Cotton Market Update for the Week Ending Friday November 30, 2018

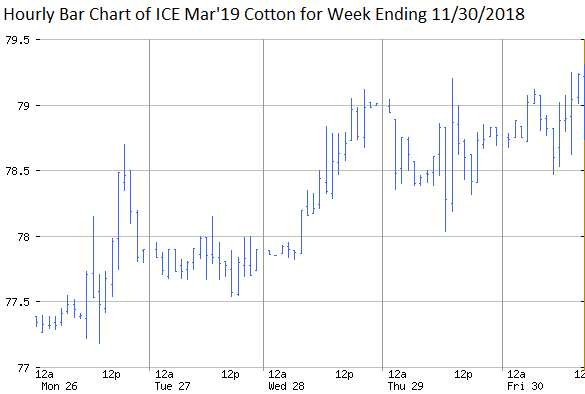

The week ending Friday November 30 saw ICE cotton futures make a gradual 1.5 cent ascent. Fundamental influences included the second straight weekly report of good export sales which reinvigorated the longstanding bullish picture of export commitments. Ongoing bullish supply fundamentals included an ongoing rainy harvest scenario in the eastern Cotton Belt. Lastly there were expressions this week of “cautious optimism” for progress in U.S.-China trade relations which may have influential in supporting cotton futures, in addition to higher stock markets, and a modest lift to corn and soybean futures.

The Mar’19 contract settled on Friday at 78.91 cents per pound, while the Jul’19 and Dec’19 contracts settled the week at 81.00 and 77.03 cents per pound, respectively. The steady-but-modest rise of ICE futures apparently didn’t cross relevant target levels that would trigger buy stops. Chinese and world cotton prices were mixed this week.

A sample of option premiums on ICE cotton futures saw minor changes associated with similarly small changes in the the underlying futures. On Thursday, November 29, an in-the-money 85 cent put option on Mar’19 cotton was worth 7.42 cents per pound, up from 6.17 cents per pound a month earlier when the underlying futures were a little higher. On November 29 an out-of-the-money 75 put on Mar’19 cost 1.34 cents per pound. Looking way out there, a near-the-money 75 put on Dec’19 cotton settled November 29 at 3.84 cents per pound, up from 3.23 cents per pound a month earlier. Looking further back, the gain in these put options since August shows how put options provide a mechanism for down-side price insurance. An out-of-the-money 85 call on Jul’19 cotton was worth 3.10 cents per pound on November 29, down from 3.58 cents a month earlier.

This week provides another example of the ever present risk of unexpected market volatility. It can happen in both directions. For example, a surprise resolution to U.S.-China trade relations, or another surprisingly large cut in U.S. production, or something else totally unexpected could trigger speculative buying. As always, the most relevant question is whether a cash contract or a hedge on today’s futures price will be a profitable, or at least survivable, price floor.

Given all these uncertainties, growers should always be poised and ready to take advantage of rallies, and protect themselves from sudden sell-offs. Forward contracting of new crop bales, immediate post-harvest contracting of old crop bales, and/or various options strategies can be used to limit downside risk while retaining upside potential. Hedges with puts or put spreads on Mar’19 futures can be used to provide near term protection of old crop bales through the harvest season. Contracted 2018 bales could be combined with call options on the deferred futures contracts. Call option strategies have become increasingly affordable with the recent decline in the futures market. New crop put strategies to hedge the 2019 crop are a straightforward and relevant approach.

Πηγή: TAMU