Naomi Blohm, senior market adviser, Total Farm Marketing by Stewart Peterson

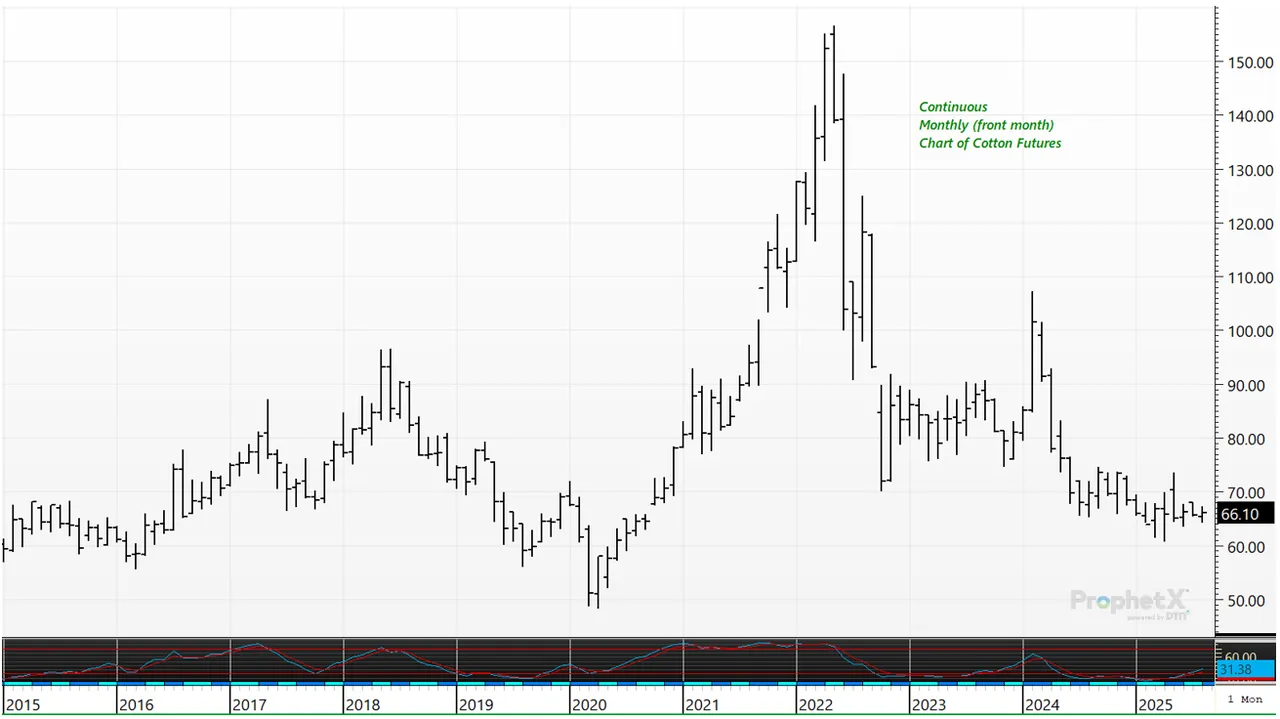

Cotton futures, like many commodities, enjoyed a triumphant price rally in 2021 and into 2022. However, cotton futures prices are now back down to modest price levels not seen since 2020. The fundamental story for cotton has been rather monotonous recently, and thus, cotton futures have traded in a lackluster trading pattern.

What’s happened

Back in late May of 2022 front month cotton futures prices topped out at a whopping 156.64 cents per pound with prices falling over the past three years to near 67 cents per pound, as of this writing.

With a lack of dynamic news in the cotton market, cotton futures prices have been in a sideways trading range for nearly three months.

However, the August USDA WASDE report provided a bit of unexpected friendly news that perked the market higher thanks to a surprise reduction in U.S. cotton production.

From a marketing perspective

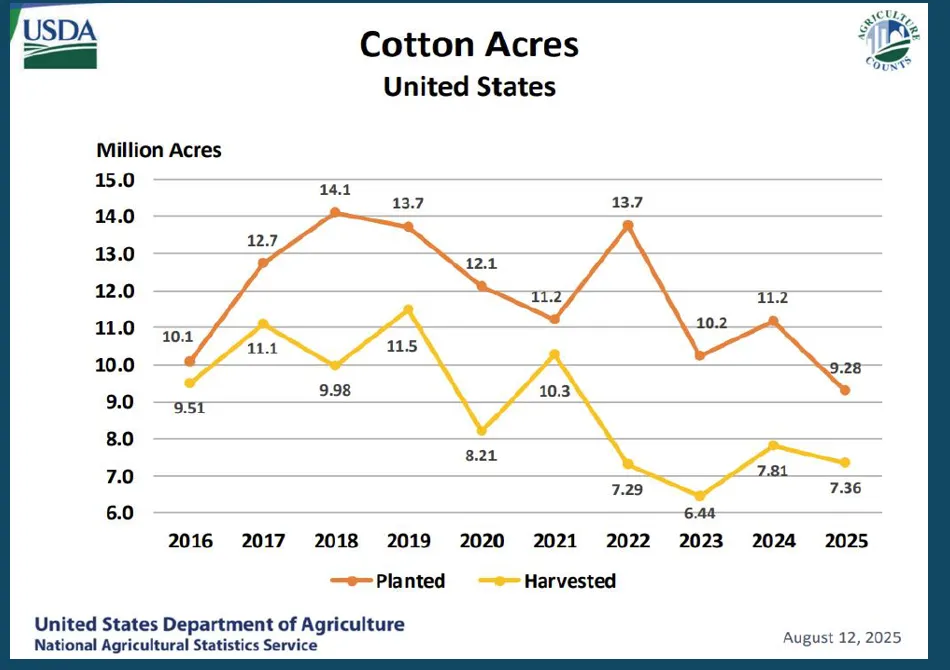

In the August report, the USDA pegged cotton production lower, due to a sharp revision lower in planted area.

The USDA lowered United States planted cotton acres to 9.28 million acres, which was down from the July report, at 10.12 million acres. The abandonment rate for acres increased to 20.7%, up from 14.4%, due to dryness in the Southwest. That puts harvested area at 7.36 million acres.

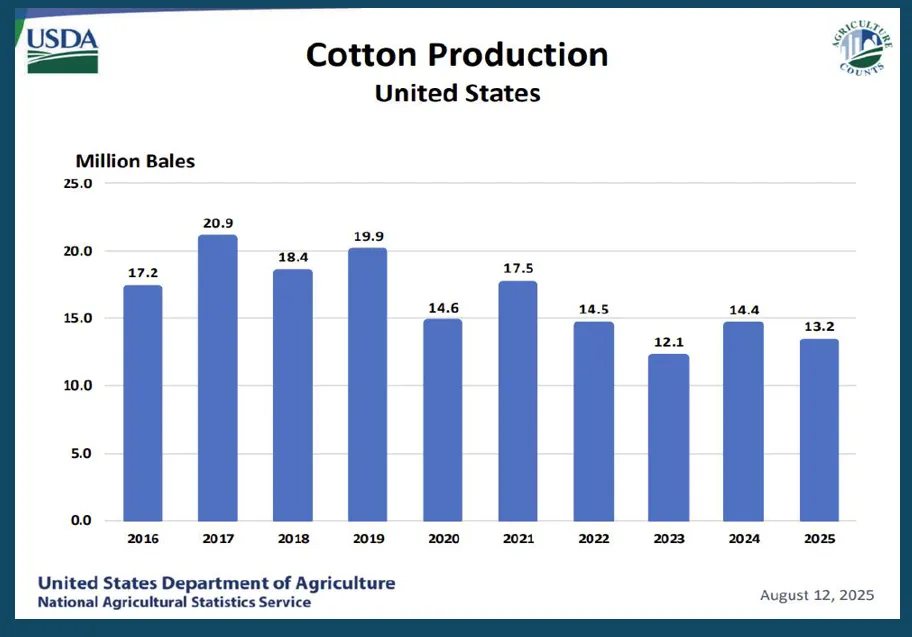

While USDA lowered planted acres, it increased yield to 862 pounds per acre, up from 809 pounds in July.

The combination of lower acres and higher yield put U.S. 2025-26 cotton production at 13.21 million bales, down from 14.60 million in the July update.

Though the supply situation turned friendly for cotton, the demand situation remains murky. And low demand is what’s keeping price action in check.

Looking closer at demand, USDA lowered cotton exports for the 2025-26 season to 12 million bales, down from 12.50 million previously as the United States continues to lose export demand to China.

The ending result when looking at both supply and demand, is that U.S. ending stocks for cotton came in at 3.60 million bales versus 4.60 million in July. This is also below the ending stock number of 4 million from the 2024-25 crop year. This news is likely supportive to cotton prices, but not enough of a reason at the moment, to justify a significant further price rally.

Prepare yourself

Lower production in the August WASDE gave the market a short-term price lift, but global supplies are viewed as ample, which may keep rallies in check.

Global 2025-26 production is marked at 116.622 million bales.

China is the world’s largest grower of cotton. The August WASDE report increased China’s production by 0.5 million bales to 31.5 million bales.

India is the second largest for cotton production, coming in at 23.5 million bales.

Brazil is ranked third, with production pegged at 18.25.

The United States comes in at fourth place, with 13.21 million bales of production.

Global ending stocks for the 2025-26 crop year are pegged at 73.91, down from 75.05 in the 2024-25 crop year, and similar to ending stocks from the 2023-24 crop year when global ending stocks were pegged at 73.36.

Global production is viewed as good enough for now, while global consumption remains in limbo with a global economic marketplace that remains in question. Without a global shake up in production, or a sudden increase in demand, cotton prices might remain in a monotone price pattern into late 2025.

Πηγή: farmprogress.com