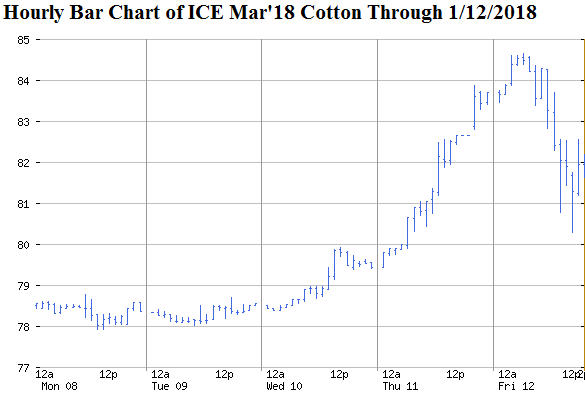

The week ending January 12 saw old crop ICE cotton futures breach 80 cents on the way to three successive days of contract highs. The trading in the latter part of the week was in very high volume and increasing open interest — an indicator of more new buying. ICE cotton futures declined after the release of a neutral WASDE report that perhaps disappointed bulls looking for confirmation of expected fundamentals. Fundamental news this week also included a good export sales and shipment numbers, especially considering the expected demand response to rising prices and the already high seasonal pace of total commitments. Chinese cotton futures were higher this week while world prices were more mixed.

{kind=link}

Mar’18 cotton settled the week at 81.68 cents per pound. The May’18 and Jul’18 contracts settled 28 and 54 points higher, respectively. These futures spreads are insufficient to cover the cost of storing cotton, e.g., May’18 would need to exceed Mar’18 by at least 150 points. There is certainly little market signal to store 2017 bales in hopes of higher prices, except for contingency purposes (what an economist would call “convenience yield”). The simplest interpretation of market signalling is that if you have at least base grade quality cotton, sell it. And if deeply discounted cash bids on your 2017 bales cause you to choke, ask yourself whether it will be any better after a few months of storage and who-knows-where price changes.

The old crop contracts remained inverted above Dec’18 which settled at 75.34 cents per pound on Friday January 12.

A sample of option prices on ICE cotton futures saw some changes from the previous week because of the rise in the underlying futures. On Thursday January 11, deep in-the-money 73 call options on Jul’18 ICE futures were worth 11.12 cents per pound; recently (and unexpectedly) in-the-money 79 calls on Jul’18 were worth 7.03 cents. An at-the-money 75 put option on Dec’18 cotton cost 4.33 cents per pound on Thursday, while deeply out-of-the-money 65 put on Dec’18 cost 0.81 cents.

This market is being supported by evidence of improving demand fundamentals, and a lot of speculative buying. The is supported by continuing strong pace of U.S. export commitments and the eventual influence of large mill fixations. But there is also a risk to see futures weaken or even crash if the hedge funds get spooked by some risk-off event, and/or if seasonally high U.S. exports turn out to be just a front-loaded pattern of what USDA has already been expecting. Remember, the current fundamental picture painted by USDA still implies price weakness by virtue of a large year-over-year increase in ending stocks. In the short run, the potential for a price reversal is also there because of the fickle fuel of speculative buying that underlies the rally since November.

Given all these uncertainties, growers should consider taking advantage of the present (or future) rallies, and protect themselves from sudden sell-offs. Forward contracting, immediate post-harvest contracting, and/or various options strategies can be used to limit downside risk while retaining upside potential. In hindsight, contracted 2017 bales could have been combined with call options on the deferred futures contracts. Unginned 2017 bales could be covered with put options on Mar’18. New crop put spread strategies to hedge the 2018 crop have become increasingly affordable with the rise in the underlying futures contract.

Πηγή: The Cotton Marketing Planner