Kent Lanclos, Leslie Meyer, Taylor Dew, Stephanie Galbraith, Tony Halstead, and Omri Bein U.S. Department of Agriculture

Introduction

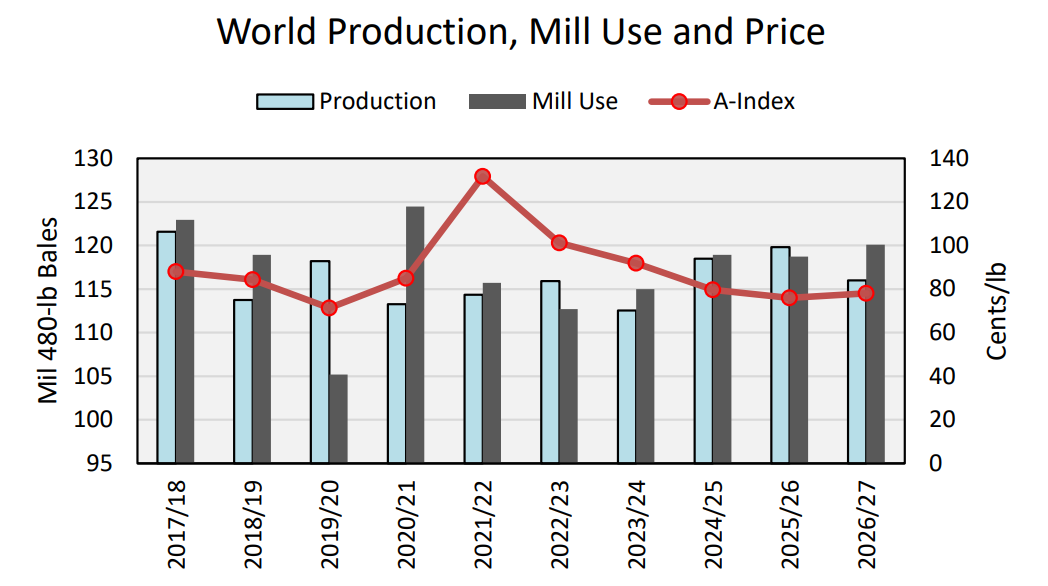

The USDA forecasts global cotton production to decline by 3 percent to 116.0 million bales due to reduced area and yield in some major producers in its first forecast for the 2026/27 marketing year (August-July). Meanwhile, cotton consumption is expected to rise by 1 percent to 120.1 million bales, driven by a stable trading environment and higher economic growth. This would mark only the third time since 2007/08 that consumption exceeds 120 million bales. Despite robust growth in total textile fiber consumption from 337 million bale-equivalents in 2007 to 520 million in 2024, the increase has been dominated by man-made fibers, reducing cotton's share from over 35 percent to around 22 percent over the past two decades. Ending stocks are projected at 71.2 million bales, down 5 percent from 2025/26. Cotton prices will remain under pressure with the A-Index averaging 78 cents per pound, just 2 cents higher than 2025/26.

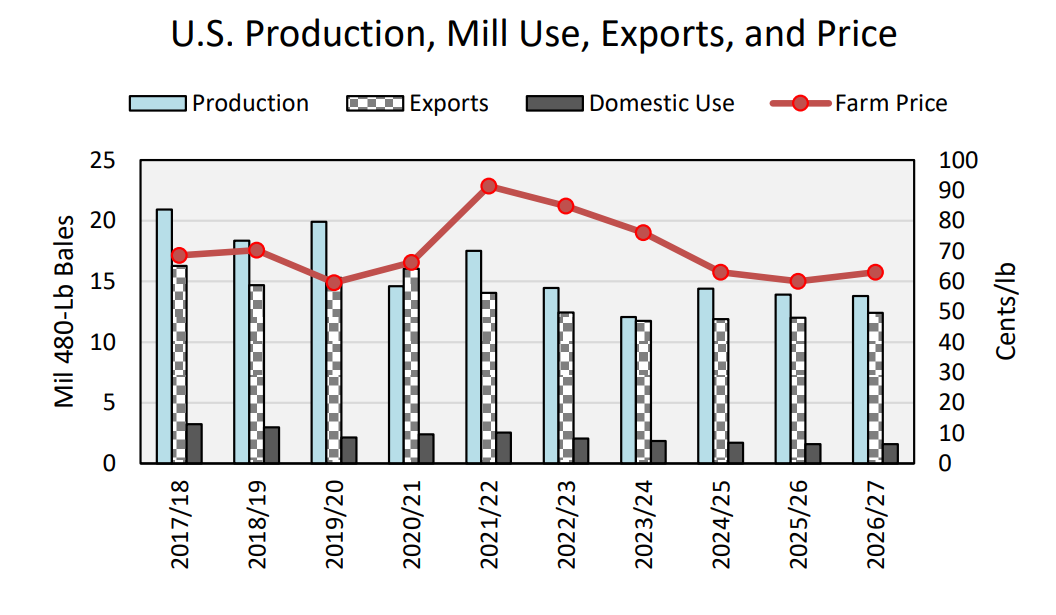

In 2026/27, U.S. all-cotton planted area is expected to increase slightly to 9.4 million acres, up just over 100,000 acres from 2025/26 as Texas cotton area rebounds from its lowest level since 2015/16. With an average abandonment rate of 19 percent and a yield of 856 pounds per acre, production is projected at 13.6 million bales, 2 percent below 2025/26. Domestic mill use remains at 1.6 million bales, while exports are forecast at 12.2 million bales, 200,000 higher than 2025/26 due to larger Chinese imports. Ending stocks will decrease by 200,000 bales to 4.2 million, with a stocks-to-use ratio of 30 percent, down 6 percent from 2025/26. The seasonaverage farm price for upland cotton is predicted to be 63 cents/lb., up 3 cents from 2025/26, supported by the slight increase in global cotton consumption and lower U.S. and world stocks.