooner rather than later. The market seems to think that the economy is recovering quickly enough that tapering won’t matter.

Export Sales

Export sales seemed to disappoint the market, and futures prices struggled after the release of the weekly report. Old crop sales were 34,500 bales in small lots to several countries. Next marketing year sales were 116,400 bales, primarily to Turkey (58,600) and Pakistan (25,400). Shipments were also slower at just 185,900 bales, which is below the average needed in these last few weeks to hit the USDA’s 2020/2021 export estimate. While the sales seem small, the number are actually in line with the historical averages for this week of the marketing year when the reporting period has one less business day because of the 4th of July holiday.

WASDE

On Monday the USDA released its July update of the World Agricultural Supply and Demand Estimates (WASDE). Although many traders had been waiting expectantly for the report, the release spurred little, if any, additional trading activity in the market. Report highlights for the U.S. included an upward revision to the crop of 800,000 bales to 17.8 million for the 2021/2022 crop, with 400,000 bales of the increase allotted to exports, now forecast at 15.2 million, and 400,000 bales more ending stocks, now 3.3 million. The increased ending stocks were not enough to discourage the market, especially given the USDA also lowered world ending stocks by 1.56 million bales on higher consumption in the outgoing marketing year that lowered the beginning stocks for 2021/2022.

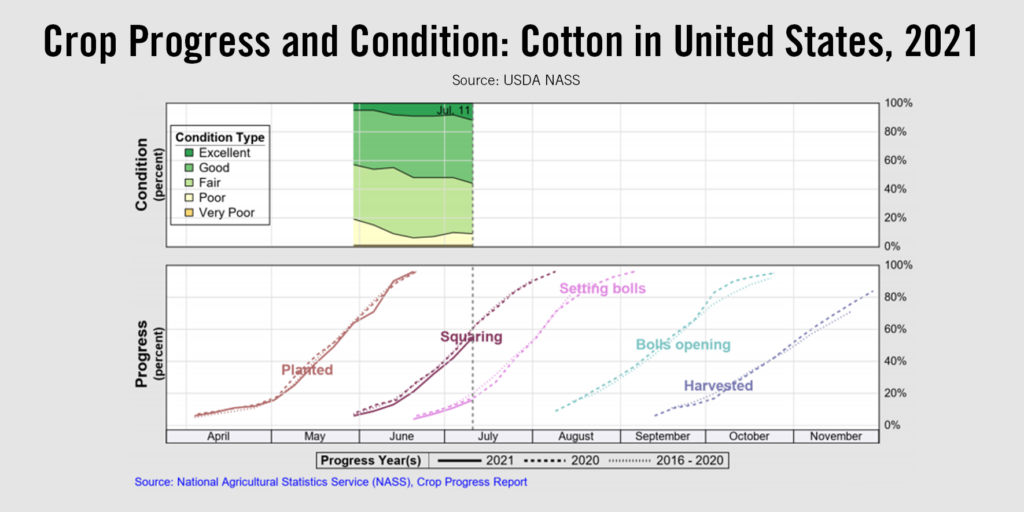

Crop Progress and Weather

Cotton conditions improved slightly in the week to July 11th. The percentage of cotton rated “Good” or “Excellent” increased eight percentage points to 52%, almost as good as in 2017. It is still a bit early to say so, but the condition reading may be hiding some risks. Cool and rainy conditions have delayed crop development in many areas, and the percent of the crop that is squaring is behind the average pace by 7% in Texas and 6% across the Cotton Belt. Late crops translate into greater hurricane and early frost risks, but weather has been ideal for catching up in West Texas. South Texas is still behind.

The Week Ahead

The Week Ahead

The threat of macroeconomic shock from the spread of the delta variant of COVID-19, or rather from the policy measures that could be employed to fight it, are a growing risk that will be on the radar. Policy risk in U.S.-China relations are also still high. Beyond these threats and the usual weekly reports, traders will also be keeping an eye on the tropics for any sign of tropical storm development.

In The Week Ahead:

- Friday at 2:30 p.m. Central – Commitments of Traders

- Monday at 3:00 p.m. Central – Crop Progress and Condition

- Thursday at 7:30 a.m. Central – Export Sales Report

- Thursday at 2:30 p.m. Central – Cotton-On-Call