Cotton Market Update for the Week Ending Friday June 15, 2018

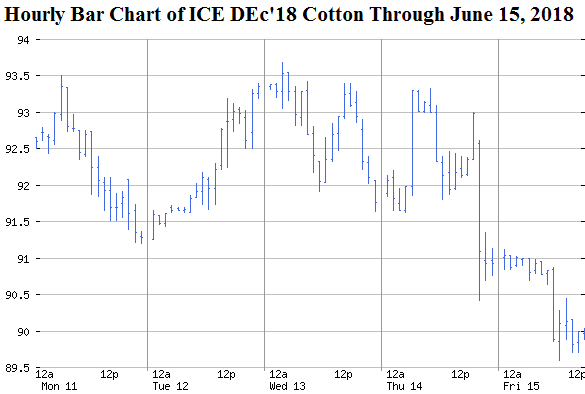

For the week ending June 15, ICE cotton futures gyrated in a sideways pattern until the beginning of Friday’s session. An early two cent drop was followed by more erosion on Friday that saw Dec’18 settle down 311 points at 89.85 cents per pound. Grain and oilseed futures were also lower, as were other commodity futures, U.S. stock markets, and Chinese markets. This general risk-off market behavior may have been triggered by a White House announcement of immanent U.S. tariffs on 1,100 Chinese products.

A sample of option prices on ICE cotton futures saw changes from the previous week because of changes in the underlying futures price. On Thursday, June 14, a 90 cent put option on Dec’18 cotton cost 4.20 cents per pound. Out-of-the-money 85, 83, and 80 puts on Dec’18 cost only 2.14, 1.56, and 0.94 cents per pound, respectively. These values highlight the continuing opportunity to hedge minimum cash prices above projected costs of production (although all these put options were more expensive with Friday’s decline in the underlying futures).

Fundamental influences this week included an announcement by China’s National Reform and Development Commission of an additional 3.67 million statistical bales of available cotton import quota, over and above the 4.1 million bales required by WTO. (Advance knowledge of this inside China is one conspiracy theory to explain of the strength in Chinese cotton markets in recent weeks.) In other international news, the progress of the Indian monsoon slowed down, leaving important cotton growing states like Gujurat behind schedule for the onset of necessary rains. Closer to home, the U.S. Cotton Belt saw scattered rainfall which included some parts of the Texas Panhandle. The forecast for the upcoming week includes more moderate temperatures and decent rain chances in the Southern Plains, as well as tropical moisture in the coastal areas of Texas.

This market remains supported by continued long speculative positioning and other demand indicators, e.g., high U.S. export commitments and remaining potential mill fixations on Jul’18 futures. There is some risk if these hedge fund longs get spooked by some unforeseen risk-off event. The April 4 Chinese tariff proposal is an example of such an event, although its effect was brief. Nobody ultimately knows how high these markets could go, especially new crop Dec’18. The only thing you can know for sure is whether a forward contract or a hedge on today’s futures price will be a profitable, or at least survivable, price floor.

Given all these uncertainties, growers should consider taking advantage of present (or future) rallies, and protect themselves from sudden sell-offs. Forward contracting of new crop bales, immediate post-harvest contracting of old crop bales, and/or various options strategies can be used to limit downside risk while retaining upside potential. In hindsight, contracted 2017 bales could have been combined with call options on the deferred futures contracts. New crop put spread strategies to hedge the 2018 crop are a straightforward and relevant approach. Competitive bale and acre forward cash contract opportunities in West Texas were available earlier in the Spring, but the ongoing drought conditions and price volatility have put a damper on that. So grower hedging may be the main tactic to take advantage of the present opportunity.

Πηγή: The Cotton Marketing Planner