Executive Summary

Highlights from the April 2022 Cotton This Month include:

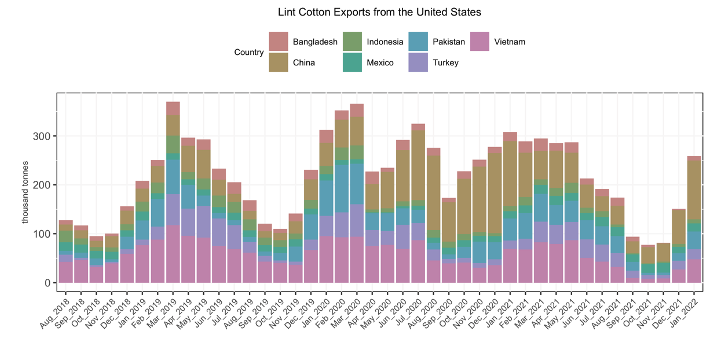

- Data regarding US cotton exports indicate the logistics situation is improving worldwide

- While a positive sign worthy of optimism, the USA has capabilities that many other countries don't so the rest of the world might recover more slowly

- Production is down slightly from the previous report but is holding at 26.43 million tonnes

- Global consumption is currently being reported at 26.16 million tonnes

New Data Shows Global Transportation Issues Might Be Improving

Don't look now, but global cotton logistics might be starting to sort themselves out after a long and painful struggle through the Covid pandemic. We can't yet say with 100% certainty that things are going to improve in the immediate future because the conclusions were drawn solely from US export data. The USA has greater means to effect changes than most other countries so not all regions will recover as quickly, but it remains the world's largest exporter and thus can serve as a sort of 'canary in the coal mine' for worldwide cotton shipping and logistics.

Consumption remains strong as we approach the end of the 2021/22 season. Global consumption is currently being reported at 26.16 million tonnes. Production is down slightly from the previous report but is holding at 26.43 million tonnes, still sufficient to accommodate consumption. If we look at the total global supply and demand numbers we do see a minor deficit in supply. Global supply is currently sitting at 57.129 million tonnes while global demand is 57.133 million tonnes.

The Secretariat’s current price forecast of the season-average A index for 2021/22 ranges from 106 cents to 126 cents, with a midpoint at 113 cents per pound.