The holiday-shortened week brought little fresh news, keeping the summer doldrums intact. December futures slipped 51 points to close at 66.03 cents per pound, with trading staying quiet inside the recent range.

The Week Ahead

This week begins with a mixed macro tone, as markets balance last week’s weak jobs report against optimism for a Fed rate cut on September 16–17. A softer dollar outlook and Fed-driven momentum could continue to provide support for commodities. The spotlight is on Thursday’s CPI report, the final key release before the Fed meets. A cooler print likely cements cut expectations, while a hotter reading could raise stagflation concerns.

For cotton, focus stays on demand trends, weather, and Friday’s USDA supply and demand update. Export sales remain a central gauge, with competing growths still weighing on U.S. market share.

Market Recap

The holiday-shortened week brought little fresh news, keeping the summer doldrums intact. December futures slipped 51 points to close at 66.03 cents per pound, with trading staying quiet inside the recent range.

Inquiries for U.S. cotton improved last week, but speculators added to short positions, keeping prices locked in a range. The technical outlook remains flat and vulnerable to sharper moves, while volume stayed light to moderate. Open interest climbed 11,119 contracts to 255,983, and certificated stocks held at 15,474 bales, the lowest since early May.

Economic and Policy Outlook

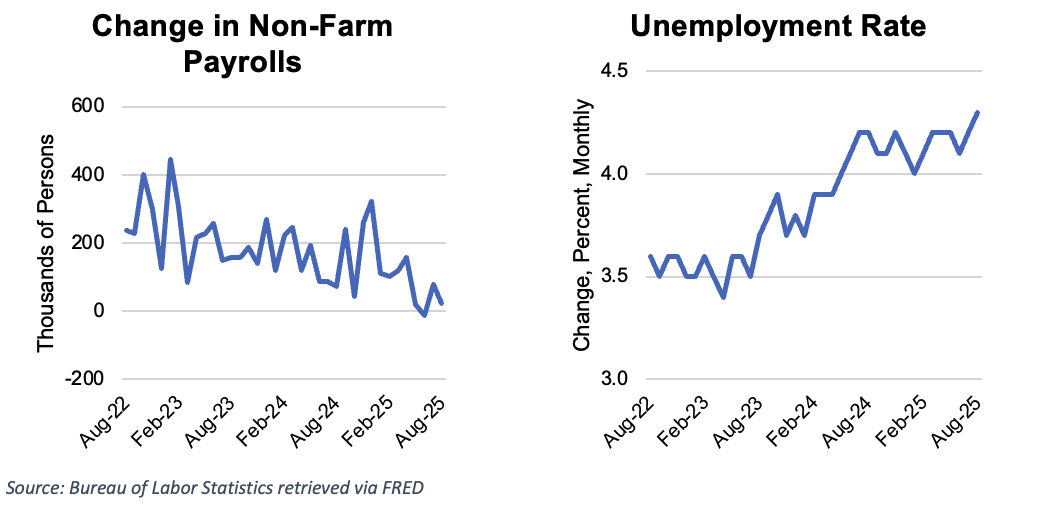

Jobs data U.S. job growth slowed sharply in August, with payrolls up just 22,000 versus expectations of 75,000, while unemployment rose to 4.3%, the highest since 2021. Revisions also showed June employment contracted, underscoring a weakening labor market. The soft report has strengthened expectations for a rate cut when the Federal Reserve meets September 16–17. The report lifted broader markets and weighed on the dollar, a setup that tends to support commodities.

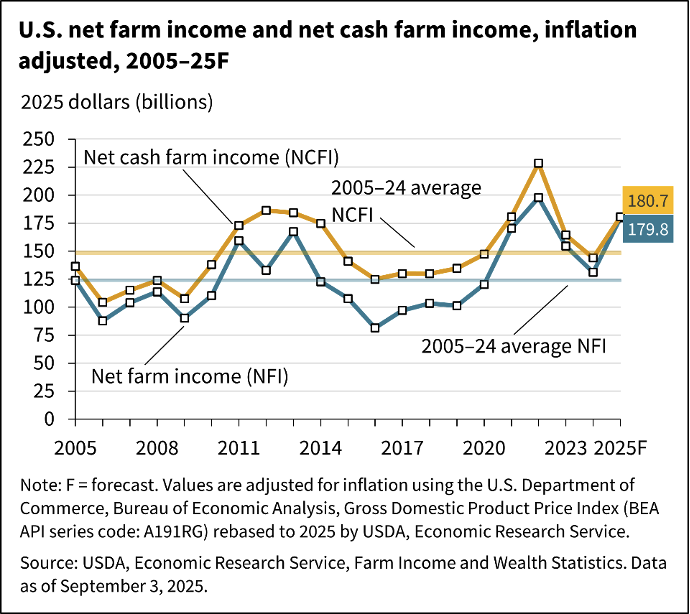

USDA released updated farm income projections showing inflation-adjusted net farm income rising $48.8 billion, or 37.2%, from 2024 to 2025. Net cash farm income is also forecast to climb $36.5 billion, up 25.3% from last year. If realized, both measures would exceed their 2005–24 inflation-adjusted averages. Inflation-adjusted cash receipts are forecast to rise $10.9 billion (2.1%) to $535.2 billion in 2025, though crop receipts will fall $12.3 billion (4.9%). Cotton receipts are expected to hold near 2024 levels at $5.3 billion, reflecting lower prices and higher production costs.

Weather and Crop Watch

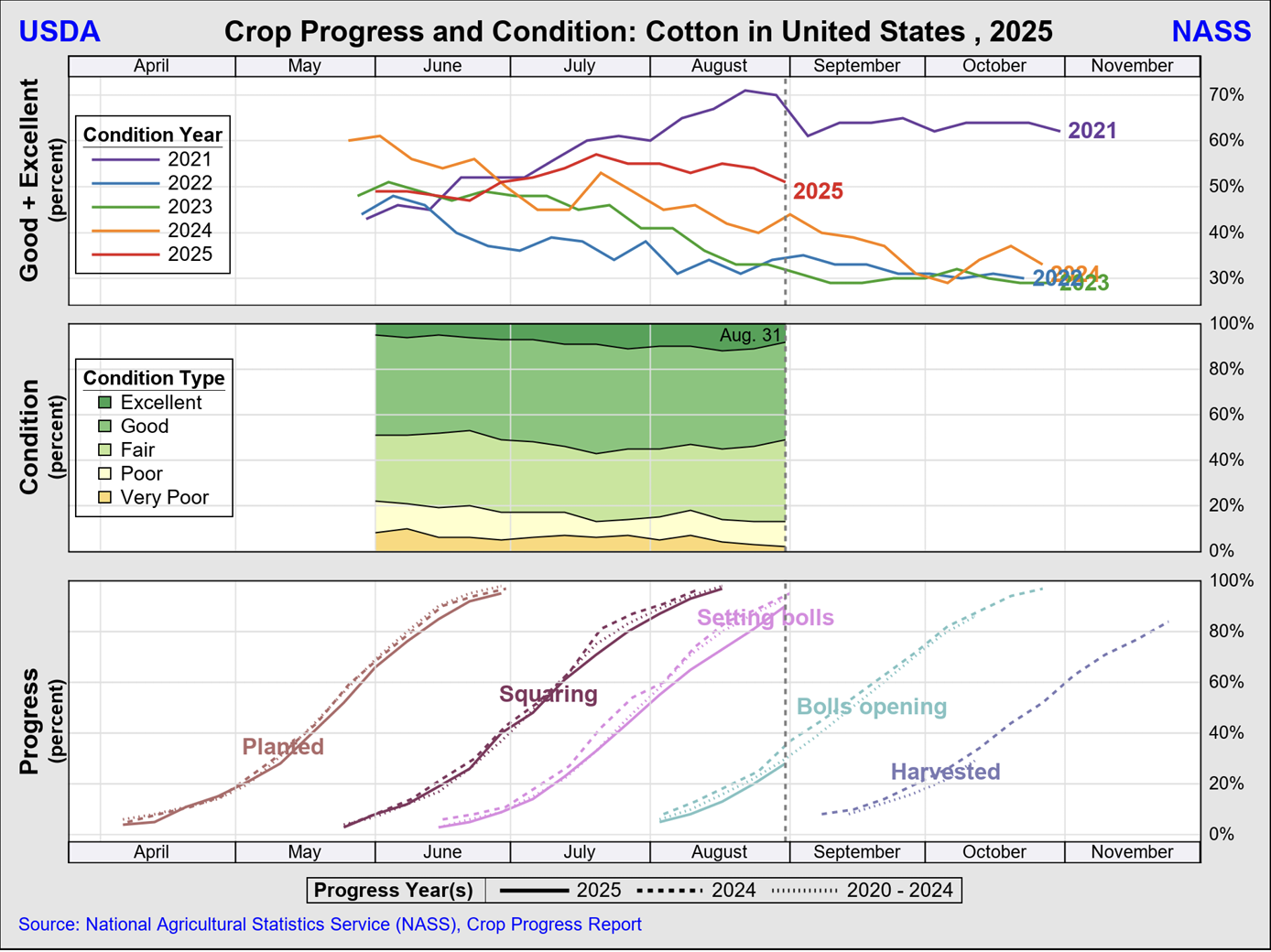

The Southwest was mostly dry this past week with near-average temperatures, leaving overall conditions little changed. For the week ending August 31, ratings improved in Oklahoma to 77% good-to-excellent, while Texas eased to 44% and Kansas held steady at 62%. Boll opening is advancing, with Texas at 28%, Oklahoma at 21%, and Kansas at 16%. In South Texas, harvest is nearly 80% complete, pushing the state total to 11%.

Welcomed Labor Day rains helped the crop across West Texas and southwest Oklahoma, with the best showers hitting around the Panhandle and east of Lubbock. South and Central Texas saw more meaningful moisture, but most spots caught scattered showers. Temperatures ran a bit hotter last week, and the outlook calls for mostly dry weather through late September, aside from a few stray showers. Cotton is progressing well overall, though the drier areas may start to feel some stress.

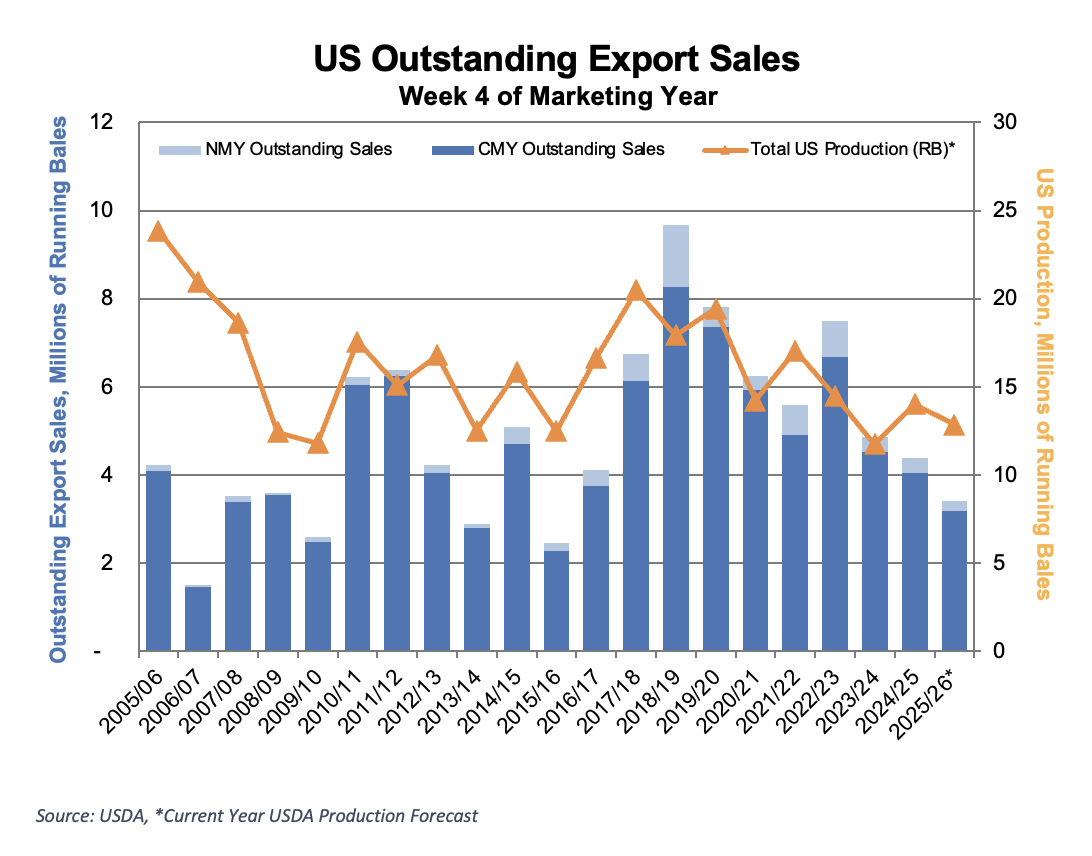

Export Trends

Export sales were solid this week, a healthy pace for late August. For the week ending August 28, net Upland sales totaled 245,000 bales, led by Vietnam, India, China, and Bangladesh. Notably, after quieter weeks, China was back in the market, booking 35,000 bales and rejoining the list of top 20 countries with commitments from the U.S.

Shipments reached 154,700 bales, again lagging seasonal norms. Vietnam took the bulk of shipments at 82,800 bales, followed by Pakistan, Mexico, Honduras, and India. This slowdown reflects the limited volume currently moving into the U.S. supply chain, with South Texas as the only region harvesting in meaningful quantities and little carryover from the 2024 season.

For Pima, new sales totaled 1,600 bales, led by India and Peru, while shipments were light at 4,400 bales.

The Seam

As of Thursday afternoon, grower offers totaled 22,362 bales. There were 2,011 bales that traded on the G2B platform that received an average price of 63.62 cents per pound. The average loan for these bales was 56.31, bringing the average premium received to 7.31 cents per pound.