Catherine Salfino

A year drawing to a close marks a time of reflection for many. And for two of the industry’s relentlessly hopeful sectors – farming and retail – it’s also a time to take stock and consider the outlook for next year.

In the farming branch, cotton prices have been stable but low, which has made it a tough time for growers. But this stability could benefit apparel makers and retailers that take advantage of the lower pricing.

“This stability in raw material pricing may be one bright point in the sea of uncertainty that has been facing the industry over the past year,” said Cotton Incorporated’s Jon Devine, senior economist, in an interview with the Lifestyle Monitor™.

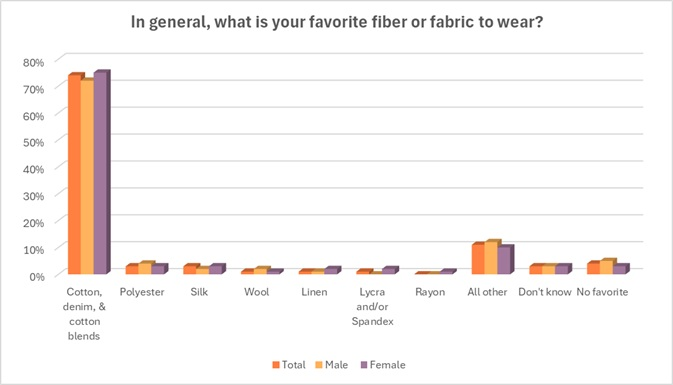

By working with cotton instead of synthetic apparel, brands can both win over consumers and help their bottom lines after facing a host of challenges[1] in 2025. Consider that nearly three-quarters of shoppers (74 percent) say their favorite fiber or fabric to wear is cotton, denim, or a cotton blend, according to Cotton Incorporated’s 2025 Lifestyle Monitor™ Survey. The survey completes 500 interviews per month with U.S. consumers between the ages of 13 and 70. Further, nearly 6 in 10 consumers (59 percent) say they would pay more for natural fibers such a cotton.

Devine explains that crop prices declined after surging during the pandemic and are now as low as they were pre-COVID. This puts growers in a bind though, since the cost of inputs have increased with inflation. The USDA estimates that costs have risen about 30 percent since 2019. The combination of weaker prices and higher costs has implied negative returns for many producers, Devine said.

The pricing issue stems from a number of factors. Firstly, China isn’t importing as much as it used to. The Asian nation is the world’s largest producer and spinner, but it grows less than its mills use, Devine said. Until recently, that made it the world’s largest importer.

“After bringing in fifteen million bales in 2023/24, which was the most in a decade, Chinese imports fell to levels near five million bales in 2024/25,” Devine said, adding that China’s imports are expected to continue at that pace. “At the same time, there has been an increase in supply, primarily the result of more cotton being grown in Brazil, which has more than tripled the size of its crop over the past 15 years.”

The combination of the pullback from China and the increased supply have created price competition in the international market – and pushed prices lower.

Indigo Ag’s Ewan Lamont, head of sustainability solutions at the Boston-based agricultural technology solutions provider, says regenerative agriculture could help improve profitability for growers.

“Today, the real profitability of a crop is dictated not just by the futures price, but by premiums and discounts based on fiber quality, a metric increasingly held hostage by extreme weather,” Lamont said in an interview with the Lifestyle Monitor™. “The 2024 season illustrated this volatility in Arkansas, where two hurricanes struck within three weeks, degrading crop quality and erasing potential margins.”

“Regenerative agriculture practices offer a critical pathway to long-term profitability and crop resilience,” Lamont continued. “Although implementation often requires upfront investment and patience because soil health does not improve overnight, mature systems that utilize practices like cover crops create a vital buffer against droughts and floods. By reducing plant stress over time, these practices maintain fiber quality and build a natural hedge against volatility, turning regenerative cotton into a strategy for both sustainability and long-term risk management.”

In contrast to the ’24 season, Devine said the 2025/26 crop year has benefitted from some improvement in the weather. Drought conditions that were present for several years in West Texas, the largest growing region in the U.S., were less severe this season. This helped reduce the percentage of acres that were not harvested or abandoned.

Outside of West Texas, Devine related that despite intermittent issues with excess rainfall, national yields are expected to be higher, adding that estimates for the U.S. crop have been increasing. It’s a double-edged sword though: Higher yields can increase producer revenue, but the bigger crop also brings additional cotton to the global export market, which can put further weight on prices.

Looking ahead, Devine expects cotton prices to remain relatively stable, if low, as the supply and demand situation is not expected to change dramatically for the foreseeable future.

“Brazil is expected to continue to produce record or near-record harvests,” Devine said. “U.S. acreage has shifted lower in response to lower prices but may not decrease too much from recent levels. Other exporters, like Australia, are also facing profitability challenges but can be expected not to change their production too drastically.”

Devine says the glut in supply could be helped if global mill-use increases. However, he points out, changes in trade policy pose significant questions for downstream markets.

“Higher tariffs remain in place for U.S. imports, with many sourcing locations subject to 20 percentage point increases,” he said. “This now includes China which, in statements from U.S. officials and in U.S. policy changes earlier in the year, appears to be targeted for duties that would be higher than most other countries. There have also been arguments made in front of the Supreme Court regarding the legality of the justification used to implement tariffs. The timing and direction of the court’s decision remain unknown.

“In the meantime,” Devine continued, “uncertainty in tariff policy and the costs posed by higher tariffs have created concern about a pullback in U.S. apparel demand, which could limit the ability of global cotton use to move higher in the near term.”

Devine also pointed out that while the U.S. is the world’s largest market for apparel, it is still just one market. Europe has been struggling with growth since COVID, but has seen economic growth with changes in government spending. Meanwhile, China continues to suffer from sluggish consumer spending as decreases in housing prices weigh on personal finances.

“As a result, the outlook for global macroeconomic growth is somewhat muted,” Devine said. “With ample exportable supply, the outlook for cotton prices could be more of the same.”

Indigo Ag’s Lamont says brands could help increase cotton demand since they’re under pressure to not only address and decarbonize scope 3 emissions, but also to mitigate changes in the environment.

“Many household names in the U.S., including The North Face, are investing in regenerative agriculture across the value chain to improve resiliency and shore up their cotton supply,” Lamont said. “That being said, growers need a consistent message of support from suppliers and designers. Fashion companies should look to support farmers. Cotton grows in rotation with other crops, creating opportunities for shared investment in more resilient supplies, sustainable operations and shared benefits.”