At a Glance

- Cotton acreage declining 3.2% to 9.0 million acres nationwide.

- Mid-South region faces steepest decline at 20.6% reduction rate.

- World cotton consumption expected to increase 1.0% in 2026.

The U.S. cotton industry is poised for a dynamic year in 2026, as producers navigate economic pressures, shifting planting intentions, and evolving global market conditions. Based on information released during the National Cotton Council Annual Meeting held, February 9 to 12 in San Antonio, Texas, data reveals a complex landscape shaped by market forces, weather conditions, and geopolitical uncertainties.

Planting Intentions for 2026: A Decline in Cotton Acreage

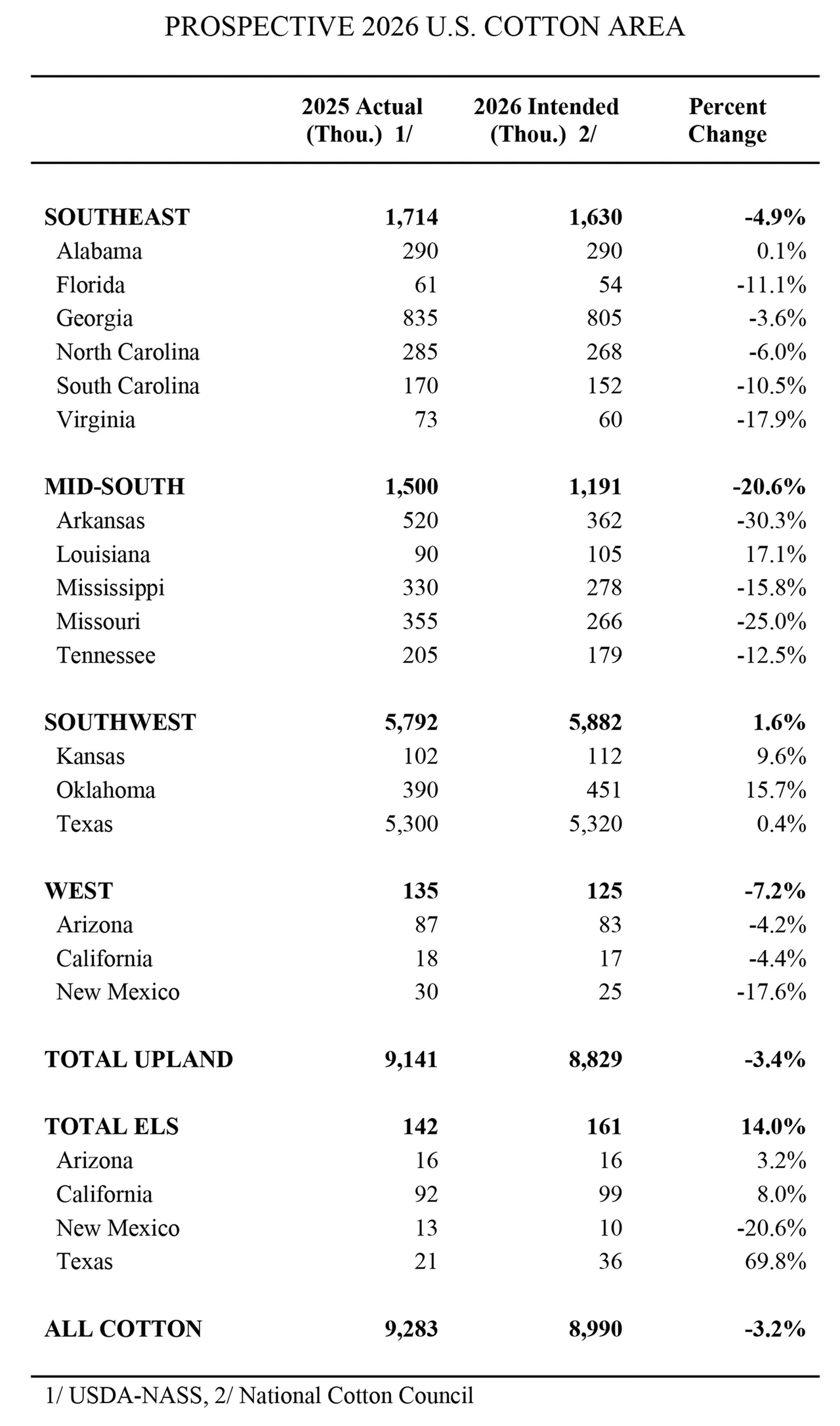

According to the NCC’s 45th Annual Early Season Planting Intentions Survey, U.S. cotton producers plan to plant 9.0 million acres of cotton in 2026, representing a 3.2% decrease from 2025.

This decline reflects the economic realities of growers who are grappling with low prices, high production costs, and weak demand, according to the NCC.

The survey, conducted in January 2026, collected responses from producers across the 17-state Cotton Belt, providing a snapshot of planting intentions based on market conditions at the time.

Regional trends in cotton acreage

The survey results highlight significant regional variations in planting intentions:

Southeast: Cotton acreage is expected to decline by 4.9% to 1.6 million acres. While Alabama growers anticipate a slight increase of 0.1%, other states in the region, such as Florida (-11.1%), Georgia (-3.6%), and Virginia (-17.9%), report notable decreases. The decline is attributed to increased planting of corn, soybeans, and other crops.

Mid-South: This region is projected to experience the steepest decline, with cotton acreage dropping by 20.6% to 1.2 million acres. Arkansas leads the decline with a 30.3% reduction, while Louisiana stands out with a 17.1% increase in cotton acreage.

Southwest: In contrast to other regions, the Southwest is expected to see a 1.6% increase in cotton acreage, driven by gains in Kansas (+9.6%), Oklahoma (+15.7%), and Texas (+0.4%). Producers in this region are shifting away from crops like wheat and sorghum to focus more on cotton.

West: Upland cotton acreage in the West is projected to decline by 7.2%, with decreases in Arizona (-4.2%), California (-4.4%), and New Mexico (-17.6%). However, extra-long staple (ELS) cotton acreage is expected to rise by 14.0%, with Texas leading the increase (+69.8%).

Economic pressures and market dynamics

Dr. Jody Campiche, NCC’s Vice President of Economics & Policy Analysis, emphasized that planted acreage is only one factor influencing cotton supplies.

Weather and agronomic conditions will play a critical role in determining crop size. Based on average abandonment rates and yields, the Cotton Belt harvested area is estimated at 7.1 million acres for 2026, with a projected crop of 12.7 million bales. This includes 12.3 million upland bales and 393,000 ELS bales.

The survey also revealed that U.S. farmers respond to relative prices when making planting decisions. During the 2026 survey period, cotton prices were nearly unchanged compared to 2025, while corn prices were slightly lower and soybean prices slightly higher. These price dynamics influenced planting intentions, with growers opting to diversify their crop portfolios.

Global Economic Outlook and Trade Implications

The NCC’s economic outlook for 2026 underscores the challenges facing the U.S. cotton industry, according to Campiche. While an improvement in world cotton demand is anticipated, potential changes in trade policy and geopolitical tensions have created significant uncertainty.

Stable to slowing economic growth is projected globally, which could impact cotton consumption and trade.

World cotton consumption is expected to increase by 1.0% to 120.0 million bales in 2026, driven by expanded consumption in key importing countries. However, world production is estimated to decline to 114.1 million bales due to lower harvested acreage and yields.

This imbalance between consumption and production is projected to result in a decline in world ending stocks to 69.8 million bales, the lowest level outside of China since 2016.

For the U.S., higher export projections and lower ending stocks could provide some price support. U.S. mills are expected to consume 1.55 million bales in 2026, slightly down from 1.60 million bales in 2025. The export-oriented nature of the U.S. cotton industry means that tariff policies and trade agreements will play a crucial role in shaping the market landscape.

Opportunities amid challenges

Despite the economic pressures, declining stocks in the 2026 balance sheet could offer some relief for prices, according to the NCC. If world consumption can overcome headwinds from the sluggish global economy and competition from cheaper man-made fibers, the U.S. cotton industry may find opportunities for growth.

Producers will continue to monitor changes in commodity prices and input costs before finalizing their planting decisions.

The NCC’s analysis highlights the resilience of U.S. cotton growers as they adapt to changing market conditions. While the industry faces uncertainties, the projected increase in world consumption and trade offers hope for a more favorable economic environment.