October 11, 2024

Cotton futures remained rangebound for the week, but the October WASDE report was a bearish surprise to the market. As traders absorb these changes, all eyes are now on harvest progress and global supply dynamics. Was the USDA accurate in its production estimates, or could further adjustments be on the horizon? Get QuickTake’s read on the week’s events in five minutes.

- December futures decreased by seven points, settling at 72.66 cents per pound for the week ending October 10.

- The cotton market was quiet this week in anticipation of the WASDE report despite stronger equity markets. It was tough to find news that would significantly impact the market after it was revealed Hurricane Milton would miss major cotton areas in the Southeast. China returned from holiday, but no meaningful business was done upon their return.

- This week, the daily volume traded was moderate. Contracts were steadily added to open interest each day, increasing the total number of open contracts by 8,834 to 241,618.

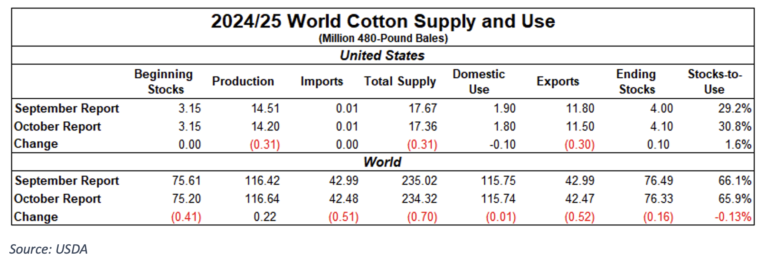

The October World Agricultural Supply and Demand Estimates (WASDE) Report was a bearish surprise for the cotton market.

- U.S. Production was cut 310,000 bales to 14.2 million bales. The Southeast crop was cut 470,000 bales due to hurricane damage. Surprisingly, the Southwest crop saw an overall increase of 250,000 bales. Estimated Texas production increased 300,000 bales to 4.4 million bales, Kansas increased 10,000 bales to 190,000 bales, while Oklahoma decreased 60,000 bales to 290,000 bales.

- The reduction in U.S. exports mirrored the cut in production, with exports lowered by 300,000 bales to 11.5 million bales. Additionally, domestic consumption declined by 100,000 bales to 1.8 million bales. These changes resulted in an increased stocks-to-use ratio of 30.8%.

- World production still outpaces world consumption. World production increased 220,000 bales to 116.64 million bales, while consumption was almost unchanged at 115.74 million bales, decreasing by only 10,000 bales.

- Other notable changes on the world balance sheet included a 500,000-bale decrease in China’s import number, bringing the total estimated imports to 9 million bales. Production in China increased 400,000 bales to 28.2 million bales. Brazilian production also increased 100,000 bales, bringing total production to 16.8 million bales.

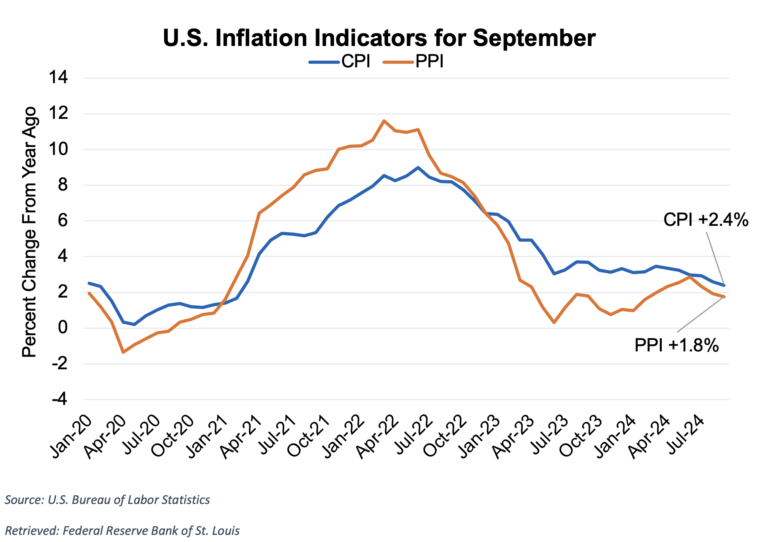

Stock markets rallied this week on the strength of solid tech earnings, but mixed inflation data provided conflicting signals to investors.

- In September, the U.S. Consumer Price Index (CPI) increased by 0.2% for the month and 2.4% year-over-year, both exceeding market expectations by a percentage point and indicating a slightly hotter reading than anticipated. However, these figures eased from last month’s levels, and it was the smallest one-year rise since February 2021.

- The U.S. Producer Price Index (PPI) was flat for September and rose 1.8% compared to last year. This reading was slightly better than the market expected, providing the Fed with mixed signals on inflation ahead of next month’s meeting.

- The U.S. dollar reached its highest level this week since mid-August, gaining ground on heightened geopolitical tensions and inflation data.

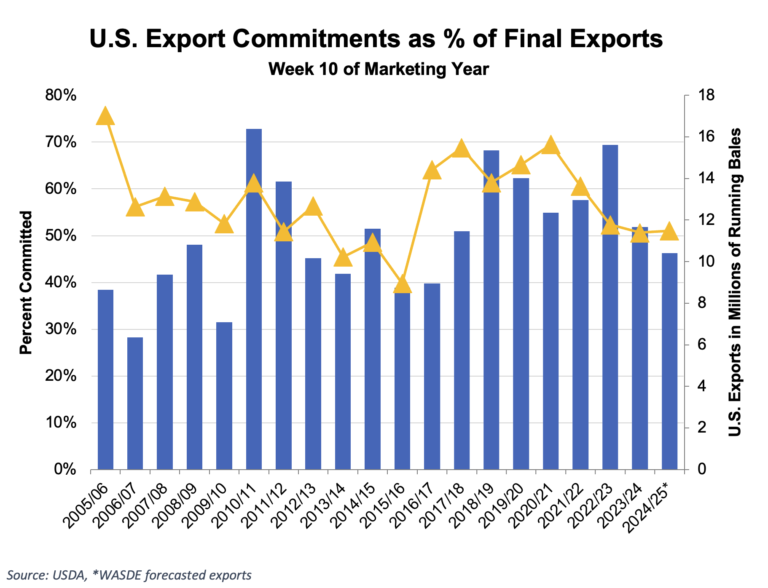

U.S. export sales and shipments were again underwhelming for the week ending October 3.

- For the 2024/25 marketing year, 89,600 Upland bales were booked, reflecting another week of lackluster demand.

- Shipments of 95,100 bales were far below average for this time of the year, providing another indicator of stagnant conditions.

- The percent of the U.S. crop committed for the year continues to trail behind last year’s low level and represents the lowest amount committed since 2016/17.

- Demand for U.S. Pima cotton has remained steady. Pima merchandisers sold 9,100 bales for the week and exported 6,500 bales.

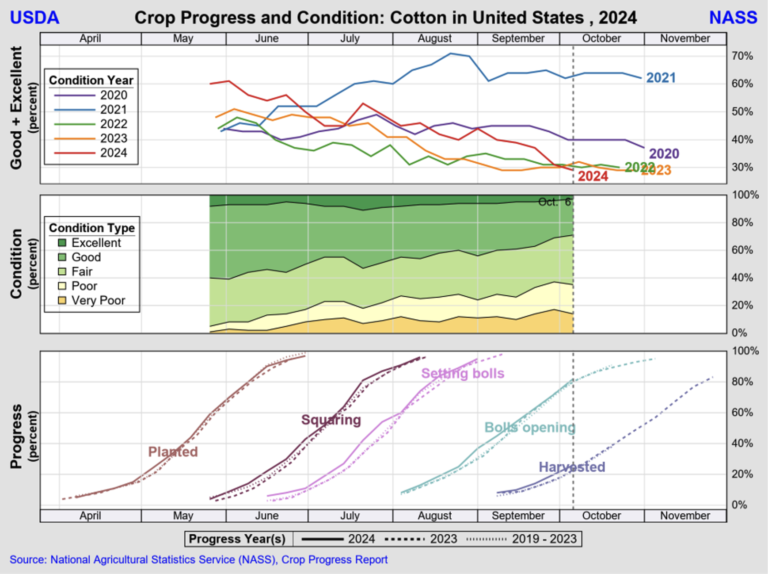

The overall percentage of the U.S. crop rated as good to excellent has fallen to its lowest level in five years, dropping to 29%.

- The percentage of crops rated good to excellent in Texas decreased 3% to 17%. Oklahoma’s good to excellent rating decreased 9% to 17%, and Kansas’s decreased 7% to 42%.

- In the U.S., 26% of the crop has been harvested. Hot, dry weather has helped the final stages of development for the crop in West Texas, Oklahoma, and Kansas. Harvest has expanded rapidly, and ginning has begun in many areas.

- Hurricane Milton formed in the Gulf of Mexico last week and quickly crossed the Gulf to make landfall in Florida. While the strong storm was damaging to the state, it did not pose a threat to cotton-growing areas in the Southeast.

The Week Ahead

- With new data to trade, the cotton market is back to business as usual. We will continue to monitor harvest progress, ginning activity, and crop quality as the cotton comes in.

- Markets will be open on Monday, but a federal holiday will delay the release of the Crop Progress and Condition Report and the Export Sales Report.

The Seam

As of Thursday afternoon, grower offers totaled 21,138 bales. There were 594 bales that traded on the G2B platform at an average price of 68.29 cents per pound. The average loan was 53.90 cents per pound, resulting in a premium of 14.39 cents over the loan.