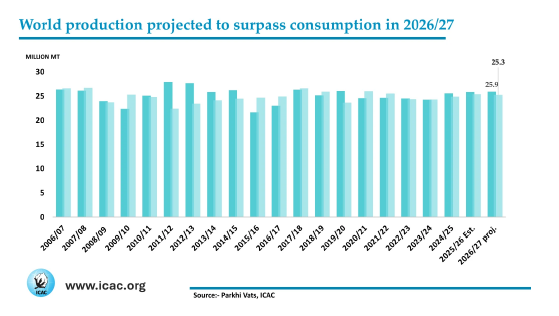

Washington, DC — World cotton production in the 2026/27 season is projected at 25.9 million tonnes, exceeding global consumption of 25.2 million tonnes, according to the May 2026 issue of Cotton This Month. That means both production and consumption are expected to remain close to current season levels, while global cotton trade is projected to decline by 2.7% to approximately 9.6-9.7 million tonnes.

There are some key market drivers having an impact:

- Geopolitical tensions in the Middle East could disrupt fertilizer supply chains, increasing input costs for producers

- Severe drought in the United States is affecting most cotton-growing areas, raising the likelihood of abandonment

- Rising prices for synthetic fibers may improve cotton’s competitiveness

- Favorable conditions in China are expected to support strong yields

Production, Consumption, and Trade

China is expected to remain the world’s largest producer (nearly 7 million tonnes) and the leading consumer (accounting for 32% of global use).

Global exports will continue to be led by Brazil, followed by the United States and Australia. On the import side, Bangladesh is projected to remain the world’s largest importer at 1.8 million tonnes, followed by China, Vietnam, Pakistan, and Türkiye.

World cotton ending stocks for 2026/27 are projected to rise by 4% to 17.9 million tonnes, reflecting higher production and increased imports, particularly in China.

ICAC’s Price Projections

The Secretariat’s current Cotlook A price forecast for the 2025/26 season, based on current supply and demand estimates, ranges from 73 to 84 cents per pound, with a midpoint of 78 cents per pound. ICAC’s price projections are made by Ms Lorena Ruiz, ICAC Economist.

Source: ICAC