Dilys Wang

Import details in Apr, 2026

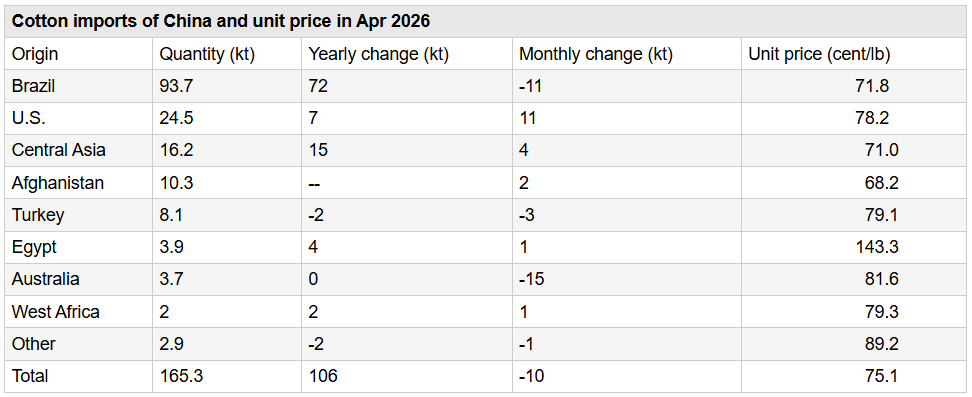

The table above lists China's major cotton import sources, ordered by import volume from highest to lowest. Of the 165.3kt of cotton imported by China in Apr, Brazil was still the top supplier with 93.7kt of cotton imported, a year-on-year increase of 72kt, but down by 11kt from Mar. U.S. cotton imports amounted to 24.5kt, a year-on-year increase of 7kt and a month-on-month increase of 11kt. Imports from Central Asia were 16.2kt, up 15kt year-on-year and 4kt month-on-month. Besides, imports from Afghanistan were above 10kt.

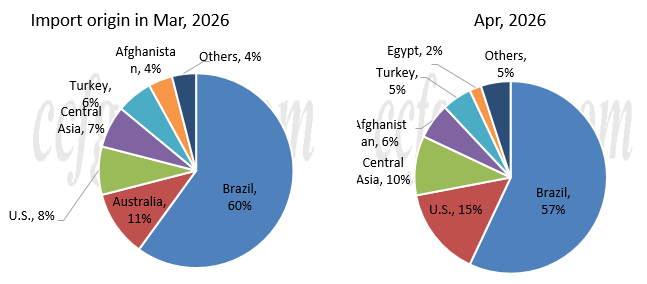

In terms of import shares for Apr 2026, Brazilian cotton accounted for 57%, up 20 percentage point from the same period in 2025 and down 3 percentage points from Mar (60%); U.S. cotton made up 15%, down 15 percentage points from 5% a year earlier and up 7 percentage points from 8% in Mar; and Central Asian cotton represented 10%, up 8 percentage points from 2% in Apr 2025 and up 3 percentage point from 7% in Mar.

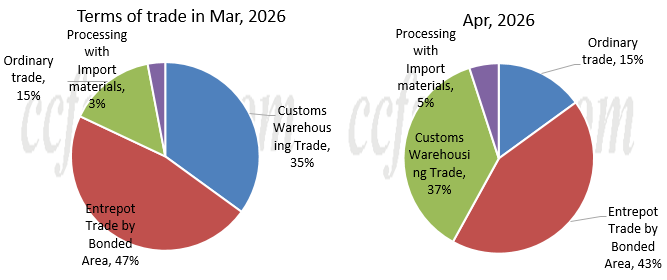

For the terms of trade, the share of ordinary trade in Apr was flat at 15%. The combined proportion of entrepot trade by bonded area and customs warehousing trade accounted for stood at 80%, down 2 percentage points from 82% in Mar. The proportion of processing with imported materials rose by 2 percentage points from Mar to 5%.

For the terms of trade, the share of ordinary trade in Apr was flat at 15%. The combined proportion of entrepot trade by bonded area and customs warehousing trade accounted for stood at 80%, down 2 percentage points from 82% in Mar. The proportion of processing with imported materials rose by 2 percentage points from Mar to 5%.

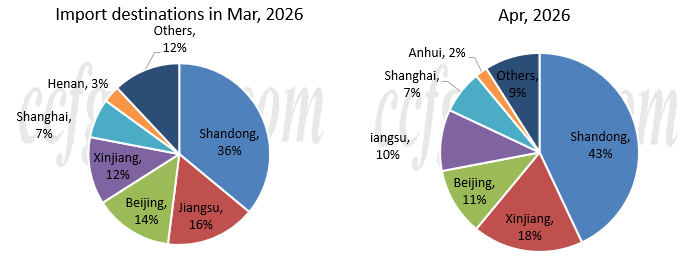

In Apr, enterprises from Shandong, Xinjiang and Beijing ranked top three in cotton imports: Shandong's share increased by 7 percentage points to 43%. Xinjiang's share rose 6 percentage points to 18%. Beijing's share reduced 3 percentage points to 11%.

General condition of China cotton imports:

On the afternoon of Aug 25, 2025, relevant departments issued an announcement on the allocation of the sliding-scale duty quota for imported cotton in 2025. The allocated volume remains at only 200,000 tons, which can only be imported through processing trade and is distributed on the basis of contract applications, with a relatively narrow scope of use. On Mar 16, 2026, China announced to allocate 300kt sliding-scale duty quotas. Coupled with the 894,000 tons of 1% duty quota allocated each year, the known quota for the 2025/26 season has reached 1.394 million tons. The Tariff Commission of the State Council announced on March 4, 2025, that a 15% tariff would be imposed on U.S. cotton. Under the 1% duty quota, the import tax rate for U.S. cotton is: 1% duty + 15% separately imposed additional duty + 10% reciprocal duty. On Nov 5, 2025, the Tariff Policy Commission of the State Council announced that, starting from 13:01 on Nov 10, 2025, it would terminate the additional tariff measures specified in the Announcement of the Tariff Policy Commission of the State Council on Imposing Additional Tariffs on Certain Imports Originating in the United States (Announcement No. 2 of the Tariff Policy Commission, 2025). Specifically, this means the 15% additional tariff on U.S. cotton is lifted; the applicable import tariff rate for U.S. cotton will be a combination of a 1% tariff and a 10% reciprocal duty.

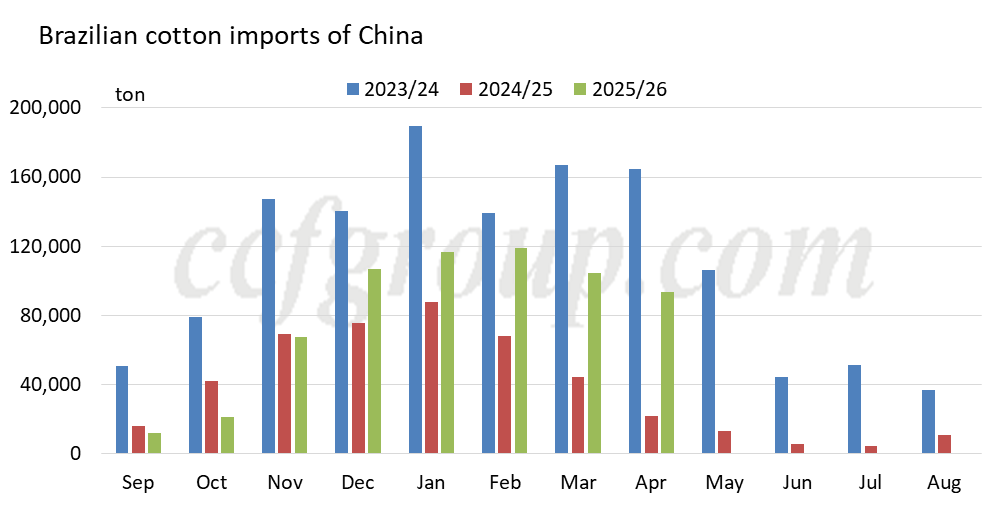

Brazilian cotton remained the top imported variety in China during Apr 2026. In Apr 2026, China imported 93.7kt of Brazilian cotton, down 10.7kt month-on-month and up 71.8kt year on year; in the first four months of 2026, imports amounted to 434kt, an increase of 211kt compared with the same period last year. For the 2025/26 marketing year (Sep-Apr), China imported 642kt of Brazilian cotton, up 216kt from the 426kt recorded in the year-earlier period.

The average unit price of imported cotton is calculated by dividing the total customs value of imported cotton by the total quantity. Among the major imported cotton varieties in Apr, the average price of Brazilian cotton was 71.78cent/lb, and that of U.S. cotton was 78.22cent/lb.

Conclusion:

Cotton imports are expected to stabilize with a slight decline in May, and Brazilian cotton will remain the top import variety.