If the September WASDE report was a dove hunt, it would have been a tiring, hot and sweaty trip where the only thing you reached your limit on was the beer in the cooler.

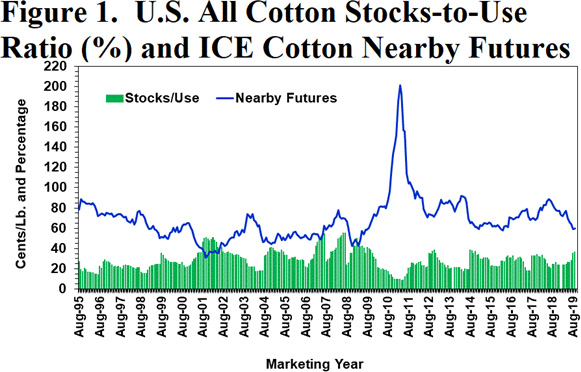

USDA’s September adjustments to the 2019/20 U.S. all cotton numbers saw a month-over-month decrease in carry-in (-400,000 bales), production (-654,000 bales), exports (-700,000 bales), domestic mill use (-100,000 bales), and un-accounted (-250,000 bales). Many analysts expected a trimming of the U.S. production forecast, and it was not surprising to see it mostly from Texas and Oklahoma where dryland productivity downshifted in the second half of the summer. All these changes netted out to zero change in the bottom line of the old crop balance sheet, leaving 7.2 million bales of ending stocks. This burdensome stocks level, as well as the large year-over-year increase that it represents, remains a fundamentally bearish indicator (see Figure 1).

The 2019/20 world cotton supply and demand adjustments were not very encouraging either. The September report continued a recent trend of downward revisions to forecasted world consumption, particularly in India and China. Further, Indian supply also increased from upward adjustments to beginning stocks, production, and imports. World trade categories saw various adjustments in various places that resulted in net reductions in aggregate imports and exports. The bottom line of all this was a 1.3 million bale month-over-month increase in world ending stocks, which would have modestly bearish implications for 2019/20 world prices, according to history and economic theory.

So, what do we make of this fundamental picture? The reductions in mill use and trade is not encouraging. It is probably related to slowing economies, lingering trade disruptions, and perhaps surpluses of yarn. Those situations may not improve in the short run. On the production side, I would not be surprised if USDA continued their incremental trimming of U.S. production. But the effect on ending stocks may not be significant since exports are usually trimmed along with lowered production. As a result, this fundamental recipe for low futures prices may persist.

There is always room for surprise. If something happens to scare the rest of the hedge fund shorts out of their bearish bets, nearby futures prices could spring back into the middle sixties. Such a rally might cause a flurry of mill buying to cover their short-term needs. If December 2019 did make it to 65 cents, would you sell your unpriced cotton there? The alternative may be the mills sitting back on their hands, and the merchants waiting for the CCC loan to provide them with futures supplies.

Source: farmprogress.com