After the Chinese Lunar New Year holiday (early Feb), cotton yarn mills have suffered gradual weakness of the market. At the first, ICE cotton futures market has surged during the Chinese Lunar New Year holiday, and ZCE cotton futures market followed up, so spinners showed strong willingness to raise the prices, but after a few weeks, sales were unfavorable and spinners anticipated peak season in Mar and Apr. Nevertheless, the sporadic epidemic appears in Mar, especially after mid-Mar, the epidemic-related control management measures tend to be stricter, and transportation is not smooth, making downstream consumption worse. With high cotton price, spot cotton sales have been lackluster.

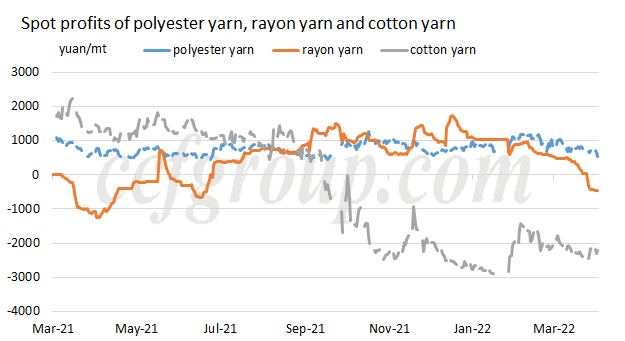

Currently, cotton yarn mills face low profits, low cotton inventory, but high cotton yarn inventory. From mid-Oct, 2021, cotton yarn mills began to suffer losses, one reaching 3,000yuan/mt. Recently, the losses basically maintain at around 2,000yuan/mt. Currently, cotton yarn sees the largest losses, and polyester yarn profits are basically flat, that is why some spinners turn the production shift. Rayon yarn profits begin to reduce recently. Yarn mills face large pressure.

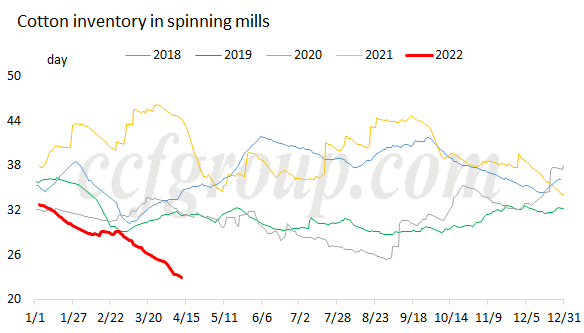

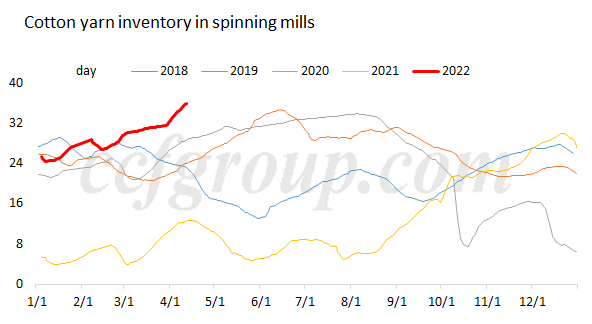

Since Mar, cotton inventory in cotton yarn mills continues to reduce, and currently, it has been around 23 days. Besides, cotton yarn inventory keeps piling up, to around 36 days.

Chinese cotton prices remain high, and cotton yarn mills have weak willingness to replenish cotton. For the low cotton inventory, one reason is that downstream consumption sees no improvement and traditional peak season is not anticipated. Another important reason is the high cotton prices. On one hand, ZCE cotton futures market is relatively firm stimulated by higher international cotton prices. On the other hand, the cotton costs are relatively high. Though there is still large quantity of Xinjiang cotton to be sold, most ginners maintain the prices (only a few ginners are eager to sell and cut prices). This season, the purchasing costs for ginners are generally at around 24,000yuan/mt. Currently, only a few ginners have sold out the cotton, while most ginners with cotton at hand maintain high offers. Some ginners with cotton at costs of 26,000yuan/mt state that the cotton has basically not sold till now, and they have not offered prices based on current low level.

Spot cotton prices continue to weaken, while sales keep lackluster. Since end Mar, sales are even more difficult amid the epidemic. Traders start to adjust lower the basis successively. But sales are tolerable for cotton at lower prices. Market prices are mixed and differ much. Besides, due to high purchasing costs, many traders are hard to accept the losses by adjusting lower prices.

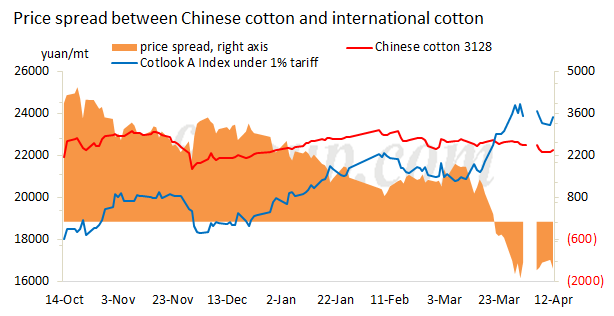

In addition, despite of the lower Chinese cotton prices than foreign cotton prices, the stimulus for Xinjiang cotton sales is limited. From Mar 22, Chinese cotton prices start to be lower than foreign cotton price, and currently, the CCFGroup Chinese cotton 3128 price is 1,500yuan/mt lower than RMB price of Cotlook A under 1% tariff. Under this price spread, Xinjiang cotton sales have not seen big improvement. According to the spinners using imported cotton, after the sharp rise of imported cotton, they indeed reduce imported cotton volumes, and purchase more Xinjiang cotton, but the increasing volumes are also not large due to weak downstream market. Some spinners turn to produce more polyester/cotton yarn. With weak downstream consumption, the lower Chinese cotton prices have limited stimulus for Xinjiang cotton sales.

Currently, cotton textile industrial chain is at a deadlock. Most ginners are not willing to cut prices, and spinners resist to pay higher cotton price and have low buying interests. Cotton yarn inventory is accumulating, and spinners face losses. Without the effective control on the epidemic, downstream consumption is supposed to be hard to see improvement. In short, spinners may keep purchasing cotton on need-to-basis.

Source: ccfgroup.com