July 18, 2025

Cotton prices edged higher this week but remained in the same old range. With just weeks left in the marketing year and broader markets gaining momentum, will the quiet persist, or is this merely the calm before the storm? Get QuickTake’s read on the week’s events in five minutes.

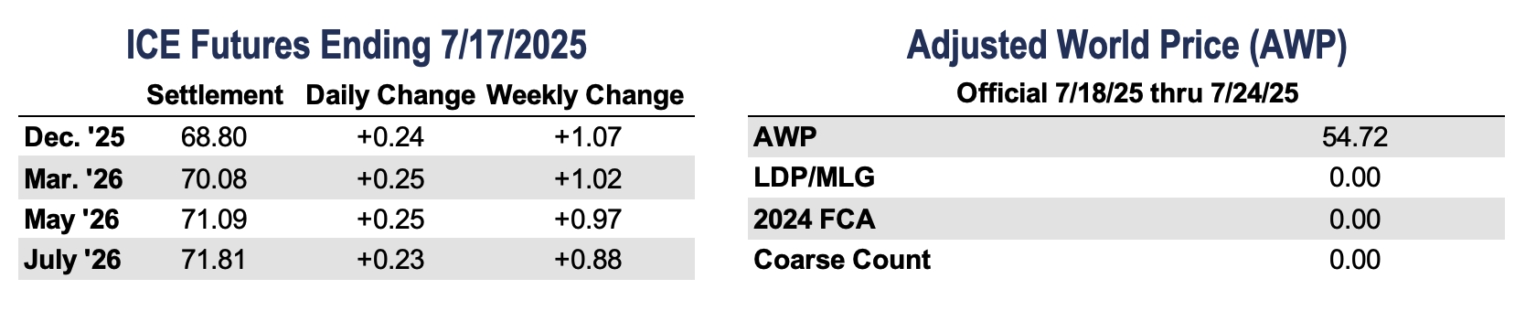

Cotton prices firmed on broader market strength, holding steady despite a heavier balance sheet and seasonal summer trade.

- December futures closed at 68.80 cents per pound, increasing 107 points from the week prior.

- Cotton prices rose in three of five sessions this week, remaining confined to a well-defined range. Support came from renewed trade talks with Indonesia and India, and potential speculative buying as technical stops were triggered. The Indian government officially announced a 7% increase in the minimum support price for cotton for the 2025/26 season, which should provide some support to U.S. cotton prices.

- Despite a stronger U.S. dollar and heavy balance sheets from last week’s supply and demand update, futures briefly topped 69.00 cents per pound. A close above that level could spark further technical momentum, but no fresh catalyst has emerged to break the market out of its range.

- Although PLC reference prices were increased in the One Big Beautiful Bill Act, farm policy talks are back in focus to address the remaining issues, with House Ag Chair GT Thompson aiming for a September push on “Farm Bill 2.0.”

- Trading volume was moderate this week. Open interest increased by 5,998 contracts to 212,229, while certificated stocks fell by 11,866 bales to 23,481, the lowest level since May.

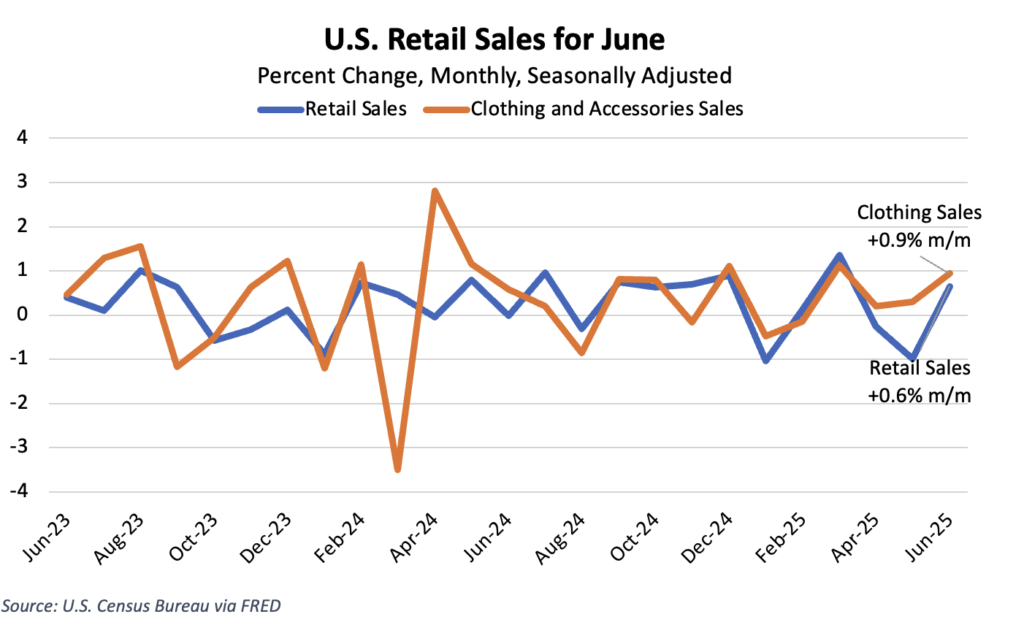

Markets held firm this week as strong retail sales and resilient consumer spending helped offset rising inflation and deepening global trade tensions.

- The S&P 500 hit another record high, with investors encouraged by signs of trade flexibility and upbeat earnings.

- Retail sales rose 0.6% in June, beating forecasts after two months of declines. Core sales, a key GDP input, climbed 0.5%, reinforcing the consumer’s central role in supporting growth. Inflation remains a concern. Headline CPI hit 2.7%, and core CPI reached 2.9%, with Fed officials warning that new tariffs could push inflation up another point into 2026.

- Trade risks escalated again during the week. The U.S. launched a Section 301 probe into Brazil and announced sweeping 50% tariffs set to begin August 1. Canada, Mexico, and Japan remain in tense talks with the U.S. as tariff deadlines approach. Late Wednesday, President Trump said he plans to send a tariff letter to over 150 countries, warning them their rates could jump to 10% or 15%, also starting August 1. The White House has hinted at flexibility but continues to apply pressure through aggressive trade measures.

- Political developments added uncertainty, as Trump proposed removing Fed Chair Powell, drawing attention to questions about central bank independence. The president subsequently retracted the idea. Fed officials, meanwhile, reiterated support for the current policy stance amid rising inflation and market pressures.

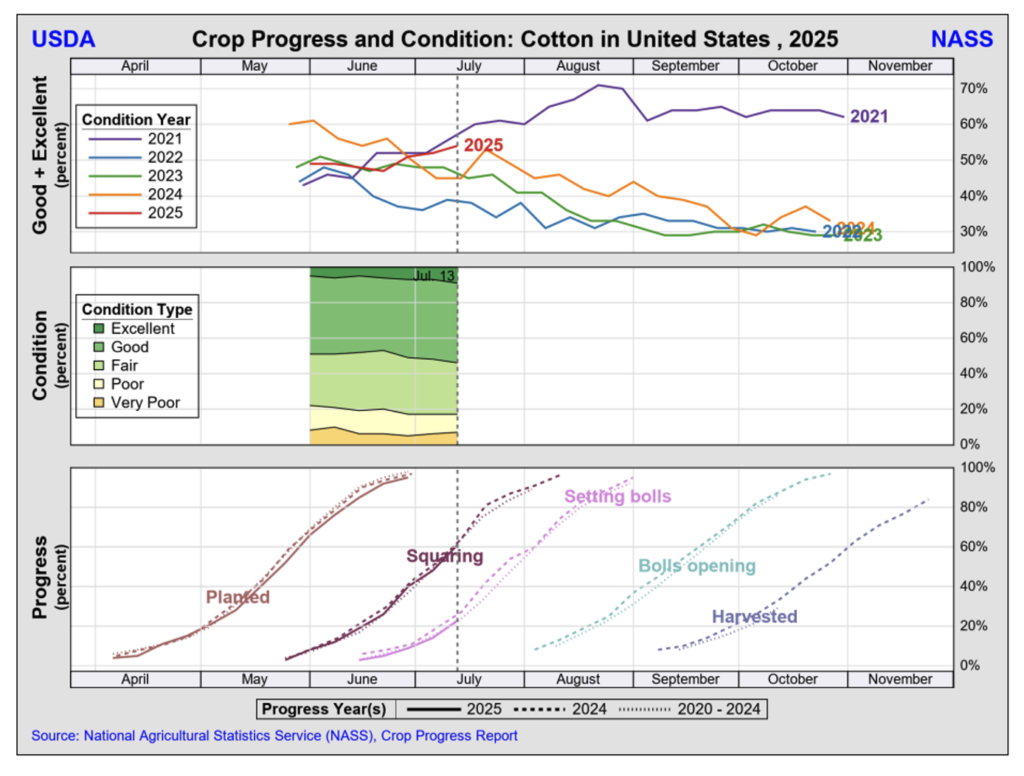

Crop development in the Southwest continues to progress, though the U.S. overall remains slightly behind normal.

- As of July 13, 55% of Texas cotton is squaring and 23% is setting bolls. Oklahoma is 35% squared, and Kansas is 45% with 6% setting bolls. Crop condition ratings improved in all three states, with Texas at 46%, Oklahoma at 62%, and Kansas at 44% rated good to excellent.

- Scattered storms brought rain and high winds to parts of West Texas, Oklahoma, and Kansas, followed by warmer, drier weather that aided development and helped firm saturated soils. Due to a wet spring, weed pressure remains a concern, and producers continue to manage pests and apply herbicides where possible.

- In South Texas, harvest prep is underway under favorable conditions. The Rio Grande Valley crop is maturing rapidly, with widespread picking expected soon. Coastal Bend fields are in full bloom, though storms in the Upper Coastal Bend briefly disrupted fieldwork.

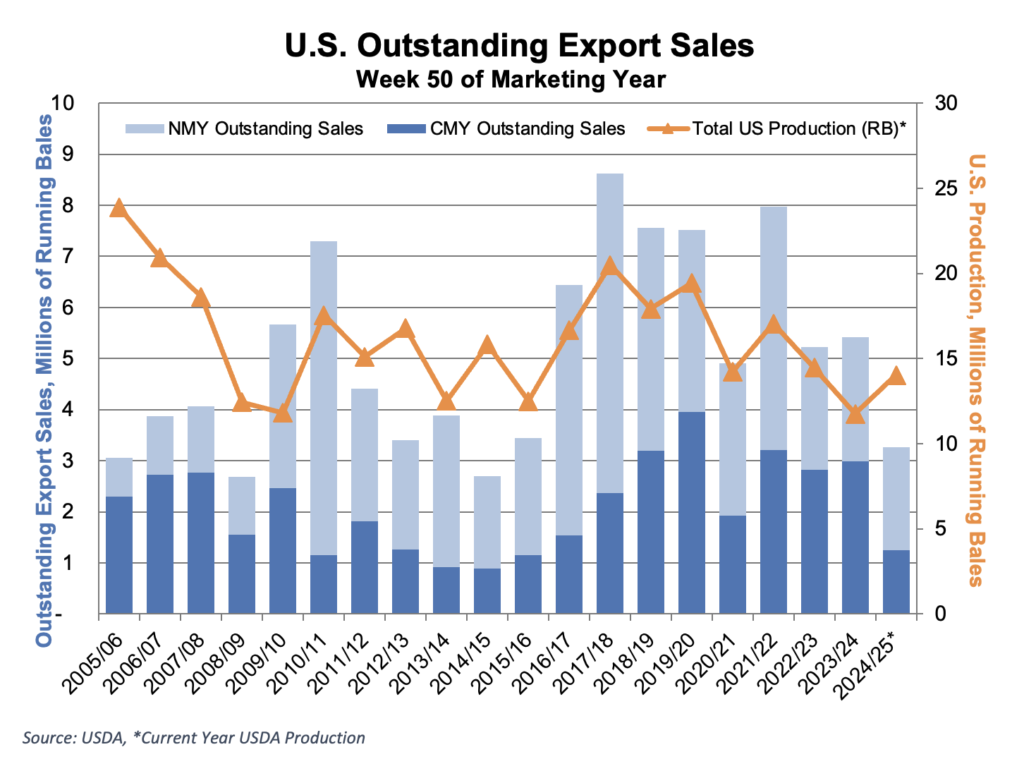

U.S. export sales declined this week, reflecting typical seasonal trends and ongoing market uncertainty late in the marketing year.

- Net Upland sales for the current crop totaled 5,500 bales, led by Vietnam and Peru. Notable cancellations from Pakistan and Thailand, some of which shifted to the next marketing year, also contributed to this. New crop sales were below average at 73,000 bales, driven by demand from Honduras, Nicaragua, and Pakistan. Demand for next year’s crop remains a concern, with commitments at their lowest level since the 2014/15 season.

- With two weeks remaining in the 2024 marketing year, export shipments totaled 156,400 bales, slightly below the pace needed to meet USDA’s 11.8 million bale estimate.

- Current crop Pima sales totaled 2,600 bales, with 3,400 bales sold for new crop. Shipments slowed to 7,900 bales following last week’s marketing-year high.

The Week Ahead

- Retail strength is propping up markets for now, but growing inflation pressure, political volatility, and aggressive trade actions are piling up. With multiple tariff deadlines hitting in August, the calm may not last much longer.

- Next week is expected to be quieter, with the USDA Crop Progress and Condition Report and Export Sales as the main reports to watch.

The Seam

- As of Thursday afternoon, grower offers totaled 27,019 bales. There were 2,927 bales that traded on the G2B platform that received an average price of 62.04 cents per pound. The average loan for these bales was 47.85, bringing the average premium received to 14.19 cents per pound.