January 10, 2025

The cotton market remained quiet ahead of Friday’s WASDE report, which delivered a bearish outlook with increased U.S. production and higher ending stocks. Outside factors shaped broader market sentiment, including strong economic data, an averted port strike, and a robust U.S. dollar. Have cotton prices found a floor, or will the continued demand weakness keep prices trending downward? Get QuickTake’s read on the week’s events in five minutes.

News in the cotton market was light leading up to the release of the WASDE report.

- The March contract closed at 68.50 cents per pound, down 7 points for the week.

- March futures struggled to find news to trade on this week, aside from the WASDE report and Export Sales reports. ICE futures settled at a contract low during the week, with selling pressure likely driven by speculators and grower pricing. Overall, markets were quiet, with limited news to influence trading activity. Cotton’s sessions were marked by two-sided trading days, staying within the range observed in recent weeks. The WASDE analysis below is not part of the weekly market coverage; however, we believe its significance to the market warrants coverage upon its release.

- Open interest increased by 5,150 contracts, bringing total open interest to 243,422.

- Certificated stocks were unchanged at 20,113 bales.

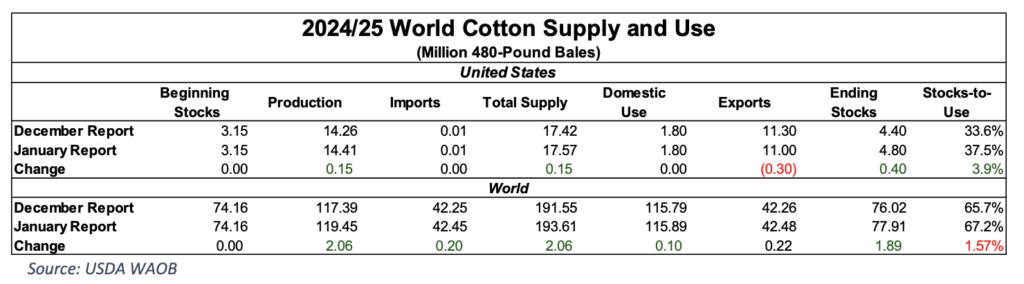

USDA increased U.S. production and ending stocks, both domestically and globally – a bearish outlook for the market.

- U.S. production rose 150,000 bales to 14.4 million, while exports were lowered 300,000 bales to 11 million. These changes flowed into ending stocks, which increased 400,000 bales to 4.8 million. The stocks-to-use ratio is now 37.5%, indicating a loose balance sheet.

- From a production standpoint, the largest increase in the U.S. crop came from the Southwest, which increased 170,000 bales to 4.55 million bales. Texas production increased 200,000 bales to 4.1 million, and Kansas production increased by 10,000 to reach 200,000 bales. However, Oklahoma production decreased 40,000 bales to 250,000.

- On the global front, total use rose by 100,000 bales to 115.89 million, while ending stocks increased by 1.89 million bales to 77.91 million. The world stocks-to-use ratio climbed to 67.2%, relaxing the global balance sheet.

- One noteworthy change was the increase in Chinese production, which grew 1.8 million bales to 30 million. There had been speculation that the crop in China was much larger than what was being reported. At the same time, the country’s imports were lowered 500,000 bales to 8 million bales. China has been noticeably absent from the Export Sales Report this year, and a larger domestic crop has been one of the contributing factors.

Stock markets had a shorter week due to former President Jimmy Carter’s funeral, but minutes from the December Fed meeting and ongoing tariff talks kept them on the defensive.

- The minutes from the Fed meeting were generally hawkish, revealing officials’ concerns about inflation. They noted that uncertainty surrounding trade and immigration policies would lead them to proceed cautiously with interest rate adjustments, indicating that any cuts would be gradual as they assess the situation.

- A potential U.S. port strike that could have disrupted the economy was averted after U.S. dockworkers and shipping companies reached a tentative agreement. Following a brief shutdown in October, months of negotiations were held to prevent another shutdown. While the deal’s specifics were not disclosed at the time, both parties had been working for months to reach an agreement before the January 15 deadline.

- There was positive news on the U.S. jobs front, with the country adding 256,000 jobs, well above the market expectation of 165,000. Stocks got punished, as it reduced the Fed’s potential to lower rates.

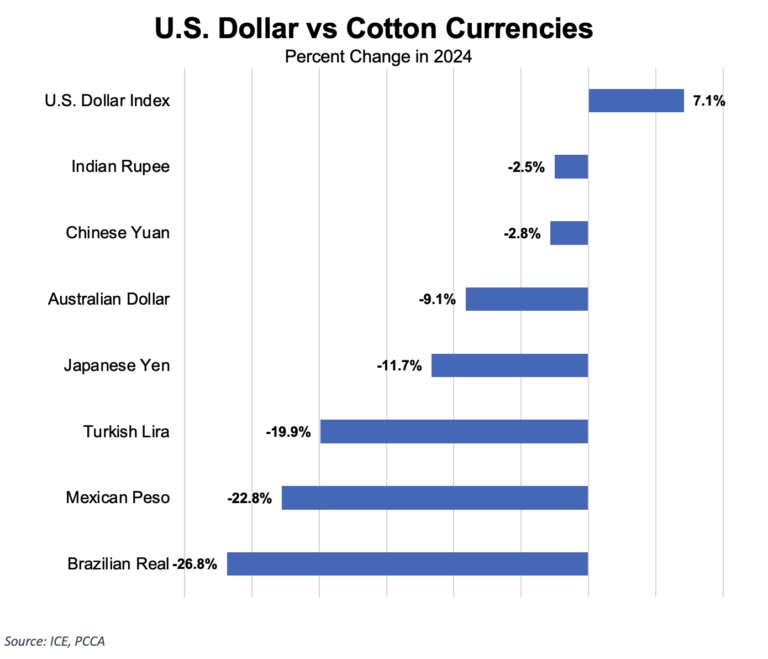

- The U.S. dollar remained strong, continuing to present a headwind for U.S. commodities. A robust dollar makes commodities, particularly cotton, less competitive in the export market. The dollar’s strength against global currencies was supported by U.S. economic strength relative to many other nations and uncertainty regarding the potential impact of upcoming tariffs.

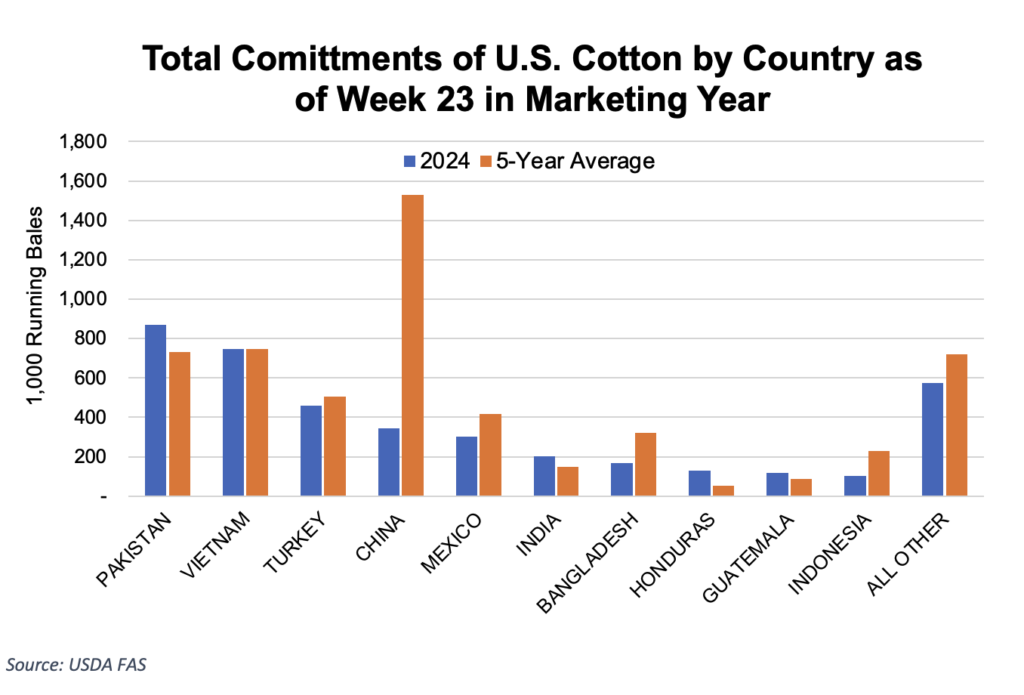

The U.S. Export Sales Report revealed that exporters shipped a marketing year high for the 2024/25 crop.

- For the 2024/25 marketing year, U.S. merchants sold 137,400 Upland bales and shipped 191,700 bales. Shipments have been on the lower end lately, but the pace has gradually picked up now that the holidays are behind us.

- Although sales have been slow, U.S. commitments are consistent with historical trends. The largest importing countries outside China are on track with their typical commitments.

- Pima merchandisers sold 6,400 bales and exported 8,300 bales. Shipments are on pace to reach USDA’s estimate.

The Week Ahead

- Now that the market has new data to trade on, it should be business as usual. Traders will pay attention to the U.S. Export Sales Report and begin to shift their focus toward new crop planting intentions.

- Next week, we will receive the December Producer Price Index (PPI), Consumer Price Index (CPI), and U.S. retail sales readings.

Announcements

- Enrollment for the U.S. Cotton Trust Protocol will be open January 6th- April 30th, 2025. Growers who are currently enrolled will need to renew their membership to continue their involvement in the program.

- New Grower Enrollment for Better Cotton will be open March 3rd-May 30th.

- For assistance or questions about enrolling in these programs, contact PCCA at 806-763-8011.

The Seam

As of Thursday afternoon, grower offers totaled 257,447 bales. There were 38,997 bales that traded on the G2B platform with an average price of 60.88 cents per pound. The average loan was 50.21, resulting in a premium of 10.67 cents per pound over the loan.