The USDA February 2023 Cotton Outlook projects world cotton consumption bottoming at 110.7 million bales for the current 2022/23 marketing year. They then forecast 2023/24 consumption recovering to 115.5 million bales due to: 1) post-COVID reopening in China with increasing GDP, 2) lower Chinese production and greater need for Chinese imports, and 3) an “unusual inventory dynamic” of pent-up cotton demand following previously COVID-disrupted deliveries of cotton textile goods. Other bullish influences for cotton consumption include the competitively low prices of raw cotton, which appear to have translated to higher levels of U.S. cotton exports since January.

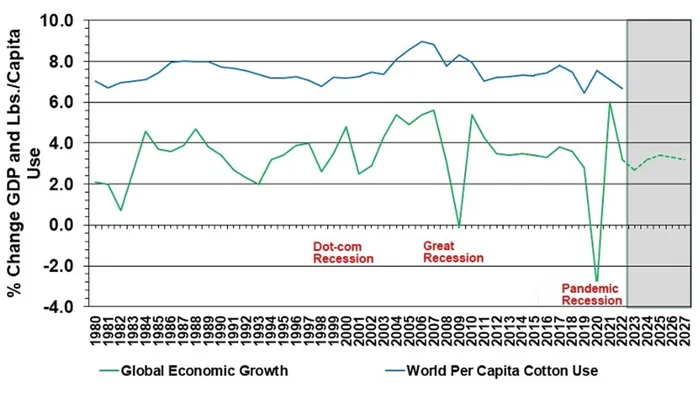

Beyond China, world GDP is also currently forecasted by the International Monetary Fund to rise slightly to 2.9% (Figure 1, dashed green line). This is important to the cotton market because cotton consumption tends to rise with economic growth and fall with economic declines. For example, the blue line in Figure 1 shows world cotton consumption ranging between about six and eight pounds per person per year. The peaks and valleys of per capita cotton consumption coincide with the respective trends of world GDP. This is not surprising since cotton-made apparel and home furnishing products are both semi-durable and somewhat discretionary.

Growing expectations of stronger economies, increasing mill use, and stronger export demand are, in turn, bullish influences on ICE cotton futures. In the near term, they could contribute to stronger old-crop prices, especially if the current hedge fund net short position is liquidated in a short covering rally.

There are, of course, counter influences. First, a bullish demand response would be somewhat self-correcting as mills generally buy less cotton at higher prices. It remains to be seen how long and how high the “unusual inventory dynamic” will push cotton prices. In addition, there is a potential macro-economic risk shrinking the demand curve and putting downward pressure on prices. The latter could result from strong recessionary influences due to high interest rates as central banks continue their attempt to lower inflation to target levels.

Source: Southern Ag Today