Naomi Blohm, senior market adviser, Total Farm Marketing by Stewart Peterson

At a Glance

- Ample U.S. and global cotton supplies suppress prices.

- Major weather issues could shift the price narrative.

- Monitor planting trends and global production closely.

Cotton prices have fallen dramatically since their price peak in 2022. Is there any hope of a price increase for 2026? Or will the dominant theme of ample supplies keep prices in check?

What’s happened

To respond to a request for a recent speaking engagement, I sought current information regarding the overall tone of the U.S. farm economy. If you are part of agriculture, you already know the answer to that question: The U.S. farm economy is struggling.

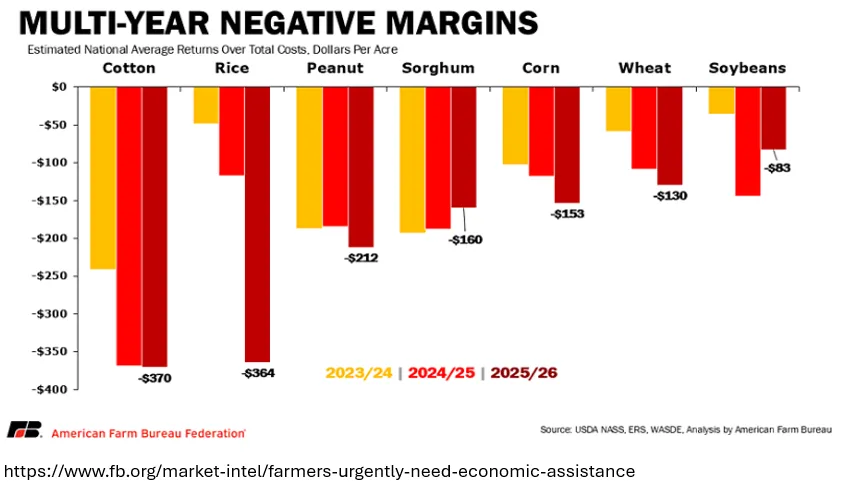

What really caught my eye was a chart compiled by American Farm Bureau that showed how over the past three years, seven different crops (corn, soybeans, wheat, sorghum, peanuts, rice and cotton) showed multi-year negative returns.

What was eye opening for me was the staggering losses for cotton. Thus, the topic of this week’s blog. What has been fundamentally happening in cotton over the past three years?

From a marketing perspective

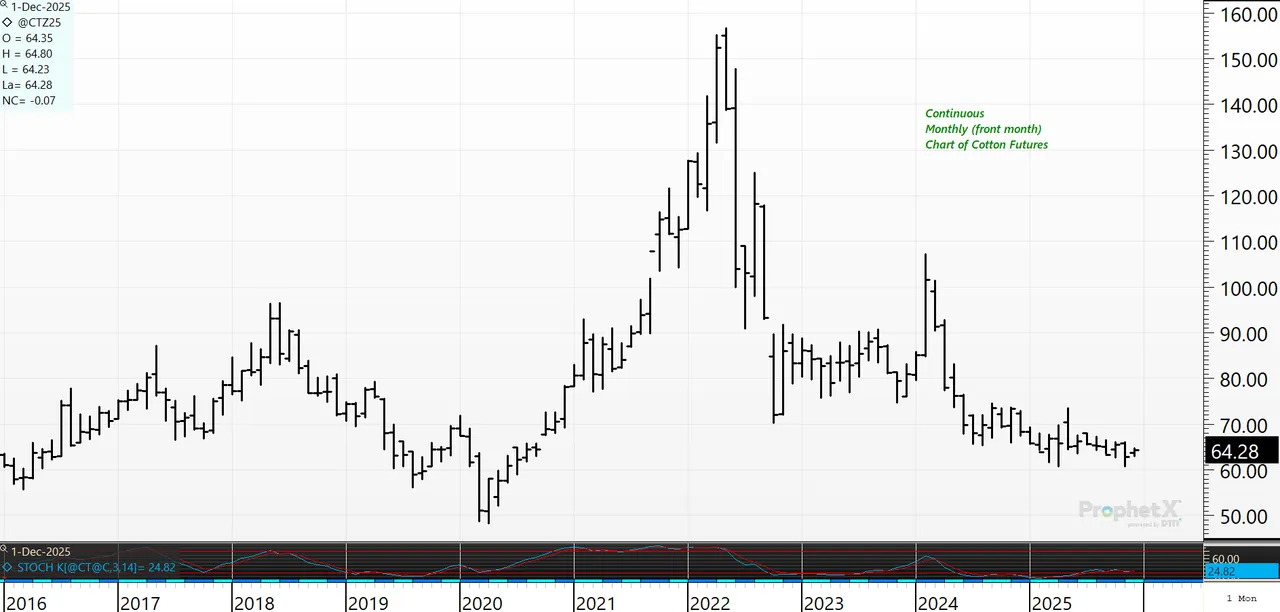

First, let’s take a look at the price of cotton futures over the past decade. From 2016 until 2019, cotton futures traded in a modest range of 60 cents/lb. to 90 cents/lb. COVID-19 struck in 2020, and the demand-loss fear allowed for cotton futures to sink to 48.35 cents/lb.

Coming out of COVID-19, a pickup in global demand followed by the commodity-wide buying spree by managed money investors throughout 2021, led cotton prices to peak at a staggering 156.64 cents/lb in 2022. That was shortly after Russia invaded Ukraine and cotton was one of many commodity grain and oilseed markets to peak at that time. Since then, prices retreated and are now dramatically lower, with current cotton futures trading near 64 cents/lb.

Next, let’s do a simple break down of the supply and demand fundamentals that have occurred in the United States over the past three years. Following the price spike in 2022, U.S. planted acres of cotton increased, with yields proving to be viewed as quite sufficient. Production met demand needs. Ending stocks began to increase.

For the 2023-24 crop year, U.S. cotton ending stocks came in at 3.15 million bales. (Bales each weigh 480 pounds). For the 2024-25 crop year, U.S. cotton ending stocks had a large increase, now pegged at 4 million bales. And according to the most recent USDA WASDE report, cotton ending stocks for the 2025-26 crop year are projected to be even higher, at 4.5 million bales. Perception of ample supplies usually correlates with lower prices.

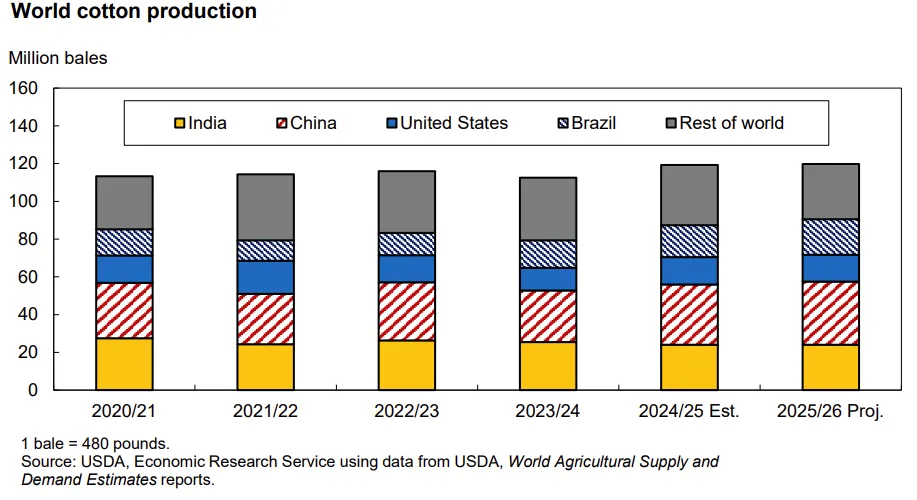

Finally, let’s do a simple breakdown of the global supply and demand fundamentals over the past three years. The theme is the same: Higher prices in 2022 led to an increase in global production, which lead to an increase in global ending stocks over the past three years.

Sufficient U.S. supplies and sufficient global production. That theme may likely carry over into early 2026 and could keep cotton futures prices on the defensive.

Prepare yourself

The reality is that it would take a major weather issue in one or two of the top growing countries to change the narrative for cotton futures in 2026.

India and China grow much of the world's cotton and use nearly everything they grow for domestic needs. Brazil and the United States are the next largest producers of cotton, and export most of their crops.

Will continued low prices mean less planted U.S. cotton acres in the spring? Will Mother Nature have an adverse weather surprise in store for 2026? How long will cotton prices stay suppressed in 2026?

Reach Naomi Blohm at 800-334-9779, on X: @naomiblohm, and at naomi@totalfarmmarketing.com.

Πηγή: farmprogress.com