Markets will look for more clarity this week after disappointing Trump-Xi meetings and heavy liquidation across commodities late last week.

May 18, 2026

The Week Ahead

Outside markets will remain a major driver for cotton this week. Firmer inflation data, higher Treasury yields, and a stronger U.S. dollar pressured risk appetite late last week, while crude oil continues to find support and remains important for the broader commodity space and polyester economics.

Trump-Xi developments and the broader shift toward a macro “risk-off” environment triggered heavy liquidation across commodities late last week, prompting funds to unwind some crowded long positions across agriculture. Cotton remains one of the more overbought ag markets and could stay vulnerable if outside pressure persists.

Trade policy will stay in focus after China agreed to purchase at least $17 billion annually in U.S. agricultural products from 2026 through 2028, though the lack of immediate buying announcements during the meetings disappointed traders.

On the calendar, big tech earnings, Fed minutes, and weekly export sales will be key market drivers this week. Weather across the Cotton Belt will also remain in focus, especially as more discussion surrounding a potential “Super” El Niño begins gaining traction.

Market Recap

A sharp and turbulent sell-off took hold in the cotton market this past week. After reaching another contract high, cotton futures sharply reversed lower, with prices going limit down at one point before recovering some losses into the close. The July contract settled at 80.61 cents per pound, down 412 points on the week. Meanwhile, the December contract also moved lower, settling at 81.91 cents, down 355 points for the week.

Outside markets remained firmly in control throughout last week, though sentiment shifted dramatically as the days progressed. Cotton futures pushed to fresh highs early in the week alongside strength in crude oil and continued speculative buying before quickly reversing course as broader macro pressure triggered heavy liquidation across commodities. Markets struggled to find direction amid ongoing Trump-Xi headlines, inflation concerns, Middle East tensions, and a stronger U.S. dollar, all of which contributed to sharp swings in overall risk appetite.

Fundamentally, the market began showing signs of fatigue at elevated price levels despite a generally supportive underlying backdrop. Certificated stocks continued building through the week, basis levels softened in some areas, and the old-crop inverse began easing after becoming inverted earlier in the rally. Speculative length also remained a major focus as traders worked through an increasingly volatile macro environment.

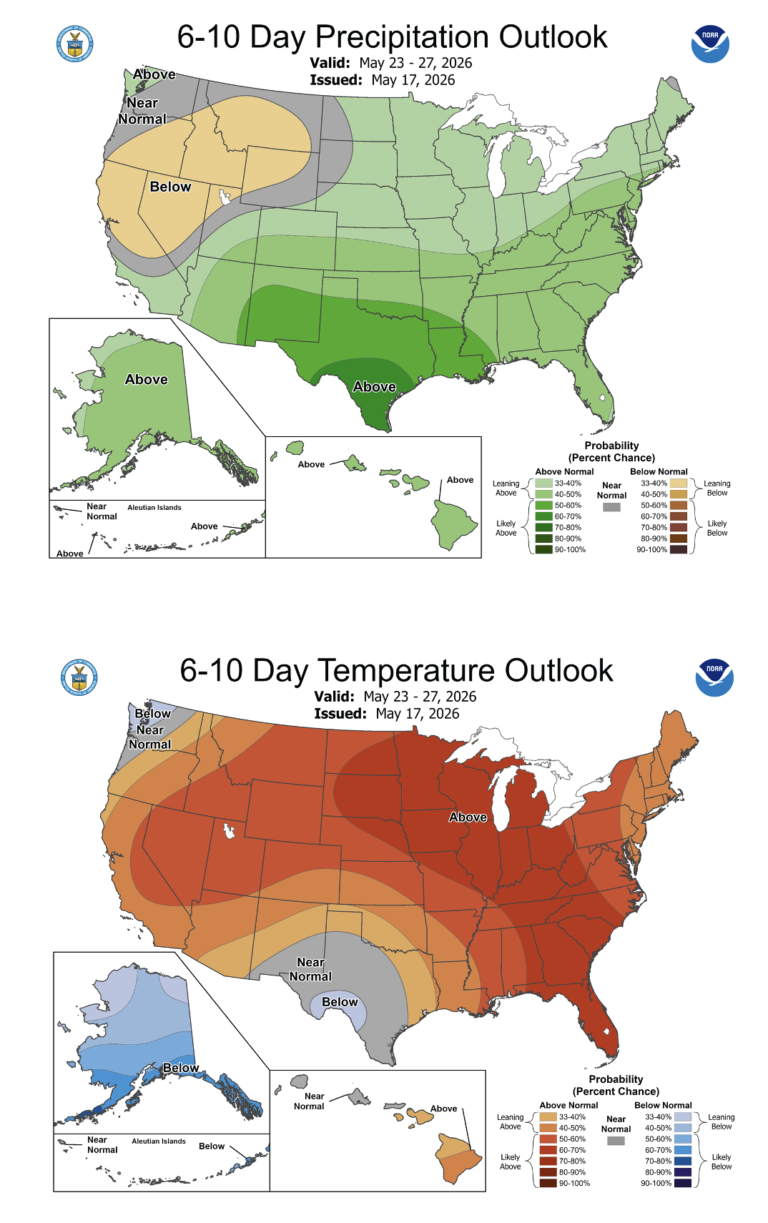

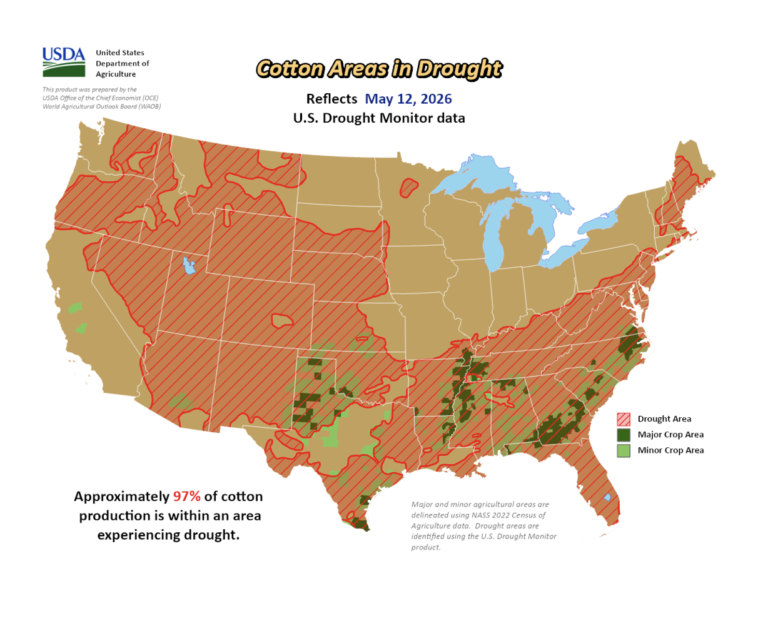

Weather also stayed front and center. Rainfall remained uneven across the Cotton Belt, with parts of the Delta and Southeast seeing improvement while much of West Texas continued battling persistent dryness for most of the week. Forecasts later began hinting at better moisture chances across portions of the Southwest, though drought remains widespread and continues to hang over the market as planting season moves forward.

Economic and Policy Outlook

For weeks, it felt like every market conversation somehow circled back to Iran, crude oil, and the Strait of Hormuz. This past week, though, focus finally shifted as U.S.-China trade talks returned to the spotlight. While both sides struck a positive tone during Trump’s two-day summit in Beijing and discussed expanded trade cooperation and potential tariff reductions, few concrete details were released initially.

That changed Sunday when the White House stated China had agreed to purchase at least $17 billion annually in U.S. agricultural products through 2028. Markets initially welcomed the headlines, though skepticism quickly followed as traders questioned how meaningful or enforceable the commitments would ultimately be. Still, the overall tone across markets has remained broadly supportive following the announcement.

April CPI came in hotter than expected, with headline inflation rising 0.6% month-over-month and 3.8% year-over-year, above expectations of 3.7%. Rising gas, grocery, and transportation costs, largely tied to the recent surge in energy prices driven by the Iran conflict, were major drivers behind the increase. The stronger inflation data reinforced expectations that the Fed may keep rates at the current 3.50–3.75% range for longer, supporting the U.S. dollar and potentially creating a tougher macro backdrop for commodities like cotton.

Supply and Demand Overview

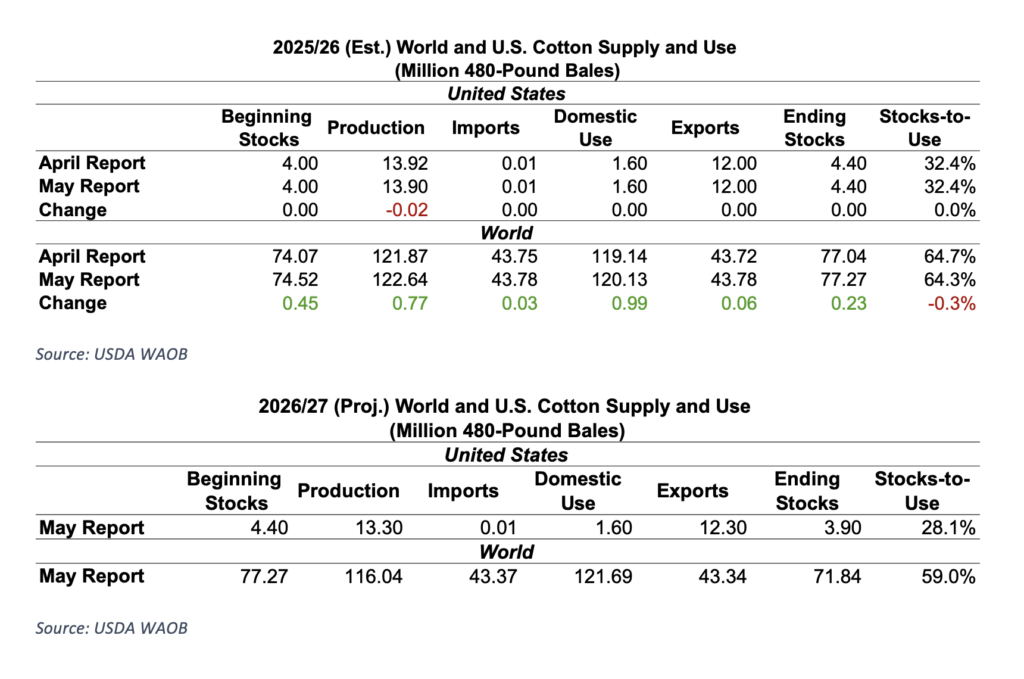

USDA made very few changes to the 2025/26 U.S. cotton outlook, slightly lowering production to 13.9 million bales while otherwise leaving estimates largely unchanged following recent strength in futures. Globally, production, consumption, and ending stocks were all revised modestly higher, largely reflecting a larger Uzbekistan crop and stronger mill use in both Uzbekistan and China.

USDA’s first look at the 2026/27 cotton balance sheet leaned modestly supportive, with lower U.S. production and ending stocks paired against stronger export expectations. Using March Prospective Plantings acreage of 9.64 million acres, USDA projected a 13.3 million bale crop, while exports were forecast at 12.3 million bales on stronger global demand. Ending stocks were projected at 3.9 million bales, tightening the stocks-to-use ratio to 28.1%, with the season-average farm price estimated at 73 cents per pound. Globally, production is expected to decline while consumption increases, leading to a 7% drop in world ending stocks.

For the week ending May 7, U.S. export sales slowed notably, with net Upland sales totaling just 47,700 bales for the current marketing year, a marketing-year low and down sharply from both the previous week and recent averages. Vietnam led buying activity, followed by Indonesia, Turkey, Pakistan, and Thailand, while cancellations from Japan weighed on totals. New crop sales came in at 29,700 bales, driven primarily by Vietnam, Mexico, Bangladesh, and Guatemala, though reductions to Pakistan limited gains.

Shipments remained respectable at 290,300 bales. Vietnam was again the top destination, followed by Turkey, Bangladesh, China, and Pakistan. Pima activity also softened, with sales totaling 9,300 bales and shipments at 12,100 bales. While sales activity has cooled as prices remain elevated and uncertainty lingers, shipment pace still remains relatively solid against USDA’s current 12 million bale export projection if sustained.

The Seam®

As of Friday afternoon, grower offers totaled 1,363 bales. The past week 11,683 bales traded on the G2B platform received an average price of 79.47 cents per pound. The average loan redemption rate (LRR) was 55.63, bringing the average premium over the LRR to 23.84 cents per pound.