May in Texas is known for Cinco de Mayo, Mother’s Day, and a mix of beautiful, miserable, and dangerous weather (hence the above quote from Shakespeare). But for cotton market watchers, May means one thing: new cotton supply and demand projections from USDA. The May WASDE report is closely watched because it is USDA’s first detailed and comprehensive guestimate of U.S. and world cotton numbers.

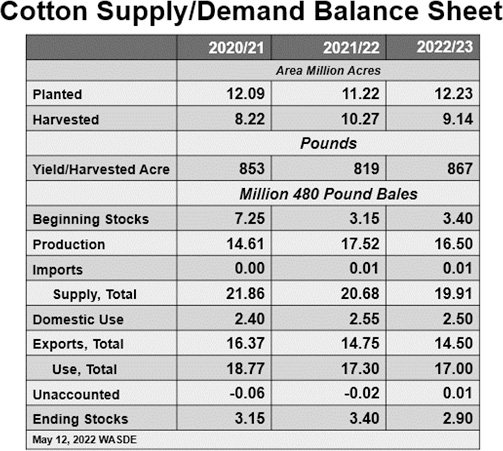

This year’s U.S. cotton numbers are currently grounded with a forecast of 12.2 million acres planted. That is based on USDA’s March 31 Prospective Plantings report. It will, however, be updated with USDA’s Planted Acreage report at the end of June, as well as USDA FSA certified acres data periodically after that. So, beware of this potential souce of change to the outlook.

USDA’s WASDE forecasts in May, June, and July typically involve assumptions of average abandonment and yield from recent history. The May WASDE report was no exception with projections of ten-year average abandonment (25%) and five-year average yield (867 lbs/acre), both weighted by region. In the case of the drought-stricken southwest region, they fudged the abandonment number higher than average. I can’t quibble with these numbers, although there is certainly a chance that the national average abandonment number could be higher. The market won’t really know the abandonment for certain until well into the fall. That uncertainty alone will keep prices supported.

On the demand side, USDA assumes (reasonably, I would say) that U.S. domestic spinning will be 2.5 million bales, while U.S. exports will total 14.5 million bales. The bottom line of all this is that U.S. ending stocks could shrink to under 3 million bales, which is tight in general and tighter than the previous year in particular (see the table). That kind of year-over-year adjustment and tight level is fundamentally price supporting, with upside potential towards $1.40.

Of course, it is early, and there is a lot of risk around this or any other projection. For example, we could have higher- or lower-than-average abandonment. What if we plant 12 million-plus acres and then have timely rains? The production question will likely remain uncertain all summer, which will buoy prices. On the demand side, how much and how long will household discretionary spending be impacted by higher prices for gasoline and groceries, and higher car payments and mortgage payments? At a minimum, such forces could be a headwind for apparel retail sales and ultimately the demand for cotton, in which case, the assumption of 14.5 million bales of U.S. exports could be too optimistic, especially if U.S. prices trend higher into the fall, and ample foreign supplies are available.

For additional thoughts on these and other cotton marketing topics, please visit my weekly on-line newsletter at http://agrilife.org/cottonmarketing/.