USDA’s October WASDE report included some major revisions to Brazil’s cotton balance sheet. This led to a correction of previous overestimates of Brazilian cotton stocks. These accounting revisions are due to the expansion of cotton production in that country. So, it might be useful to take a more historical view of the U.S.’ biggest competitor in cotton production and export.

Brazil is a little like Texas in that it has a range of planting and harvest dates, depending on the region. The variation in growing seasons also depends on whether cotton is grown as the primary crop or a shorter season “second crop” after soybeans.

Brazil has two main cotton-producing regions. The Northeast Region (Figure 1) was the traditional cotton-producing region of the country prior to the 1990s. Over the last 25 years, cotton production has been expanding in the Central-West region (Figure 1), particularly the state of Mato Grosso.

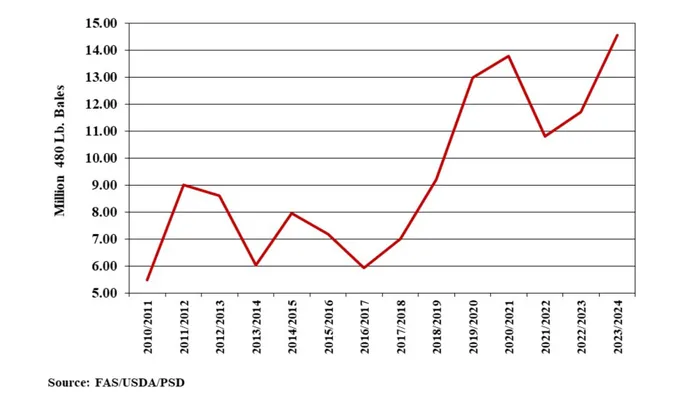

The dominant production system in Mato Grosso involves planting “second crop” cotton following harvested soybeans. The latter results in a shorter growing season with reduced inputs, while still benefitting from rain-fed planting/growing seasons and a dry harvest season (June to September). The combination of these efficiencies and the expanding acreage in Mato Grosso is reflected by a massive increase in Brazilian production over the last 14 years (Figure 2).

As a result, Brazil is now projected to displace the U.S. as the world’s third-largest cotton producer. Even more problematically, Brazil appears poised to surpass the U.S. as the top global exporter of cotton. It will be interesting to watch in 2024 if the countries go head-to-head, assuming the U.S. has a healthy 16-plus-million-bale crop next year. The U.S. may well remain the top exporter, but only if we can sell at competitively lower prices.

For additional thoughts on these and other cotton marketing topics, please visit my weekly on-line newsletter at http://agrilife.org/cottonmarketing/.