International cotton prices moved lower during most of May, influenced by a fall in New York futures. The Cotlook A Index began the month at 94.90 US cents per lb, reaching a high point of 95.10 on May 10, before a sustained decline saw the Index end the month at 89.40. Speculative selling appeared to be the main reason for the decline in futures, in which the lead July contract fell to its lowest point since mid-late January. On May 21, the December contract moved to a premium over July, which widened as the month-end approached. Open interest continued to rise during most of the period.

The downturn in futures mid-month saw shippers’ asking prices fall and triggered a revival of active mill demand. What began as price-testing in the second week of May became broad-based buying interest from a wide range of markets, albeit mainly to cover spinnersΆ most pressing requirements. Forward business was scarce in the first half of the month, but as the review period progressed some sporadic forward enquiry emanated from certain Far Eastern markets.

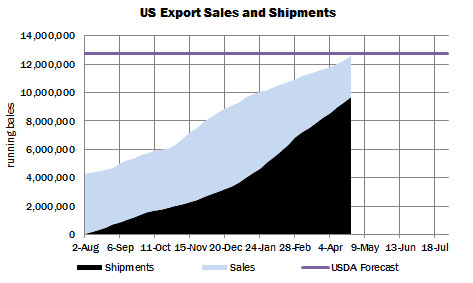

Weekly United States export figures reflected that the recent robust pace of sales commitments has slowed somewhat. Nonetheless, the five USDA export sales reports during May saw this seasonΆs upland export sales commitments rise by an aggregate 725,000 running bales and 27,500 of Pima, resulting in a further tightening of the short-term supply position. Weekly shipments have been continuing apace and, by the week ended May 23, almost 85 percent of the volume sold had been shipped. In order to achieve USDAΆs forecast of the volume to be shipped in the current season the weekly volume that must be shipped is just over less than 190,000 running bales.

WashingtonΆs export projection for 2012/13 was increased to 13.25 million statistical bales of 480 lbs, in its May report, which also featured the release of the DepartmentΆs initial supply and demand numbers for the 2013/14 marketing year. The report prompted a rather bearish reaction, since (like our own) USDAΆs statistics indicate a further increase in the global cotton surplus in 2013/14, and record world stocks by the end of next season.

On a more positive note, import buying remained a feature of the Chinese market, either for shipment or from stocks held on consignment. Spinners in possession of allocated import quota, or those registered to take advantage of the 3:1 ratio of state reserve purchases to import quota entitlement, have been quite active in the international market, in addition to buying at the state reserve auctions, at significantly above the level of world prices. It will be recalled that mills are limited in the amounts they can buy by July 31, to the equivalent of either six or eight months of their assessed annual consumption. ChinaΆs raw cotton imports in April totalled almost 431,000 tonnes. The main suppliers were the United States, India and Uzbekistan. Chinese spinners have also turned to Australian cotton of late, for shipments from May onward.

The persistence of strong import data and market reports of continued import buying have prompted an increase in Cotton OutlookΆs Chinese import estimate for 2012/13 to 3.9 million tonnes, which would constitute the third highest seasonal total on record. Somewhat more cautiously, we have also raised our forecast of imports for 2013/14, to 2.5 million tonnes (in line with USDA). Chinese import policy next season remains a source of uncertainty, but considering that the 3:1 principle will be in place at least until the end of July, some of the associated quota will inevitably be used against supplies imported during the early months of the next (August/July) season.

With regard to the state reserve auctions, May saw the pace of mill buying increase somewhat, as 2012/13 crop domestic cotton and imported supplies were made available in greater volume at the daily auctions. Prices have fluctuated widely and spent much of May at a firm level, close to that of the China Cotton Index. By May 31, sales in the current auction series had reached 1.908 million tonnes, leaving the quantity under government control, according to our estimate, at below 9.2 million tonnes.

The Cotton Corporation of India (CCI) has continued to release its stock for tender, in regular on-line auctions. CCI procured over 2 million bales (of 170 kgs) of the domestic crop via its price support operations and an initial tranche of 250,000 bales was earmarked for sale. It will be recalled that a portion of CCIΆs procured stocks was also sold outside the framework of the arranged tender. At the time of writing, a provisional estimate of the cumulative volume sold since the beginning of the auctions is placed at 166,000 lint equivalent bales.

Following the Indian Meteorological DepartmentΆs (IMD) initial long-range forecast for the onset of the Southwest monsoon, the customary mood of anticipation was witnessed in the Indian subcontinent. IMD correctly predicted the date that the Monsoon would make landfall as June 1/3. The rains arrived over Kerala on June 1. Since its arrival, the monsoon has further advanced over the whole of Kerala, parts of coastal and south Karnataka and Tamil Nadu. Conditions are apparently favourable for the northern limit of the monsoon to advance further in the coming days, into Karnataka and Andhra Pradesh.

Elsewhere in the Northern Hemisphere, the main focus has been on the United States crop. West Texas has been suffering from drought conditions, and some farmers are still awaiting moisture before sowing cotton. However, planting deadlines are fast approaching. Scattered storms brought some relief late in the month, but failed to transform the situation, raising the prospect of substantial abandonment. Total cotton planted in Texas was estimated at 49 percent or prospective area on May 30.

Some fields in the Delta remained waterlogged for much of the month and planting is behind the average pace there, as well as in the Southeast. However, sowing in the latter region is advancing quickly.

Primarily to reflect the situation in Texas, Cotton OutlookΆs 2013/14 US production estimate was reduced during the month by nearly 250,000 tonnes, to 3,116,000 tonnes, down from 3,771,000 in 2012/13.

In most other parts of the Northern Hemisphere, planting seems to have proceeded without significant difficulty. No major, weather-related setbacks have thus far come to light.