The ICAC’s Impacts Brief on the Cotton Market During the COVID-19 Lockdown

The global cotton sector plays a vital role in the global economy as an agricultural commodity with over 100 million families engaged in production and as industrial commodity used to produce apparel and textiles. The global cotton market is aff ected by fundamental factors of supply and demand and has been impacted by the Great Lockdown resulting from the COVID-19 pandemic. COVID-19 has had far-reaching impacts on agricultural trade, manufacturing, consumer demand, and prices. The impact on the global cotton value chain has put pressure on all sectors of the value chain. The containment measures that have eff ectively halted an overwhelming portion of the global economy have and will continue to have deep impacts on the cotton sector. This brief provides an initial assessment of the impacts of the Great Lockdown on cotton supply and demand, prices and trade followed by recovery prospects and recommendations.

Supply and Demand

• The ICAC’s global production estimate for 2019/20 is at 26.2 million tonnes with production for 2020/21 currently estimated at 25.2 million tonnes, a 4% decrease as global area decreases based on lower prices. • Global consumption for 2019/20 is currently estimated at 23 million tonnes from the additional pressure of containment measures and the continual pressure of global trade tensions. With decreasing use, ending stock levels are expected to rise to 21.8 million tonnes with the stocks-to-use ratio at record high levels. • Cotton consumption and GDP growth are correlated. When GDP growth has slowed, consumption growth has followed. The current IMF projection of a 3% contraction in the global economy is expected to contribute to a 11% decrease in cotton consumption. However, as GDP growth accelerates, consumption growth recovers. • While the IMF’s current projection for a 3% decline in GDP is more severe than the 2008 financial crisis, this crisis diff ers in that it was induced by a public health event rather than weak policies in the financial sector signalling the possibility of a smoother and swift er recovery under appropriate policy responses. • The widespread lockdown has resulted in record levels of unemployment. While there has been an increase in online shopping in some countries, retail activity in the textile and apparel sector has slowed. The retail sales of clothing and clothing accessories in the U.S. fell by 79% between February and April 2020. While consumers may expect to see income losses in the short term, expectations of increased spending should be anticipated as economies recover, thus indicating that with economic recovery, apparel and textile purchases should be expected to rebound. • While both luxury and fast fashion brands have lost market capitalisation since the outbreak of COVID-19, the fall in value terms has been more severe for luxury brands than for fast fashion brands. Because fast fashion brands cater to more income- and price-sensitive consumers, it is expected that consumers of fast fashion brands will take longer to return to stores than the consumers of luxury brands. • The ITMF in March-April conducted a couple of surveys on the COVID-19 impact on the global textile industry. The survey reached 700 companies and indicates that in 2020, cancellations of orders could reach 31% and the employee turnover could reach 28%. That could mean total losses for the global textile industry of about $300 billion. • With higher incomes, consumers in Europe, the United States and Japan are responsible for importing 61.5% of the global apparel imports. However, with increasing wealth, other consumers in Asia, particularly in China and Korea, are responsible for emerging growth with 13.7% and 15.9% growth in imports from 2017 to 2018. Recovery from the pandemic lockdown has already begun in China and many other Asian countries as containment measures have been eased and businesses begin to reopen.

Prices

• Containment measures have driven most commodity prices down. Nevertheless, agricultural food prices are expected to remain broadly stable in 2020 as they are less sensitive to economic activity than industrial commodities. • The dollar has emerged again as the preferred currency by investors, reinforcing its great influence on the world economy. The currencies of major cotton consuming and producing countries have lost value against the US dollar. The Mexican peso (24.8%) and the Brazilian real (36.3%) have witnessed the greatest fall since January 2020, making them one of the worst-performing currencies against the dollar. • Cotton prices will remain under pressure due to several factors, including higher ending stocks in the current and next season, weaker textile fibre demand from brands and retailers, and lower polyester prices. If the price gap between cotton and polyester continues to widen, this would reduce cotton’s competitiveness and decrease its world share of textile fibre consumption.

Trade

• The top three largest importers of textile and apparel products by value (the European Union, the United States and Japan), have significantly reduced textile and apparel imports in Q1-2020. Since late February, many textiles and apparel export orders have been cancelled or delayed and major retail companies have filed for bankruptcy. Short-term prospects for the textile and apparel industry are expected to be grim. • Cotton merchants risk a decline in the value of trade because of contract cancellations and market losses. Storage charges may represent costs of $16 million per month. The losses to the merchant sector caused by the contract cancellations linked to COVID-19 will likely cause more firms to exit the cotton trading industry.

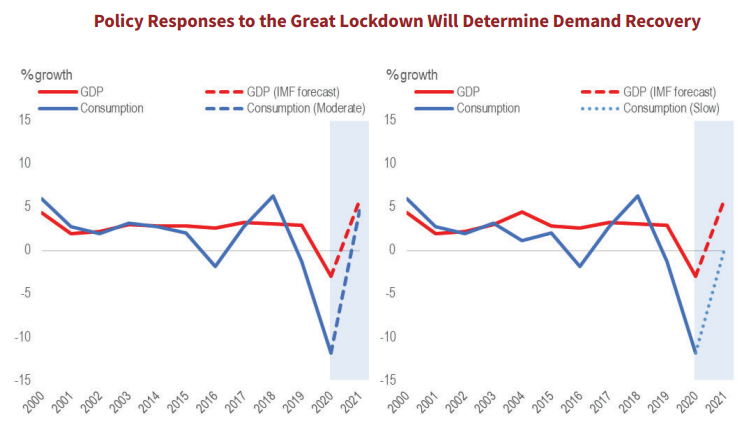

Recovery Scenarios

• A moderate recovery could be envisioned in a ‘new normal’ with safety ensured by proper local and national government responses and policies, businesses could safely reopen, and economic activity could begin to increase with appropriate precautions being taken to provide for health and wellbeing. • A slower recovery could be envisioned where either stringent containment measures remain in place and government policies including those for public health systems, small business and unemployment remain weak or ineff ective. A slow recovery extending beyond 12 to 18 months with little action to promote consumer demand would lead to a more severe contraction in cotton mill-use in 2021. With the global 20/21 production estimated at 25.1 million tonnes, an additional economic slowdown and slow consumption growth would increase pressure on ending stocks which in turn increase downward pressure on prices. In a prolonged crisis, food security would become an important issue and smallholder farms in developing economies would likely switch to food crops.

Recommendations

• Enforcing contracts is fundamental if markets are to function properly and promotes business expansion, trade, investment, economic growth and development. • Public health and safety need to be assured through appropriate precautions by local and national governments responses and polices as physical businesses reopen and economic activity increase. • Stimulus measures and financial support to small and medium enterprises to reduce the financial burden, including loans, grants and credits to support liquidity. • Income support during temporary unemployment to support income losses for standard and nonstandard employment. • Be careful that agricultural support and subsidies provide income to support to farmers do not have unintended consequences (e.g. increasing supply that further push down prices).

Source: ICAC