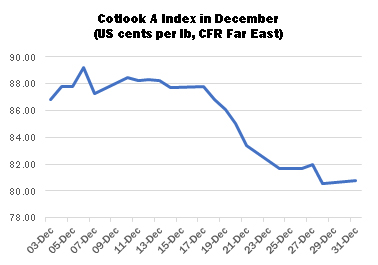

International cotton prices fell sharply further during December, which saw the Cotlook A Index decline to its lowest point of the 2018 calendar year. At the end of the month, the Index was hovering just over the threshold of 80.00 cents per lb, having lost nearly seven percent of its value during the month and over 20 percent since its high point in mid-June.

The decline in prices followed a sudden downward move in New York futures around the middle of the month. In six consecutive sessions of decline, the March contract lost more than seven cents, before regaining a measure of stability toward the end of the month. No single explanation for the abrupt downturn could be identified, but external macro-economic factors — slowing growth and the unresolved Sino-US trade issues — were given greater weight by most analysts than cotton fundamentals. The second of those factors has of course also had direct implications for US exports, since in early July China placed an additional import tariff of 25 percent on US cotton, resulting in a moderate volume of cancellations of US export sales to that market.

Following a hiatus of several months, in December China’s customs authorities began once again to provide import data broken down by origin. During the first four months of the international statistical season, China imported close to 540,000 tonnes of raw cotton, substantially more than during the same period a year earlier. Australian accounted for some 46 percent of imports during the four-month period, followed by US and Brazilian (around 13 percent each) and Indian (11 percent). During the corresponding period a year earlier, US cotton had claimed nearly 27 percent of Chinese imports.

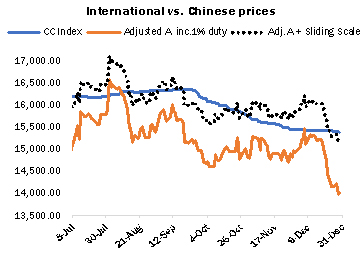

Fresh Chinese import demand remained lacking during most of December, though reports in circulation late in the month suggested that lots held on consignment had been traded more actively. For most of the period, the relationship between local and international prices provided little incentive to purchase foreign cottons against the additional 800,000-tonne import quota (subject to a sliding scale of import duty) available in recent months. A more than adequate local supply also tended to militate against import buying: a substantial volume was carried over from the previous domestic crop and by late December the bulk of the 2018/19 output had been ginned.

Mill demand from virtually all import markets remained very slow during the first half of December, but the sharp fall in offering rates during the second half of the month prompted a significant upturn in buying interest, in particular from the Indian subcontinent. US cotton appears to have been the major beneficiary, as demand has focused largely on the plentiful lots that have this season been discounted for quality. To the frustration of market observers, however, the volume of recent US turnover cannot yet be quantified, since USDA’s weekly export report has fallen victim to the partial government shutdown. The Department’s World Agricultural Supply and Demand Estimates are unlikely to be released in January.

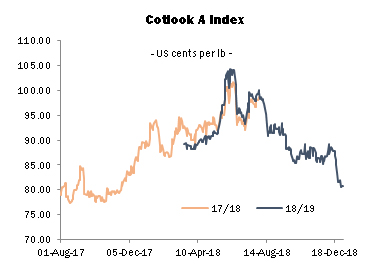

In late February, Cotton Outlook will publish initial forecasts of world production and consumption during the 2019/20 season. As always, these forward assessments are of a very tentative nature. Until recently, the expectation had been that the firmness of international prices would provide a strong stimulus to cotton plantings in the Northern Hemisphere. As measured by the A Index, world values by the end of December remained above their nominal long-term average, though by a much smaller margin than earlier in the year. The latest downturn in the market may therefore prompt some farmers to reassess their choice of crops for the season ahead.

The demand side of the balance sheet appears no less uncertain. Over recent months, Cotton Outlook’s forecast of global consumption has been reduced substantially, to reflect both spinners’ difficulty in maintaining acceptable margins and some of the broader influences alluded to above. Most commentators see only limited grounds for optimism with regard to the economic prospects for 2019.

Πηγή: cotlook.com