Cotton Market Update for the Week Ending Friday May 4, 2018

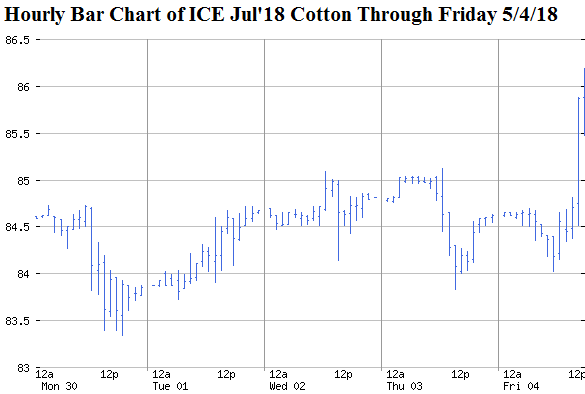

The week ending May 4 saw nearby ICE cotton futures gyrate mostly in a sideways pattern, although new crop followed a gradual uptrend to new highs. Fundamental news this week included decent export sales, albeit with some cancellations, and continued strong export shipments.

Jul’18 cotton on the ICE settled higher on Friday April 13 at 86.90 cents per pound. Old crop prices remain inverted above Dec’18 which settled at 80.57 cents per pound on Friday. Chinese futures and the A-index of world prices were mixed/higher this holiday-shortened week (Chinese Labor Day).

A sample of option prices on ICE cotton futures saw some changes from the previous week because of changes in the underlying futures. On Thursday, May 3, a out-of-the-money 75 put option on Dec’18 cotton cost 2.23 cents per pound while a deeply out-of-the-money 65 put on Dec’18 cost 0.29 cents a pound. These values highlight the continuing opportunity to hedge minimum cash prices in the upper 60s, i.e., above projected costs of production.

This market remains supported by long speculative positioning and continued evidence of good demand, e.g., the strong pace of U.S. export commitments and remaining potential mill fixations. But there is also a risk to see futures weaken if the remaining hedge fund longs get spooked by some risk-off event. The April 4 Chinese tariff proposal is an example of such an event. Even after accounting for some likely upward revisions to 2017/18 U.S. exports, the longer term fundamental picture painted by USDA still implies some price weakness by virtue of a moderate year-over-year increase in 2017/18 ending stocks. The same is true of the 2018/19 outlook.

Nobody ultimately knows how high these markets could go, including new crop Dec’18. The only thing you can know for sure is whether a forward contract or a hedge on today’s futures price will be a profitable, or at least survivable, price floor.

Given all these uncertainties, growers should consider taking advantage of present (or future) rallies, and protect themselves from sudden sell-offs. Forward contracting of new crop bales, immediate post-harvest contracting of old crop bales, and/or various options strategies can be used to limit downside risk while retaining upside potential. In hindsight, contracted 2017 bales could have been combined with call options on the deferred futures contracts. New crop put spread strategies to hedge the 2018 crop are a straightforward and relevant approach. Since February I have heard of bale and acre forward cash contracts being offered in West Texas on competitive sounding terms, e.g., 2.5 cents and 3.5 cents off Dec’18, respectively, for international base quality. Taking advantage of the present opportunity for selling or hedging at these levels was a main topic of conversation on the April 11 Ag Marketing Network conference call.