April 6, 2026

The Week Ahead

Markets remain driven by geopolitics and energy, with Middle East tensions and inflation data in focus.

- Crude oil continues to lead the macro narrative as escalating Middle East conflict keeps energy markets elevated and sentiment highly reactive to headlines. The macro tone remains supportive but volatile, with this week’s inflation data, including PCE and CPI, set to test whether the current narrative can hold.

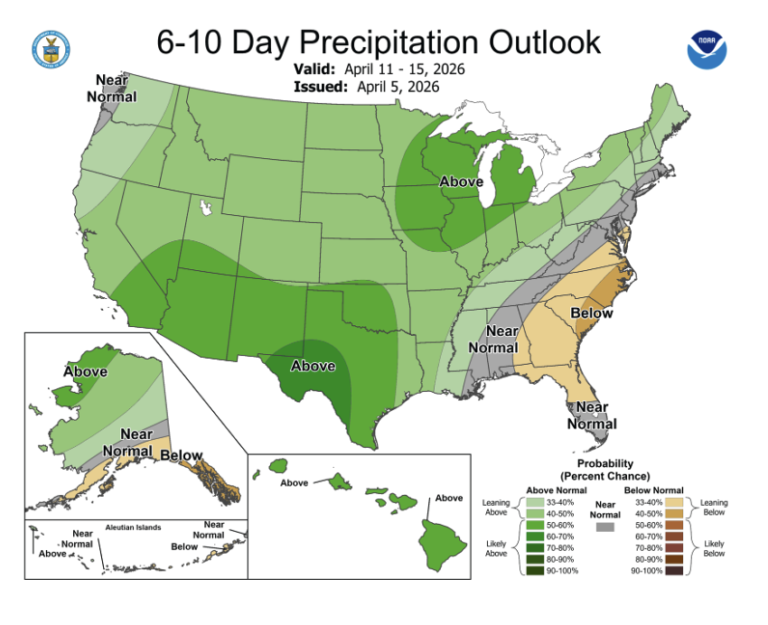

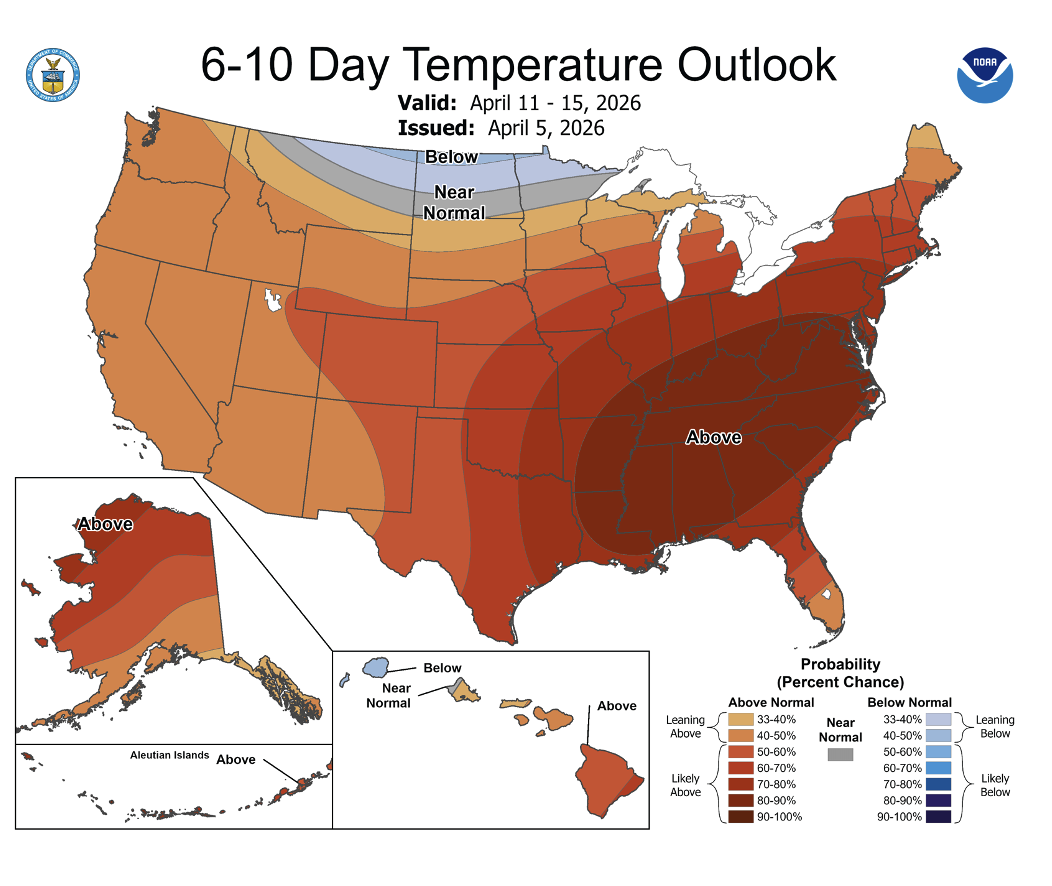

- On the cotton side, attention turns to Thursday’s 11 a.m. CDT release of USDA’s supply and demand report, though it is typically a lighter update ahead of May when new crop balance sheets are introduced. Near-term support continues to come from firm energy markets and seasonal strength, while demand signals and macro direction will remain key drivers.

Market Recap

- Cotton futures moved higher during the shortened week, with May settling 146 points stronger at 70.92 cents per pound. Prices pushed back above the 70-cent mark early and held that level through all four trading days. Technical signals were supportive, and continued fund buying and strength in outside markets, particularly energy, helped underpin the move.

- Price action remained volatile, with the market pulling back from the session highs at times while still holding together on the week. By Thursday, futures traded more two-sided as the market worked through strong export data and began positioning ahead of next week’s supply and demand report. Despite the choppier trade, the market held together well, supported by steady shipments and consistent demand signals.

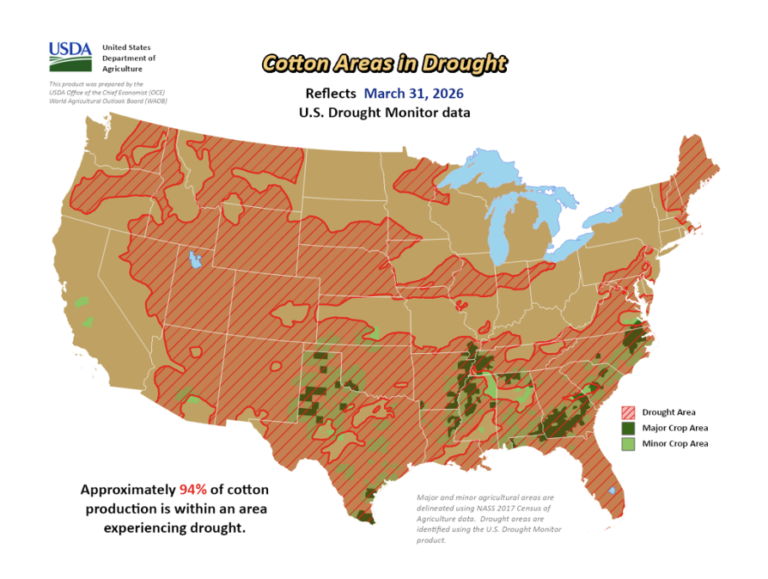

- USDA’s Prospective Plantings report showed 9.64 million acres for the 2026 crop, at the higher end of expectations and up roughly 4% from last year’s 9.28 million acres. The increase was largely driven by the Southwest, with Texas estimated at 5.52 million acres, Oklahoma at 450,000, and Kansas at 100,000. The figure came in above both the National Cotton Council’s 8.99 million acres and USDA’s February Ag Outlook of 9.4 million. While the report leaned bearish on the surface, uncertainty around final acreage remains, given ongoing drought concerns and volatility in input costs during the survey period.

- Continued buying in the latest Commitments of Traders report supported the market, while on-call activity improved for a seventh consecutive week as the imbalance narrowed. Trading activity remained active, with open interest falling 2,582 contracts to 340,588, and certificated stocks declining 1,424 bales to 113,241.

Economic and Policy Outlook

- Tensions around the Iran conflict remain high, with early signs of a potential ceasefire breaking down after Iran rejected the latest proposal and negotiations stalled ahead of a key U.S. deadline. The Strait of Hormuz continues to be the focal point, with restricted vessel traffic and ongoing threats to energy infrastructure keeping supply risks elevated. Oil markets have responded with sharp volatility, holding above $100 per barrel, while refined products like diesel and jet fuel are seeing even tighter conditions due to disruptions in shipping and refining capacity.

- Even with OPEC+ signaling higher output, the market remains skeptical that additional supply can offset current disruptions, especially given logistical constraints in the region. The result is increasing concern that higher energy costs could feed back into broader inflation, particularly across transportation and agriculture. For now, markets remain highly reactive to headlines, with further escalation posing upside risk to prices, while any meaningful progress toward reopening Hormuz could bring some relief.

- The March jobs report showed a stronger-than-expected rebound, with 178,000 jobs added and the unemployment rate dipping to 4.3%, pointing to a still-stable labor market. Gains were broad across sectors, aided in part by a recovery from weather and strike-related weakness in February. Wage growth remained relatively modest, even as rising energy costs begin to filter through the economy. While the data reflects resilience for now, the broader impact from geopolitical tensions and higher input costs is likely to build in the months ahead.

- USDA is focused on rising input costs, with fertilizer at the center as global disruptions tied to the Strait of Hormuz push prices higher. According to USDA, about 80% of U.S. farmers had already secured fertilizer ahead of planting, limiting immediate impact, while policy efforts are aimed at easing costs and improving access for the remaining 20%. Longer term, the administration has said it is looking at supply chain, energy, and pricing pressures as part of a broader effort to bring down elevated production costs.

Supply and Demand Overview

- U.S. export sales improved in the week ending March 26. Net upland sales totaled 371,500 bales, up from the previous week and the prior four-week average, with Vietnam, Turkey, and China leading the way. New crop sales reached 117,300 bales, primarily to Turkey and Mexico, while Pima sales were also strong at 15,500 bales.

- Shipments were solid, with upland at 356,700 bales, running above the recent pace, and Pima shipments at 7,600 bales. Looking ahead, shipments will need to average just under 300,000 bales per week to reach USDA’s 12 million bale export estimate. Overall, it was a solid report driven by strong movement, though there’s still ground to cover.

The Seam®

- As of Thursday afternoon, grower offers totaled 5,416 bales. The past week 19,828 bales traded on the G2B platform received an average price of 71.54 cents per pound. The average loan redemption rate (LRR) was 54.51, bringing the average premium over the LRR to 17.03 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).