Cotton prices were quiet this week, drifting in narrow ranges as traders awaited fresh direction from Friday’s WASDE. Light volume, steady crop conditions, and subdued demand kept the market in a holding pattern. With broader markets rallying and fresh data in hand, will cotton prices start to move with more conviction? Get QuickTake’s read on the week’s events in five minutes.

The summer doldrums have set in, and the cotton market is treading water ahead of the July supply and demand update.

- December futures closed at 67.73, sliding a marginal 73 points for the week.

- As summer trading patterns set in, cotton prices drifted in narrow ranges this week. December futures swung between small gains and losses, weighed down by light volume and a lack of clear direction. The latest Cotton On-Call report showed the unfixed sales imbalance widening again, while the Commitments of Traders report pointed to continued spec short covering. The market was in wait-and-see mode ahead of Friday’s WASDE, with traders watching how USDA accounts for larger acreage, improving crop conditions, and what that means for production estimates.

- Trading volume was light this week, with Thursday marking the smallest daily volume of 2025. Open interest rose by 4,359 contracts to 206,231, while certificated stocks dropped 4,977 bales to 35,347, the lowest level since May.

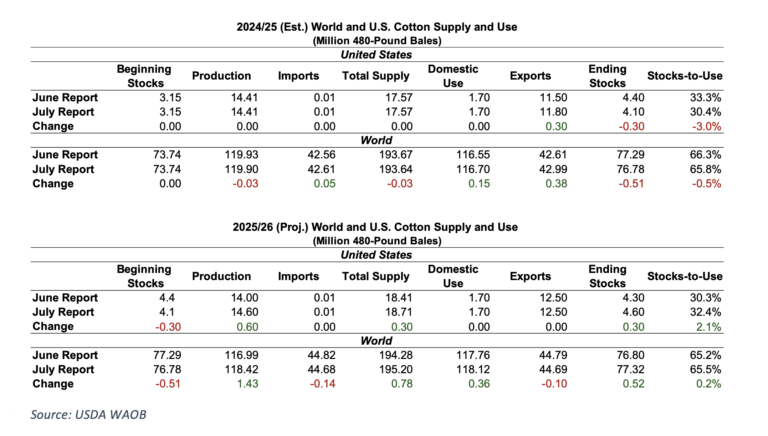

The July WASDE offered a modestly more bearish tone, raising U.S. cotton production and global stocks for 2025/26. While no major surprises emerged, the shift toward higher output and inventories reinforces a well-supplied outlook heading into the new crop year.

- For 2025/26, U.S. production was increased by 600,000 bales to 14.6 million, driven by higher harvested acreage and reduced abandonment in the Southwest. Beginning stocks were trimmed 300,000 bales following an upward revision to 2024/25 exports. With use unchanged, ending stocks rose to 4.6 million bales, lifting the stocks-to-use ratio to 32.4%.

- Globally, 2025/26 production rose 1.43 million bales to 118.42 million, led by China, the U.S., and Mexico. Consumption was raised slightly to 118.12 million bales. The net effect was a 520,000-bale increase in world ending stocks, which now stand at 77.32 million bales. China’s import forecast decreased 700,000 bales to 5.8 million, while Brazil’s export outlook remained firm at 14.3 million.

- For 2024/25, U.S. exports were lifted by 300,000 bales to 11.8 million, cutting ending stocks to 4.1 million. World consumption saw minor upward adjustments to 116.65 million bales, while ending stocks declined to 76.78 million. Overall, the report showed encouraging signs for demand, but was underscored by ongoing supply-side pressure heading into the new crop year.

Broader markets notched all-time highs, shrugging off familiar tariff tensions thanks to strong earnings and firm Treasury auction demand.

- Markets rebounded this week, with the S&P 500 and Nasdaq hitting fresh record highs, boosted by strong earnings from tech giants like Nvidia, which briefly topped a $4 trillion valuation even as trade tensions persisted. Investors shrugged off new tariff threats, helped by solid demand in the 30-year and 10-year Treasury auctions.

- The One Big Beautiful Bill Act (OBBBA), signed into law by the Trump administration on July 4, delivers broad reforms across tax, social, and agricultural policy. For farmers, it represents the most substantial overhaul of the farm safety net in over two decades.

- For cotton, key provisions include a 14% increase in the Seed Cotton Reference Price to $0.42 beginning with the 2025 crop and a higher upland marketing loan rate of $0.55 starting in 2026. The bill preserves existing base acres and offers a one-time allocation of up to 30 million new acres for qualifying producers. It also ends the global de minimis import provision in 2027 and permanently extends the Section 199a pass-through deduction.

- The White House extended the tariff pause to August 1, allowing more time for negotiations before new duties take effect. A second wave of tariff letters went out this week, targeting countries with rates up to 30% and confirming a 50% copper tariff. Brazil was warned of a 50% tariff, escalating trade tensions. While impacted countries race to finalize deals, the administration has hinted at flexibility. Markets largely shrugged the news off late in the week, but uncertainty persists.

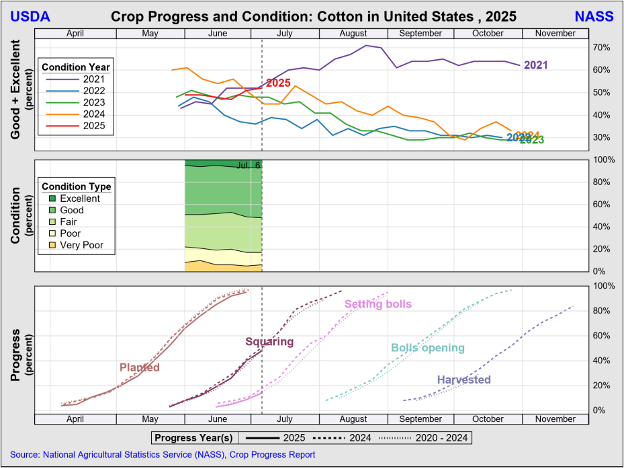

Crop development in the Southwest is progressing, though overall U.S. progress remains slightly behind average.

- In Texas, 40% of the crop is squaring and 15% is setting bolls. Oklahoma is 24% squared, and Kansas is 30% with 4% setting bolls. Crop conditions improved two percentage points in Texas to 42% rated good to excellent and rose six percentage points in Kansas to 37%, while Oklahoma declined seven percentage points to 60%.

- Scattered showers brought light to moderate rain across West Texas, the Panhandle, Blacklands, and Coastal Bend. Temperatures were seasonable, with highs in the 80s and 90s and lows mostly in the 60s and 70s. The two-week outlook is mostly favorable. Isolated to scattered showers are expected most days. Dry, warmer weather later this month should aid development of late-planted fields.

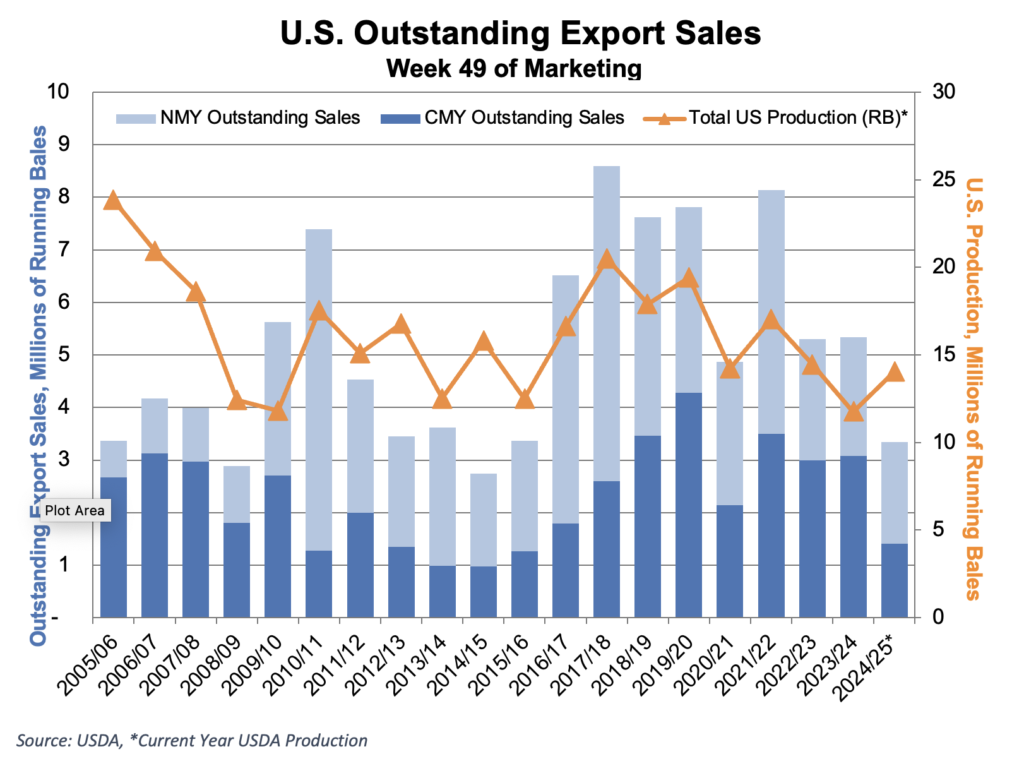

U.S. export sales were solid for the current crop year, but average for the next.

- Net Upland sales for the current crop totaled 75,100 bales, led by Vietnam, Pakistan, India, and Turkey. While Bangladesh posted notable cancellations, some appear to have been shifted to the next marketing year. New crop sales were average at 81,500 bales, up from the prior week, with demand from Bangladesh, Vietnam, South Korea, and Mexico.

- Export shipments remained strong at 240,900 bales, above average and still outpacing the weekly pace needed to reach USDA’s 11.5 million bale export forecast, which requires about 125,000 bales per week.

- Current crop Pima sales reached 3,400 bales, and 2,600 bales were sold for new crop. While sales were modest, shipments hit a marketing year high of 17,600 bales.

The Week Ahead

- Now that the July WASDE is out, the cotton market has fresh data to trade on heading into next week. Focus will shift to Monday’s Crop Progress and Condition Report, followed by Thursday’s Export Sales. Broader markets will watch Tuesday’s Consumer Price Index (CPI), Wednesday’s Producer Price Index (PPI), and Thursday’s retail sales for clues on inflation trends and consumer demand.

The Seam

- As of Thursday afternoon, grower offers totaled 29,863 bales. There were 1,442 bales that traded on the G2B platform that received an average price of 64.98 cents per pound. The average loan for these bales was 52.28, bringing the average premium received to 12.70 cents per pound.