Cotton Market Weekly August 16, 2024

- The December futures contract lost 9 points for the week ending August 15, settling at 67.15 cents per pound. On Wednesday, a new low settlement price of 67.05 was established.

- A surprise cut to U.S. production on the WASDE report briefly boosted the market, but the momentum was unsustainable. Speculators have reached a record short position, and the selling continued this week. Cotton prices in China have also been down, dragging U.S. futures lower.

- Monday’s WASDE report caused daily volume to spike, but it was otherwise modest. The total number of open contracts increased by 3,352 to 230,009.

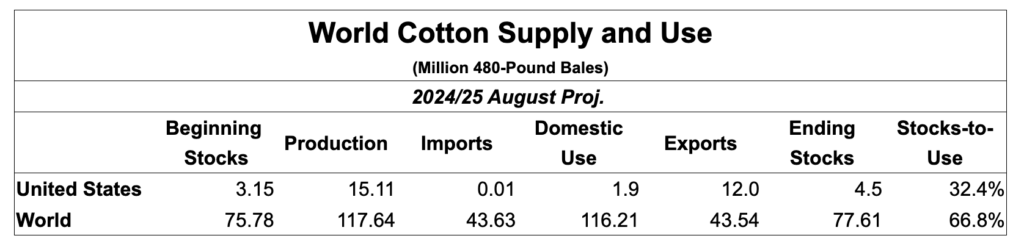

The August World Agricultural Supply and Demand Estimates (WASDE) report showed a massive cut to U.S. production.

- U.S. Production was estimated at 15.1 million bales, down 1.9 million bales from the prior estimate. Exports decreased from 1 million bales to 12 million bales. The changes flowed into ending stocks, which decreased 800,000 bales to 4.5 million bales.

- NASS updated planted acreage in this report. Texas planted acreage is estimated at 5.95 million acres, Oklahoma at 435,000, and Kansas at 130,000. Texas production is estimated at 4.5 million bales, Oklahoma at 430,000 bales, and Kansas at 190,000 bales. The cut to Texas production was a surprise, but the estimate cannot be ruled out with the recent hot and dry weather.

- On the global side of the balance sheet, ending stocks decreased by 5.02 million bales to 77.61 million bales. This change was mainly due to historical misreporting of Chinese stocks.

- World consumption decreased by 980,000 bales to 116.21 million bales. A notable change was the 1.5 million bale decrease in Chinese imports, bringing the country’s estimated imports to 10 million bales.

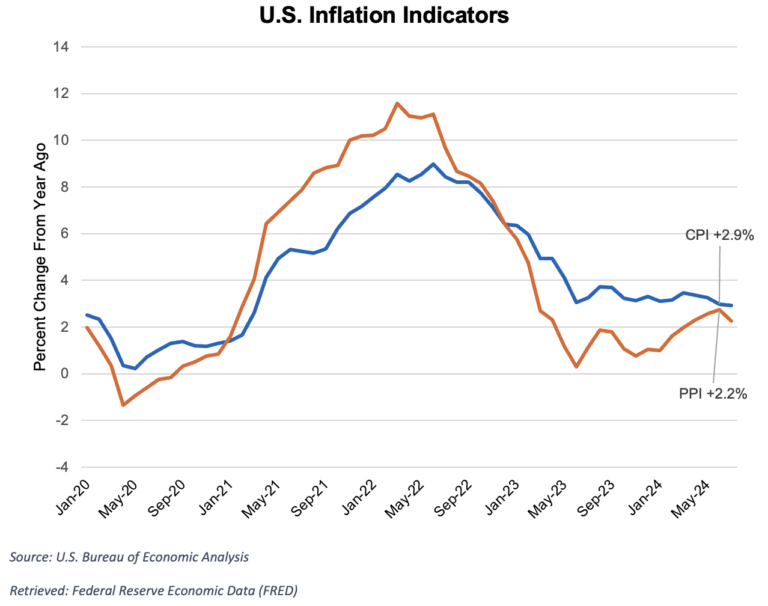

Major markets rallied on cooler inflation readings, all but sealing the deal that the Fed will cut interest rates at the September meeting.

- The U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) were reported below expectations for July. The CPI rose 2.9% on the year, falling below 3% for the first time in three years. The PPI rose 0.1% month-over-month and 2.2% year-over-year.

- The Fed last raised interest rates in July 2023, which have since remained at the highest level in two decades. The Fed has been hesitant to cut interest rates due to high inflation and a strong labor market. Still, the cooler inflation readings that extended into July have them reevaluating their position. The labor market will take center stage in the coming months as the Fed decides whether to cut interest rates.

- The headline U.S. Retail Sales in July encouraged markets and showed that the U.S. consumer continues to spend. Overall, retail sales increased 1% month-over-month and 2.66% year-over-year. However, clothing and clothing accessory sales decreased 0.1% month-over-month but are up 2.5% on the year.

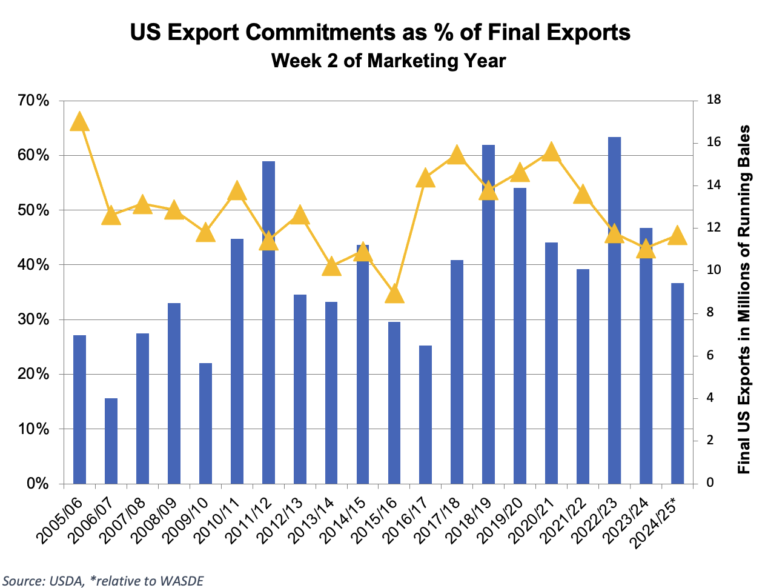

Nothing was extraordinary about the Export Sales Report for the week ending August 8.

- For the 2024/25 marketing year, 110,900 Upland bales were booked for the week. Many expected to see better sales with the low prices recently.

- Shipments of 131,300 bales were below average for this time of the year.

- The U.S. remains at the lowest level of commitments reported for this time of the year since 2016/17.

- Pima merchandisers sold 22,400 bales for the week and exported 8,600 bales.

The good to excellent condition rating for the U.S. increased to 46%.

- The crop rated good to excellent in Texas increased by 1% this week to 33%. Oklahoma remained at 61%, and Kansas decreased 6% to 51%. The crop condition is suspect in the Southwest due to the hot and dry weather seen in recent weeks.

- In the U.S., 74% of cotton is setting bolls, and 13% of bolls are opening.

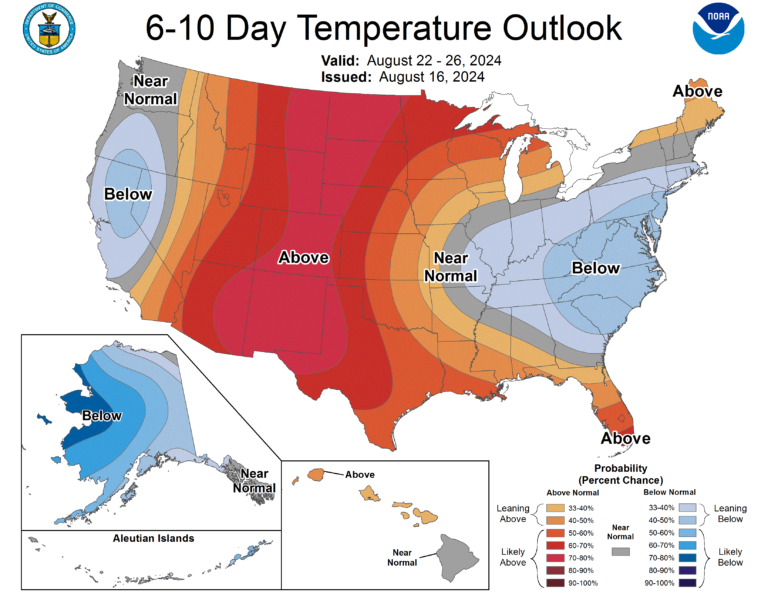

- The weather in South Texas has been favorable in the past week, allowing harvest to continue without interruption. However, the heavy rains in July and early August still raise concerns about yield and quality.

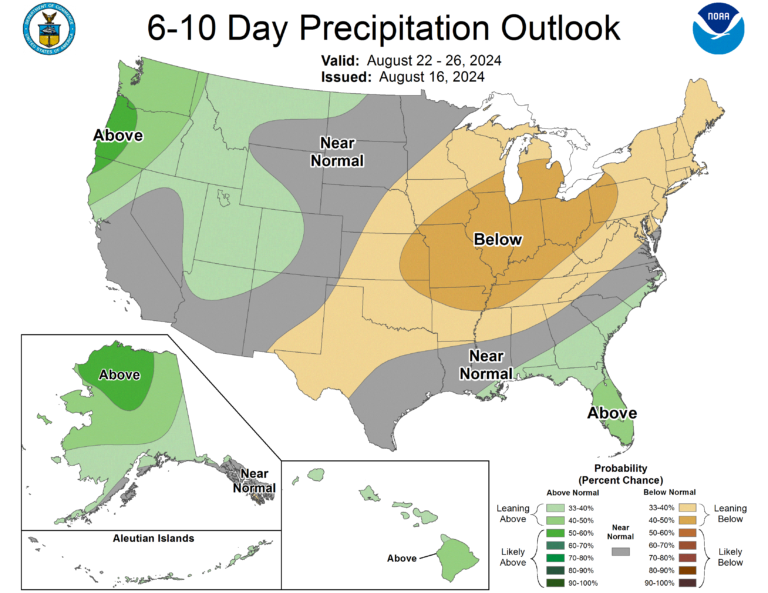

- Areas in West Texas, Oklahoma, and Kansas have recorded multiple days of triple-digit temperatures and very little moisture. Although the crop is slowly progressing, the heat and lack of moisture have impacted the dryland crop. The temperature and precipitation outlook is not encouraging.

The Week Ahead

- Next week will be a slower week for data releases. We will continue monitoring the usual report releases pertaining to the cotton market. We will also monitor the forecast closely, as the crop is struggling under the heat.

The Seam

As of Thursday afternoon, grower offers totaled 18,296 bales. There were 1,982 bales that traded on the G2B platform with an average price of 63.63 cents per lb. The average loan was 54.13 which resulted in a premium 9.50 cents per lb. over the loan.