For at least a few reasons discussed here, 2019 will shape up to be an important and pivotal year for many farms and cotton growers. A lot has happened, more will happen, and the economy on the farm is wrought with uncertainties.

Market Situation. The new crop December futures price is challenging support at the 72 to 73 cent area. After hanging around 74 to 75 cents for a while, prices are showing additional weakness. December futures at 73 cents or less excites no one that will be growing cotton this year. But we are reminded that December 2018 was at 76 cents this time last year. December 2018 eventually went to over 90 cents, and no one saw that coming at the time.

No one is suggesting that the 2019 crop will follow a similar pattern. For various reasons, it likely will not, and the recent weakness adds more concern. But set your price targets/goals and take action when the market gets there. December 2019 currently suggests targets at 76-78 cents and 79-82 cents above that. For the 2019 crop, attention should be focused on managing downside risk, even more-so than usual.

On February 9, the National Cotton Council released the results of its annual acres planted survey. That survey suggests a 2.9% increase in cotton acres this year and a likely crop of 23 million bales, compared to 18.4 million bales for 2018.

Growers care about price among other things. What implications does a potentially much larger crop have? Assuming this increase in acreage and production materializes, how is the market going to react to roughly a 4 ½ million bale larger U.S. crop? Will 73 to 74 cents hold? Talk is beginning to circulate about something in the 60s. We all know that price will ultimately be determined, in part, by yield and acres harvested.

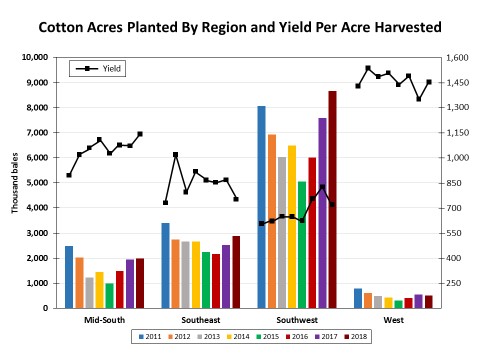

Acres and Yields. The 2018 season saw increased acres planted in three of the four regions. Yields dropped in the Southeast and Southwest. Acres planted have been less variable in the Southeast and Southwest. This means that in both regions, cotton has a larger foundational percentage of acres that are very likely to remain in cotton almost regardless of market forces.

Prices for competing crops such as corn and soybeans (and peanuts in peanut-producing states) certainly have an impact on cotton acres – but less so in the Southeast and Southwest compared to the Mid-South.

Ok, so what does all this mean? It means that for a lot of land and for a lot growers, most cotton acres stay in cotton and growers stick with rotations and just have to roll with the punches handed out by the market. Yes, some acreage will be tweaked based on market signals, but the degree to which that happens varies by region and even by state within a region.

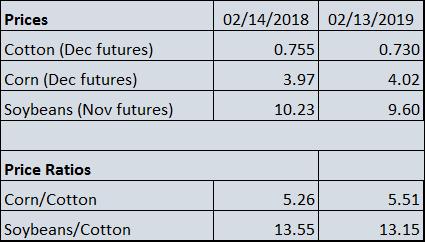

Prices and Price Ratios. Prices can give us a hint as to what direction farmers might go when tweaking acres. It is relative prices – how prices compare to each other that matters, not a single price itself.

With cotton, we have to be careful, because when the price of cotton is low (around 60 cents and less), the market signal no longer matters because loan program LDPs and MLGs will kick in to insulate the farmer from low prices.

Compared to last season at this time, the corn/cotton price ratio has increased. This means that, compared to cotton, the price of corn is higher than at this time last year. The soybean/cotton ratio has declined. The price of soybeans, compared to cotton, is lower than last year.

Early thinking is that corn will gain some ground, but soybeans will lose some ground to cotton. This can and will change. Last year, cotton went to the 80-cent level during planting time. Corn went to over $4.00 during planting time.

Effective last crop year, generic base and its temporary base provisions are eliminated. Plant for the market. Generic base, along with the attractive PLC Reference Price for peanuts, resulted in higher peanut acreage during the 2014 farm bill years. Peanut acreage declined sharply last year with the elimination of generic base. Peanuts acres could increase this year at the expense of cotton – if cotton moves below the low 70s and/or if peanut contracts are higher than $400 per ton.

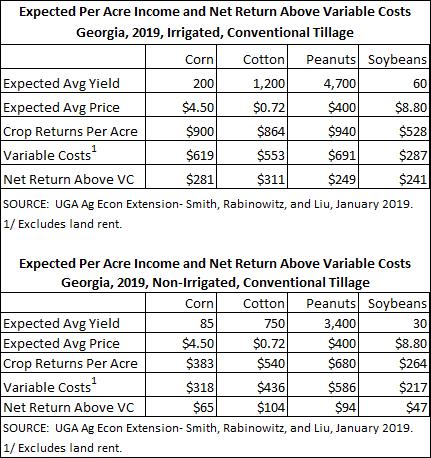

Comparative Net Returns. University of Georgia income and cost estimates for 2019 show cotton with the highest expected net return per acre in both irrigated and non-irrigated production. This is based on the price, yield, and costs assumed.

Yields and costs will vary for your area and your farm. These estimates are just examples. It’s interesting and useful to do a little “sensitivity analysis.” For example, for non-irrigated production, if the price of cotton drops more than 1.3 cents, peanuts at $400 per ton would offer higher net return ($104 – $94 = $10 per acre / 750-lb cotton yield = $0.013). Alternatively, peanuts at more than $406 per ton would provide higher net return than 72-cent cotton ($104 – $94 = $10 per acre / 3,400-lb peanut yield x 2,000 lbs = $6 per ton more needed.

Several factors are negatively impacting cotton’s competitiveness. The price/value received by the farmer for cottonseed has declined sharply in the past couple of years. For some growers, this increases the net cost of ginning and storage. Also, the strong basis enjoyed just a few years ago has since weakened. A two-cent more negative or less positive basis on 1,000-lb or two bales per acre cotton amounts to a $20 per acre decline in income.

Cotton’s Safety Net. For the 2018 crop year, generic base on a farm had to be converted to seed cotton base or bases of seed cotton and other covered commodities. The PLC Payment Yield for seed cotton could also be updated based on 2008-2012 yields. Producers had to choose between PLC or ARC for 2018 seed cotton. The seed cotton program is continued in the new farm bill, so cotton has an improved safety net now and going forward.

For all covered commodities on a crop-by-crop farm-by-farm basis, producers will make another ARC/PLC election this year for 2019 and 2020 crops, then make an election annually for each year 2021-2023. Effective beginning for the 2020 crop year, the PLC Payment Yield can be updated on a crop-by-crop, farm-by-farm basis based on 2013-2017 yields.

Being able to update the payment yield for 2018 and 2019 seed cotton PLC and then being able to do so again for all covered commodities for 2020 and beyond is huge. Updating payment yields – because it requires historical data and because producers on a farm may have changed over that period – can be a challenge easier said than done. But, based on conversation with FSA here in Georgia, it has gone well in most cases.

In states with significant peanut acres and base and because peanut farms also tend to be cotton farms, the decision on generic base conversion was not an easy one. In my opinion, the best safety net over the long haul is to have bases close to what is actually planted – how good is any safety net (payments program) if you normally plant 1,000 acres of a crop and only have 600 acres of base of that crop? But the allure of peanut PLC payments based on a $535 Reference Price and with the separate payment limit for peanuts, adding peanut base perhaps at the expense of cotton base with Option 2 may have been hard to turn down.

The seed cotton (SC) PLC for the 2018 crop is currently projected at 2.0 cents per lb. Based on the latest data available, the SC MYA Price is currently projected to be 34.7 cents. The SC Reference Price is 36.7 cents (36.7 – 34.7 = 2.0 PLC Payment Rate).

This is subject to change, as the 2018 crop marketing year does not end until July 31. The PLC rate is received on 85% of the farm’s seed cotton base times the farm’s seed cotton PLC Payment Yield.

Price Outlook Factors and Summary. On February 8, USDA released its first crop production and supply/demand estimates since the partial government shutdown. Following are some of the major February revisions from the earlier December estimates:

- The 2018 US crop was lowered 200,000 bales

- 2018 crop year U.S. exports remain projected at 15 million bales

- World use/demand was lowered 2 million bales. The reductions came in India, China, Turkey and Vietnam.

- The 2018 Chinese crop was raised 500,000 bales and projected imports raised 500,000 bales.

Weekly export reports released since the re-opening of government offices show a good level of export sales.

Old crop futures prices have threatened to fall into the upper 60s. New crop futures (December 2019) are hanging around 73 cents. Prices have been and continue to be hammered by the possibility of a larger 2019 U.S crop, combined with weakening and uncertain demand, plus uncertain exports due to the lingering tariff situation with China.

Prices will eventually swing on U.S. crop condition, harvest acres and yield. Given the environment we’re in, the U.S. exporting 15 million bales for the 2018 crop year would be quite a feat. The uncertainty of exports to China can be offset by increased exports to markets like Turkey, Vietnam and Bangladesh.

Marketing the 2019 crop should especially consider tools and strategies that limit downside price risk, while keeping the opportunity for higher prices open.

Πηγή: Cotton Grower