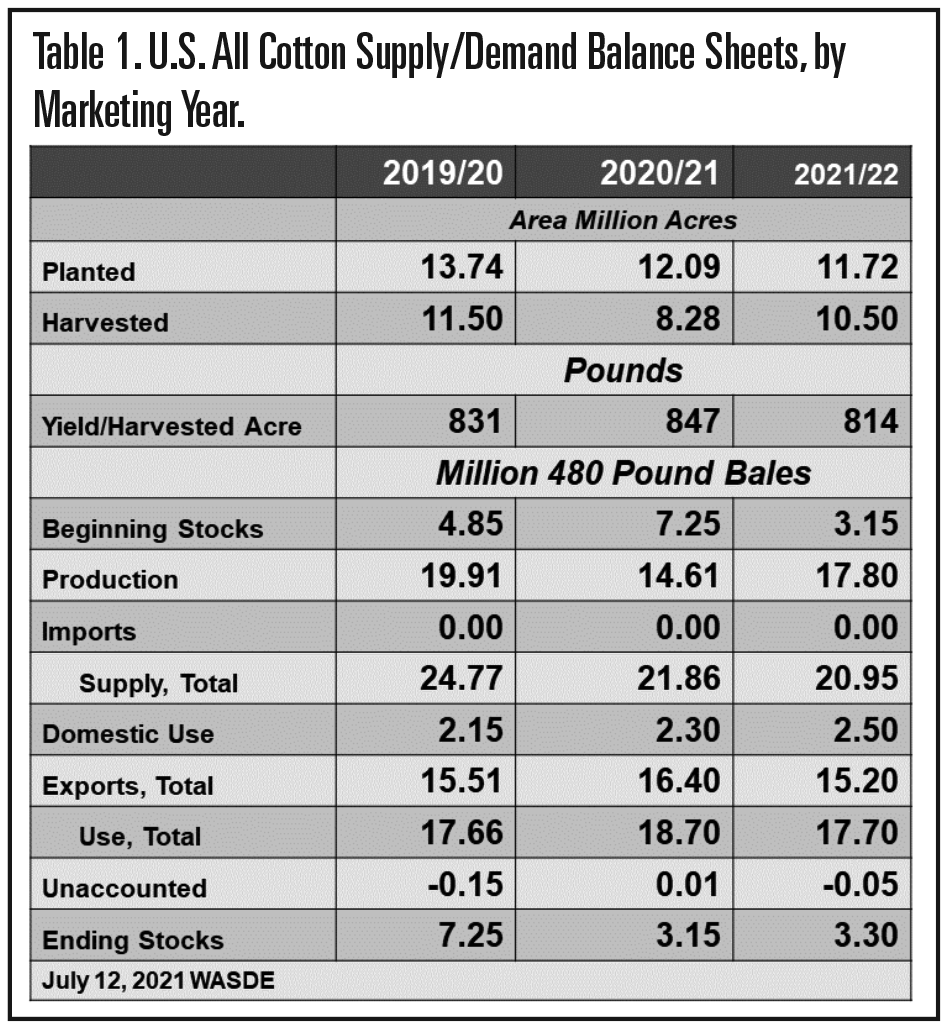

The last notable adjustment was that USDA lowered expected average U.S. cotton yield by 33 pounds per acre. That is a big downshift month-over-month. It assumes that the lower abandonment means a lot of low-yielding Texas dryland will get harvested, pulling down the U.S. yield average. The flip side of that assumption is if West Texas gets a mix of heat units and timely moisture going forward, plus that idyllic September/October, then yields might be higher than expected.

Table 1. U.S. All Cotton Supply/Demand Balance Sheets, by Marketing Year.

I submit that there is room for price volatility in both directions as the current balance sheet gets updated. The three-something million bale ending stocks outcome that is currently projected should support futures in the current 80 cent range. Going forward, any surprises in the form of lower production from inadequate heat units, flooding, tropical storm damage, inadequate maturation, an early freeze or messy harvest season could push prices into the 90s. On the other hand, a few million extra bales from a good growth, maturation, and harvest conditions could pressure prices a bit in the early fall.

For additional thoughts on these and other cotton marketing topics, please visit my weekly on-line newsletter at http://agrilife.org/cottonmarketing/.

Source: farmprogress.com