Cotton futures remain stuck in the summer doldrums, with trading confined to a narrow range and little fresh news to drive direction.

August 25, 2025

The Week Ahead

This week should be relatively quiet, but still brings key economic updates with July personal income and spending data—featuring the Fed’s preferred inflation gauge, the PCE index. The release comes on the heels of last week’s Jackson Hole meetings, where officials stressed the balance between easing inflation pressures and broader growth risks. Markets are subdued heading into Labor Day, with the next major tests coming from the September 5 jobs report and September 11 CPI. Taken together, these data points and Fed signals could guide expectations for rate cuts and the dollar, with ripple effects across commodities and cotton.

For cotton this week, focus will continue to be on demand and weather. Competition from other growths continues to weigh on U.S. export sales, while heat, dryness, and storm activity in key regions remain important for crop prospects.

Markets will be closed on Monday, September 1, in observance of Labor Day. Our next QuickTake will be released on Tuesday, September 2.

Market Recap

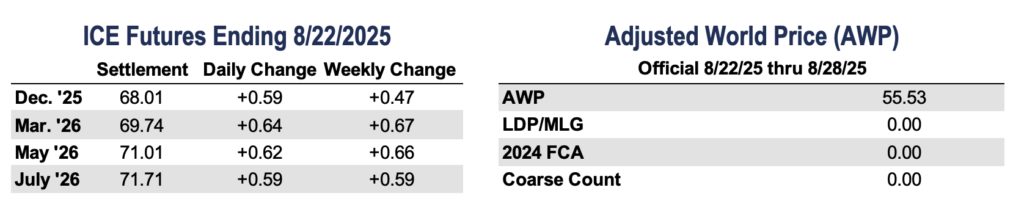

Cotton futures remain stuck in the summer doldrums, with trading confined to a narrow range and little fresh news to drive direction. December futures ended the week at 68.01 cents per pound, up 47 points.

China announced that it will issue 200,000 tons of sliding-tariff cotton import quotas to textile firms, matching last year’s level. The move could create some opportunity for U.S. cotton, though a large share will likely be sourced from other suppliers.

India’s suspension of the 11% cotton import duty last week was initially seen as supportive for U.S. demand, given the pressure from U.S. tariffs on the industry. The impact looks limited, however, unless the exemption is extended, as cotton must arrive in India by September 30, a deadline that’s nearly impossible to meet.

The market continues to wrestle with the significant on-call imbalance, while speculators hold an entrenched short position that has yet to unwind. For now, the technical picture looks flat, leaving the market vulnerable to sharper moves if positioning shifts or demand signals improve. Volume was moderate last week, while open interest rose 3,400 contracts to 242,285. Certificated stocks fell by 1,543 bales to 15,474, the lowest since early May.

Economic and Policy Outlook

Powell’s Jackson Hole remarks on Friday boosted odds of a September cut to 80%, sending stocks higher and the dollar lower. European Central Bank officials, meanwhile, appear comfortable holding rates steady in September, with cuts not expected until December. With U.S. policy shifting dovish and the dollar sliding, commodities and ag markets head into September with a supportive backdrop.

U.S. and EU officials rolled out new details of their trade deal last week, aimed at giving American farm products easier entry into Europe. The agreement lowers tariffs and streamlines certification, though key areas remain unresolved. The changes set the stage for more consistent access to EU buyers and mark an incremental shift in transatlantic trade flows.

Weather and Crop Watch

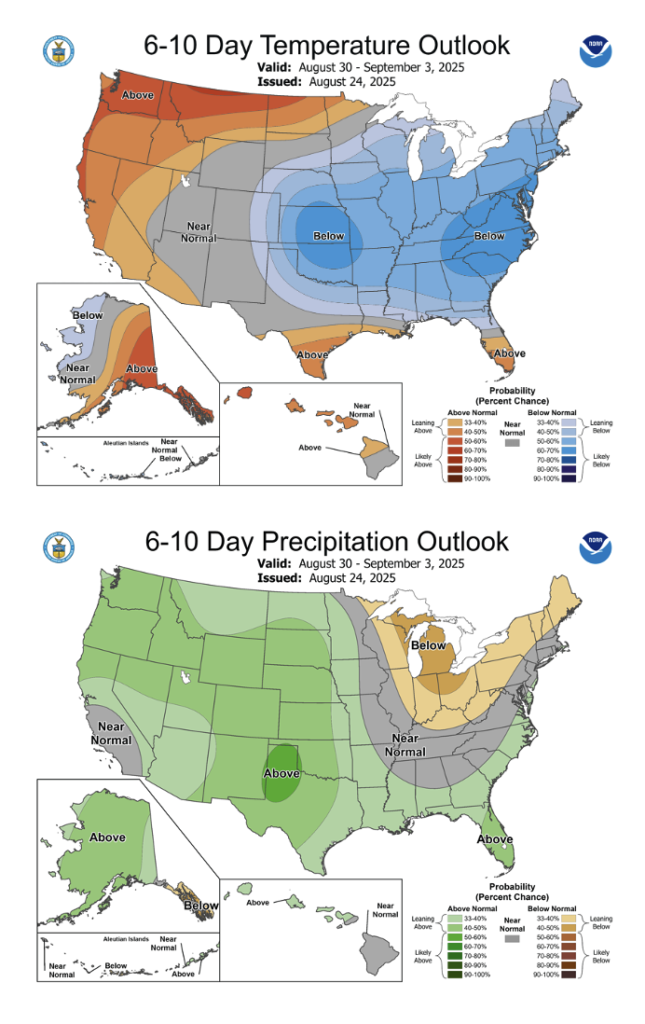

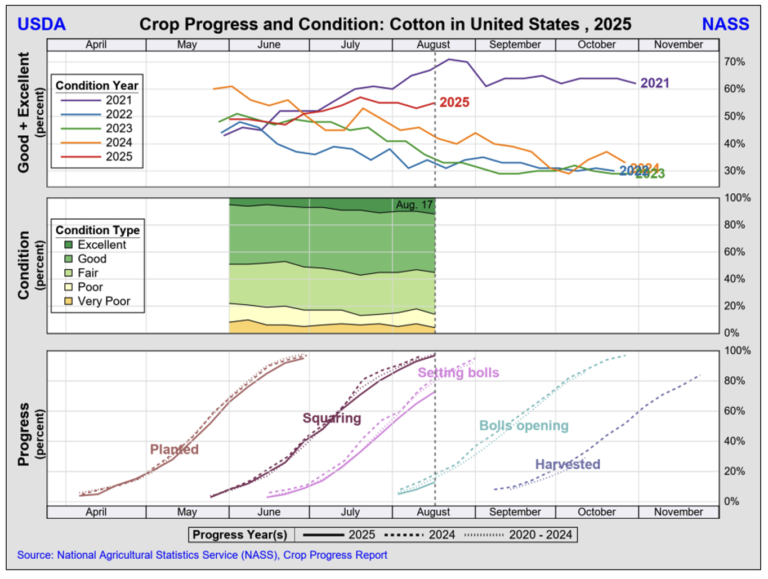

Rainfall eased conditions in parts of the Southern Plains this past week, though many West Texas dryland fields remained patchy and in need of more moisture. Most cotton has now set bolls, with opening just beginning in some areas. As of August 17, crop ratings stood at 49% good to excellent in Texas, 65% in Oklahoma, and 53% in Kansas. Although the Southwest crop is running slightly behind, overall U.S. cotton conditions are the strongest in five years, apart from 2021.

Rainfall brought some relief to parts of the Southern Plains this past week, with some areas picking up more than an inch and scattered showers reaching Central and South Texas. Many acres across West Texas, however, saw only light or patchy rainfall, leaving some areas of dryland cotton still under stress. Looking ahead, widespread showers and thunderstorms are expected throughout the week, with the Panhandle of Texas and Oklahoma likely to see the most improvement, while the driest parts of West Texas may only benefit modestly. Temperatures are set to moderate after recent heat.

Export Trends

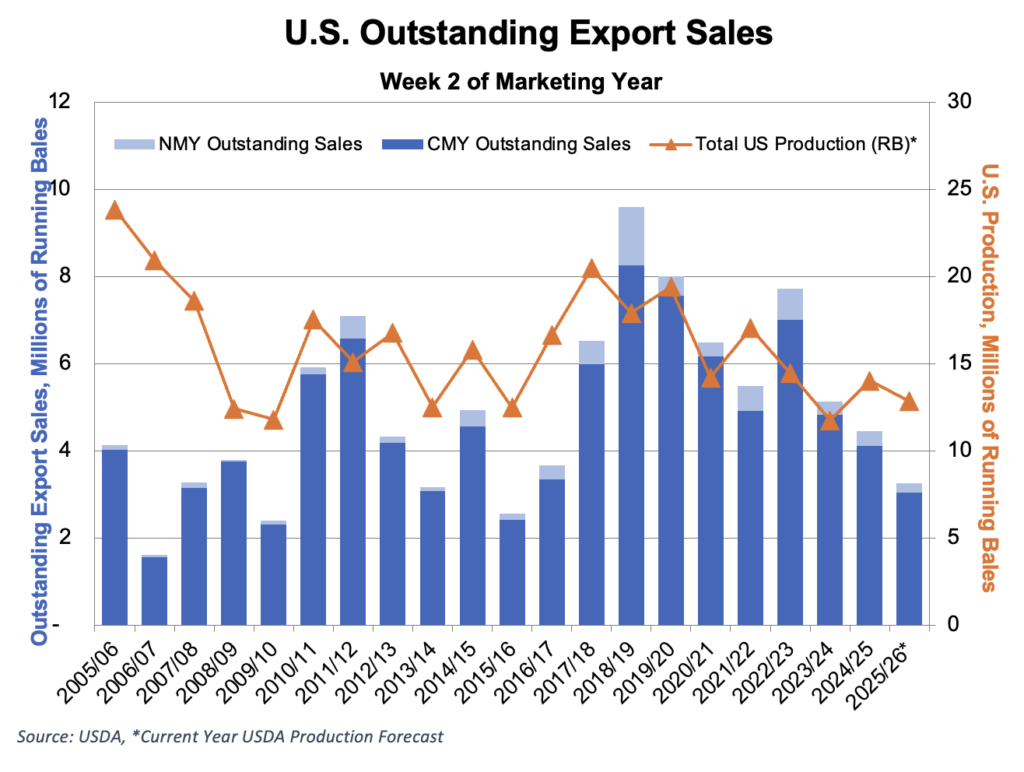

The second week of the marketing year brought softer demand and slower shipments than we usually see for this point in the season, but with limited U.S. supplies on hand, that’s not unexpected. Net sales came in at 105,400 bales, led by Vietnam, Bangladesh, and Pakistan. Interestingly enough, China was missing from the top 20 buyers. Outstanding sales totaled 7,833 bales, reflecting the slow start.

Shipments were lighter this week, with 123,300 bales exported. This is often a quieter stretch, as the market takes a wait-and-see approach while the 2025 crop starts to make its way into the pipeline.

For Pima, new sales totaled 1,000 bales, led by Bangladesh, while shipments reached 4,600 bales.

The Seam

As of Thursday afternoon, grower offers totaled 24,187 bales. There were 2,571 bales that traded on the G2B platform that received an average price of 64.31 cents per pound. The average loan for these bales was 54.86, bringing the average premium received to 9.45 cents per pound.