On Jun 1, ZCE major cotton contract, Sep contract, surged over 900yuan/mt, and the spread between Sep and Jan contracts narrowed quickly unexpectedly. The rise of Sep contract was obviously higher than that of Jan contract. Rumors were in circulation on the market soon. There were mainly two rumors: 1. The commercial cotton stocks issued by one institution were not in line with the actual stocks, and some enterprises considered that the actual commercial cotton stocks were relatively tight; 2. One large spinning mill purchased large quantity of cotton. Some markets had good orders and there were rumors that some markets could have orders fulfilled till end Oct.

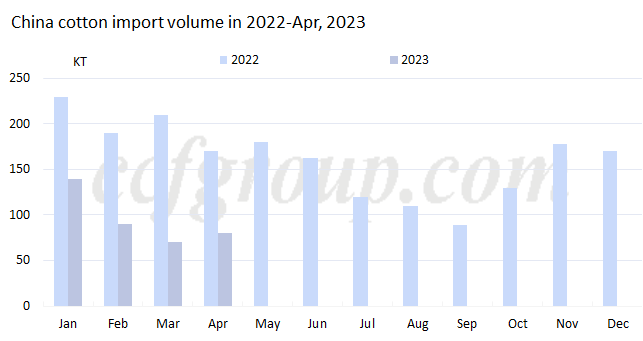

Looking from the first rumor, there are different views on stock data. Every enterprise and institution has own investigation, and the differences on the stock data between the relative institution and actual market may have own different way to calculate the data. According to our views from the market situation, the stock may be not that tight like the rumors saying less than 2 million tons. Some enterprises hold the stock till now and sales are scarce. Nevertheless, supply of spot cotton at lower prices gradually reduce with the sales from Oct 2022 to May 2023, especially when ZCE cotton futures slumped on May 25-26, sales have improved obviously, and mainstream basis climbs up quickly. Some sellers that offer high prices also start to sell. Later, with the gradual reduction of cotton inventory, basis is expected to go firmer gradually. Moreover, monthly cotton imports have been constantly below 100kt this year, and till Aug and Sep, 2022/23 cotton inventory may tighten gradually. However, no obvious supply gap is seen currently.

For the second rumor, we have confirmed with the relative spinning mill, it has not purchased large quantity of cotton this week, and the major purchases are during last week, when ZCE cotton futures slump during May 25 and May 26. For downstream demand, downstream market is in slack sentiment, and sales are thinner in May compared with Apr. Nevertheless, the situation differs in different markets, and Guangdong market is the weakest this year, while Nantong market which is hot previously also cools down somewhat. But operating rate of spinning mills has not reduced and cotton consumption has been constantly high indeed this year.

The sharp rise of ZCE cotton on Jun 1 more lies in the bullish expectation in medium to long run. Though 2022/23 Chinese cotton production is high, cotton imports reduce largely year on year, and from demand side, monthly cotton consumption has been constantly above 700kt or even 750kt from Mar, 2023. With the digestion of available cotton stocks, the supply of 2022/23 cotton in the end period of 2022/23 season is supposed to gradually tighten. In terms of the market in 2023/24 season, the weather condition in Xinjiang remains unfavorable from late Apr to late May, and there are still expectations over large reduction of 2023/24 Xinjiang cotton production and harvest-rush of seed cotton in the second half year. On May 21, when Xinjiang suffered bad weather again, ZCE cotton tried to climb up again on May 22-23, but heavy worries have covered on the macro environment and most commodity prices stepped downward on May 22-23, so ZCE cotton failed to increase. During May 24 and May 31, ZCE cotton futures declined following the trend of commodity market. The open interests of ZCE Sep contract dropped by about 100,000 lots during May 24 and May 26. On May 31, after the release of China manufacturing PMI, the bearish sentiment retreats periodically, and bulls enter the market again, and by virtue of the rumors, ZCE cotton futures surge significantly on Jun 1. The bullish expectations for cotton market in medium to long run never change.

Source: ccfgroup.com