February 14, 2025

The cotton market saw a slight bounce as traders exited March positions and tariff news continuing to drive volatility across all markets. Have cotton prices found a floor, or will the approaching March First Notice Day bring more volatility as the focus shifts to the May contract? Get QuickTake’s read on the week’s events in five minutes.

The cotton market rebounded from its lows this week with substantial volume as traders exited their March positions.

- March futures closed at 66.83 cents per pound, up 80 points for the week.

- Now that May’s open interest exceeds March’s, focus will shift to the May contract. May futures closed at 67.98 cents per pound, up 76 points for the week.

- The largest of the major indexes began rolling their positions from March to May, and active spread trading defined the marketplace this week. On Tuesday, the March contract saw the second-highest daily trading volume ever. Speculators reached a record net short position, which may have contributed to some of the buying seen early in the week. Outside markets acted as a headwind for cotton. Despite strong export sales, the market finished lower, likely due to bearish fundamentals and the major indexes concluding their roll period.

- The Cotton On-Call report continues to show a significant imbalance in the March contract, with on-call purchases outnumbering sales. While the imbalance decreased from last week, it is expected to shrink further as March First Notice Day approaches, which could put some pressure on the market.

- Daily volume traded was high, and open interest increased by 1,852 contracts, bringing total open interest to 289,825. Certificated stocks were unchanged at 218 bales.

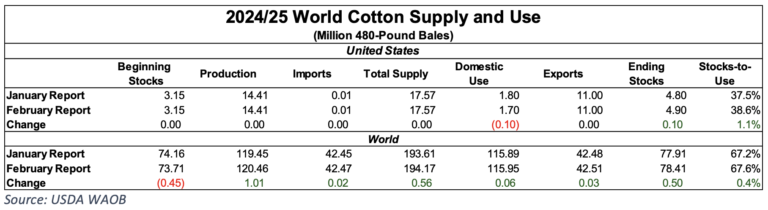

USDA’s February release of the World Agricultural Supply and Demand Estimates (WASDE) Report was uneventful but overall bearish for the cotton market.

- The U.S. side of the balance sheet loosened slightly as domestic consumption was reduced by 100,000 bales to 1.7 million bales. This adjustment led to a 100,000-bale increase in ending stocks, bringing the total to 4.9 million bales. This increased the stocks-to-use ratio to 38.6%. The rest of the U.S. balance sheet remained unchanged, with production at 14.41 million bales and exports at 11.0 million bales.

- The global balance sheet showed a 60,000-bale increase in consumption, bringing it to 115.95 million bales, while ending stocks rose by 500,000 bales to 78.41 million bales. As a result, the stocks-to-use ratio increased to 67.6%. China accounted for the most significant revisions in this report. The country’s crop was raised by 1 million bales to 31 million bales, while imports were lowered by 700,000 bales to 7.3 million bales.

Stock markets fluctuated this week, responding to news on inflation, tariffs, and the potential easing of geopolitical tensions.

- Tariffs have remained a central topic in the headlines, but the market may be showing signs of ‘tariff fatigue.’ The latest update from the Trump Administration indicated that the U.S. would move toward reciprocal tariffs and consider a country-by-country approach to determine tariff levels. These tariffs will not be implemented immediately, and traders saw this as a sign that negotiations could be possible, which helped boost equity markets.

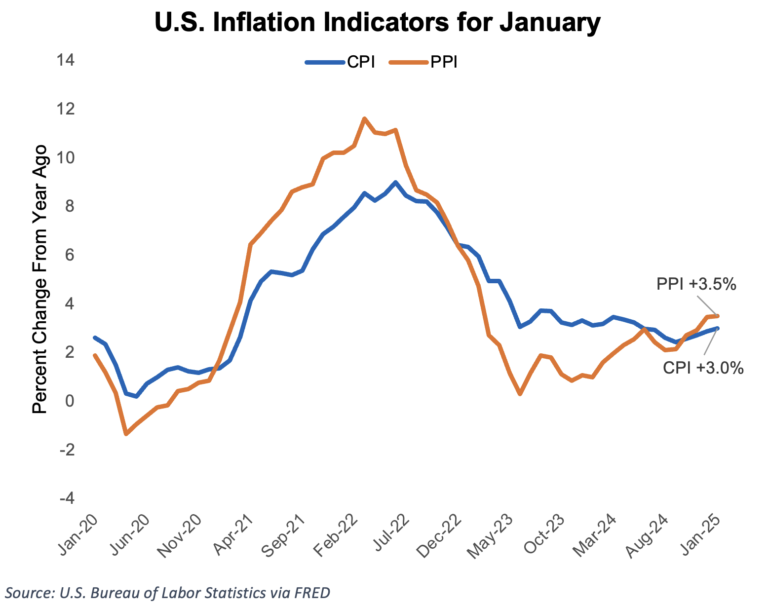

- The U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) came in hotter than analysts had anticipated. For January, CPI rose 0.5% month-over-month, surpassing the 0.3% expected, and increased 3% year-over-year, compared to the 2.9% expected. PPI rose 0.4% month-over-month, above the 0.3% forecast, and climbed 3.5% year-over-year, exceeding the expected 3.2%. In his testimony to Congress this week, Fed Chair Powell stated that the central bank has made progress toward its 2% inflation goal, but it is not yet at the desired level, and there’s no urgency to cut interest rates. The data released this week supports the more restrictive stance being taken.

- Markets reacted positively to President Trump’s announcement that he had initiated peace talks with Russian President Vladimir Putin to help end the war in Ukraine.

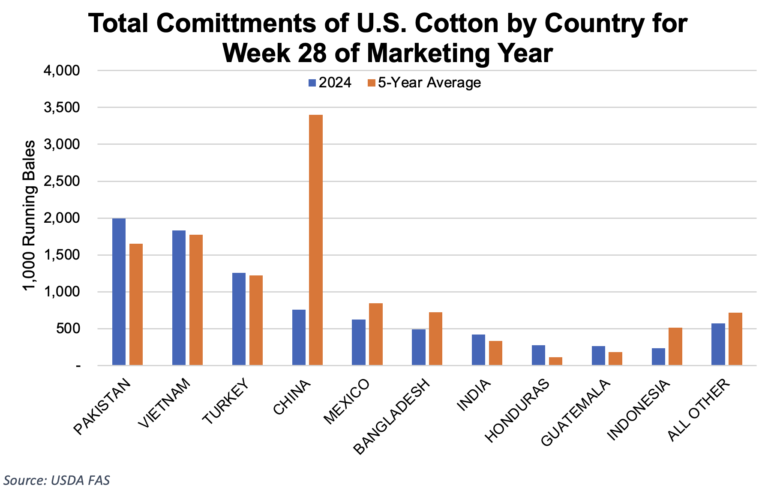

The U.S. Export Sales Report indicated strong sales and a marketing year high for Upland bales shipped during the week ending February 6.

- For the 2024/25 marketing year, U.S. merchants sold 244,700 Upland bales and shipped 260,900 bales. Shipments have remained steady but below the pace needed in recent months to meet USDA’s current export estimate of 11 million bales. This week’s marketing-year high shipments were at the pace required to reach that estimate. Sales have consistently stayed above the necessary level, which is just over 100,000 bales per week.

- As noted in the WASDE and reflected in the Export Sales Reports for the 2024/25 marketing year, China has been notably absent from purchasing U.S. cotton. This is partly due to a larger-than-usual domestic crop and concerns over potential tariffs the U.S. could impose on the country.

- Pima sales were solid, but shipments were at a marketing-year low. Merchandisers sold 4,000 bales and exported 1,100 bales.

The Week Ahead

- The National Cotton Council’s Annual Meeting takes place this weekend. They will release their Economic Outlook and Planting Intentions for the 2024/25 crop on Sunday, February 16.

- Next week will be a shortened trading week due to the President’s Day holiday on Monday, February 17. Data releases will be relatively quiet, with the exception of the reports from NCC on Sunday and the weekly Export Sales Report on Thursday.

- March First Notice Day is on February 24, which could lead to increased activity as traders exit their March positions.

Announcements

Enrollment for the U.S. Cotton Trust Protocol is now open through April 30th, 2025. Growers who are currently enrolled will need to renew their membership to continue their involvement in the program.

New Grower Enrollment for Better Cotton will be open March 3rd-May 30th.

For assistance or questions about enrolling in these programs, contact PCCA at 806-763-8011.

The Seam

As of Thursday afternoon, grower offers totaled 167,606 bales. There were 54,927 bales that traded on G2B platform with an average price of 62.77 cents per lb. The average loan was 51.45, resulting in a premium of 11.32 cents per lb. over the loan.