Recently, polyester market shows weakness, with PSF prices falling somewhat. VSF prices are relatively stable, but its price spread with cotton continues to expand. Except spandex, cotton is extraordinary outstanding. Therefore, market players frequently ask why the price of cotton is so strong. This article analyzes the reasons and the current status quo of cotton industry.

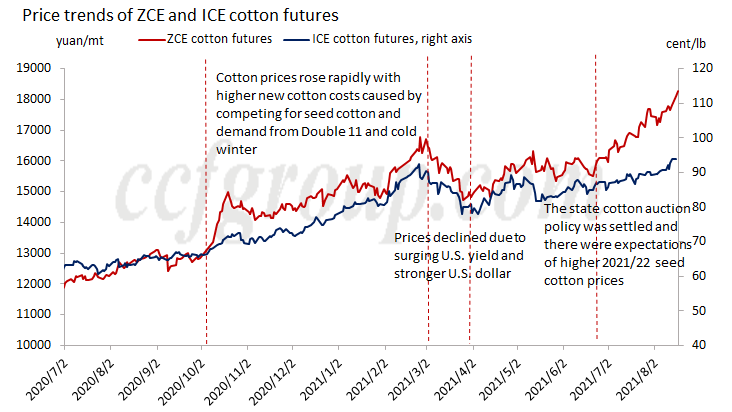

After the China state cotton auction policy was settled in end Jun, Chinese cotton prices have been constantly rising strongly in Jul and Aug, mostly attributed to the expectations on high new seed cotton prices in beginning period of 2021/22 season caused by the fierce competition for seed cotton like last year. In 2020/21 season, seed cotton started to procure from mid-to-late Sep in Xinjiang, and large quantity of cotton arrived on the market during National Day holiday (Oct 1-8, 2020). Due to increasing ginning capacities in Xinjiang (more than 100 new lines last year), ginning factories competed for purchasing seed cotton, and seed cotton prices rose rapidly during the National Day holiday. New cotton costs were higher about 2,000yuan/mt than ZCE cotton futures at that time. In the meantime, end-users replenished stocks in advance with worries over rising costs, and actual demand also came from Double 11 and expectations of cold winter, leading to the upswing of cotton prices from Oct 2020 to Feb 2021. After the Chinese Lunar New Year holiday, cotton prices slumped in Mar, 2021, as end-users were hesitant to conclude orders and macro risks were seen from surging U.S. yield and higher U.S. dollars. In Apr-Jun, cotton prices were relatively stable amid the inflation and government control on macro commodity prices. After the China state cotton auction was settled in end Jun, market players expected that 2021/22 Chinese cotton production might decrease in 2021/22 season, and planting costs of new cotton climbed up, while ginning capacities remained high, so market players anticipated a similar market situation like last year and reacted first on cotton futures market.

In the other major cotton producing countries outside China, Brazilian and Pakistani cotton production is supposed to reduce much, and there are also uncertainties on the production of U.S. and Indian cotton. Moreover, downstream market is not poor during Mar and Aug. Industrial stocks of cotton yarn have not piled up. Downstream buyers replenish more cotton or replenish cotton in advance with the expectations of tight supply, which causes higher cotton prices. In summary, in the cotton industrial chain, cotton prices are more reflected the expectations of tightening supply, while PSF and VSF markets have no such obvious supply and demand contradiction like cotton market, so they have no outstanding situation.

| Current status of cotton industrial chain | ||

| Factors | Status | Nature |

| Chinese cotton price | Prices have been high | slightly bearish |

| Expectations of cotton prices in early 2021/22 | Above 7.5yuan/kg of seed cotton prices have been reflected on ZCE Jan'22 contract. On Aug 17, the closing price was equivalent to about 7.8-7.9yuan/kg of seed cotton price. | neutral |

| Chinese-foreign cotton price spread | Large price spread, but driving forces of ICE cotton become stronger | neutral |

| Cotton-cotton yarn price spread (spinning profit of Chinese cotton yarn) | Spot profits narrow, while actual profits remain high | From bullish to bearish gradually |

| Cotton-PSF/cotton-VSF price spread | The substitution between cotton and VSF is easier. Currently, price spread between cotton and PSF/VSF expands, but end-user demand is stronger on cotton this year. | neutral |

| Chinese cotton demand | Cotton inventory in spinning mills is neutral. Spinners still show strong purchasing willingness on concern about rising costs | bullish |

| Chinese cotton yarn demand | Moderate, slightly going thinner. More speculative demand | neutral to bearish |

| Industrial inventory of Chinese cotton yarn | Industrial inventory remains low, and better than that of polyester yarn and rayon yarn. Part of large spinning mills has orders filled till end Sep and early Oct | bullish |

| Commercial inventory of Chinese cotton yarn | Large commercial inventory, and warehouses are full in Guangdong and Nantong | slightly bearish |

| Grey fabric market orders | No obvious signal of peak season coming. There are worries over the overseas demand pulled forward, but domestic demand may still exist, but the peak season is hard to confirm | neutral to bearish |

| Grey fabric inventory | Good status of inventory, better than polyester industrial chain | neutral |

| International cotton supply | Uncertainty on Indian cotton production, and USDA may forecast lower Pakistani cotton production further. In addition, USDA may continue to lower global cotton stock-to-use ratio. Harvests of Brazilian cotton is slow, and 2020/21 Brazilian cotton production reduces much | bullish |

| International cotton demand | China has started to purchase large quantity of U.S. cotton, and there is also purchasing demand from other countries | bullish |

| Downstream status on international market | Cotton yarn prices are also high due to high cotton prices in India and Pakistan, and the epidemic situation is severe in Vietnam | bullish |

We have analyzed the major factors influencing cotton prices and the current status in cotton industrial chain. Though there is no obvious signal of peak season coming and there are worries about the overseas demand pulled forward, downstream spinning mills have to use cotton with high costs, and cotton yarn traders may not sell stocks quickly (the stocks that are replenished previously have high profits). Cotton yarn has many new capacities, and with high operating rate, the demand for cotton is supposed to remain large. Chinese cotton prices may fall down somewhat, but in long run, the upward trend is not supposed to change.

Source: ccfgroup.com