By Jim Steadman

Here we go again. Stepping out into the unknown. Sticking our necks out to kickstart the new year’s cotton acreage projection game once more.

In reality, Cotton Grower’s track record for acreage projection has been pretty good for the past several years. And, if nothing else, it gives the industry something to ponder and/or poke fun of until the more esteemed scientific surveys from the National Cotton Council and USDA are released in the coming months.

As always, these acreage projections are based on input and conversations with multiple stakeholders in the cotton industry — our readers, state cotton specialists, economists, and others related to U.S. cotton. It’s a reporting job with math involved, and we try to do our best with the information we get.

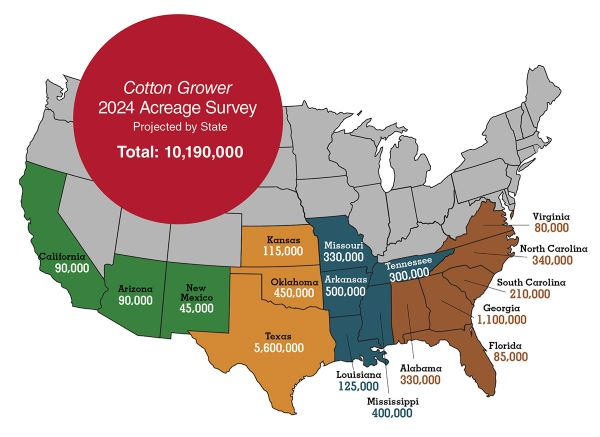

That said — and based on the information in hand as of mid-December — U.S. cotton growers are projected to plant a total (upland and Pima) of 10.19 million acres in 2024. That’s a decrease of roughly 42,000 acres from USDA’s 2023 reported plantings last October, or approximately .5% down from 2023’s pre-harvest numbers.

In essence, our calculations show no significant change in cotton acreage from late 2023.

What Happened?

One year ago, U.S. cotton growers were feeling pretty good about their crop prospects for 2023. Prices were still acceptable (but not high), and early season moisture gave hope for a good start to the year across most of the Cotton Belt. Flooding issues washed some traditional cotton acres in California and Texas away to alternative crops, and another summer of searing heat baked away prospects of favorable yields, especially across the Southwest, still reeling from the effects of the historic drought of ’22.

USDA’s final October tally of 10.23 million acres shows how much Mother Nature and other market forces took out of the early 2023 projections of 11.0 to 11.5 million acres.

As expected, there was one overriding comment in nearly every response we received — cotton prices in relation to other commodities will strongly influence cropping decisions and acres for 2024. Of course, continuing inflation concerns, global demand for cotton, political and geopolitical issues, and continued high production costs certainly have an impact, too.

“If you look at the historical corn/cotton ratio, the results point to about 10.8 million acres of cotton,” says Dr. Darren Hudson, Professor and the Larry Combest Endowed Chair for Agricultural Competitiveness and Director of the International Center for Agricultural Competitiveness at Texas Tech University. “The problem is the ratio doesn’t capture our current level with 77-cent cotton and $5 corn. The ratio would suggest it’s more favorable to cotton this year than last year. But my gut tells me that at 77 cents, we’re just not going to get a lot of it.”

Here are the survey results on a regional basis.

Southeast

Overall, sources in Alabama, Florida, Georgia, the Carolinas, and Virginia indicated they’ll plant 2.15 million acres of cotton in 2024, an 8% decrease from 2023. As the number indicates, acreage across the region should hold relatively steady, especially in Georgia, to slightly down. No acreage increases were anticipated in any of the region’s states.

“Multiple factors are depressing cotton,” says Steve Brown, Alabama Extension Cotton Specialist. “The price is not in the upper 80s or better. Severe drought in southwest Alabama and harvest season rainfall were disappointing. And rising input costs remain.”

“In North Carolina, meaningful improvements in price would likely increase our acreage noticeably,” says Guy Collins, North Carolina State Extension Cotton Specialist. “Severe drought in some places in 2023 may affect some acreage decisions.”

“I’m generally an optimist when it comes to acreage, but I’d predict Georgia stays stagnant at best compared to 2023,” says Camp Hand, University of Georgia Extension Cotton Specialist. “We still have more infrastructure in place for cotton compared to corn, and there aren’t many other options to break a dryland peanut rotation other than cotton. We are a cotton state. And in my mind, we will stay that way for the foreseeable future.”

Mid-South

Most Mid-South states are projecting flat to slightly decreased acreage for 2024, with the exception of Tennessee where a slight increase is indicated. All totaled, the survey results show 1.65 million acres for 2024 across the five-state region.

“I think acres will be pretty flat,” says Brian Pieralisi, Mississippi State Extension Cotton Specialist. “It’s really hard to say for sure with south Mississippi still in such a drought. I wouldn’t expect a large increase in acres as long as prices stay in the 80-cent range.”

“Looking at futures for cotton, the price appears to be holding flat, and I’m sure most potential growers would be more comfortable with it higher,” notes Trey Price, LSU Extension Cotton Specialist. “All that being said, I don’t expect to see much of an increase in cotton acreage, if any.”

“I expect we will pick up just shy of 50,000 acres to bring us back to the 300,000-acre mark in Tennessee, with a plus or minus of about 75,000,” predicts Tyson Raper, University of Tennessee Extension Cotton Specialist. “The 2023 Tennessee crop was nothing short of incredible, and I suspect the subsequent excitement with the commodity will push our increase. But there’s a long way to go before May!”

Southwest

The lingering effects of the 2022 drought combined with triple-digit summer heat to hamper cotton production across the region. Overall, production results were marginally better than 2022, as some areas did fine while growers in other parts of the region faced another year of insurance claims and abandoned acres.

Based on our survey input, Kansas, Oklahoma, and Texas growers anticipate planting a combined 6,165,000 cotton acres in 2024 — a very slight .8% increase from final planted acres in 2023.

West

Once again, grower decisions on cotton in California, Arizona, and New Mexico continue to hinge primarily on water availability and cotton price. In 2023, final USDA numbers showed 239,000 acres of cotton across the three states. Projections for 2024, based on current input, show approximately 225,000 total cotton acres for 2024 across the region — a nearly 6% decrease.

Snapshot in Time

For the second consecutive year, primarily due to current cotton prices and other uncontrollable market factors, few respondents were fully confident in their projections. Some, in fact, would not be surprised to see 9.8 million acres while others could potentially see up to 10.5 million acres. This is our best guesstimate for now.

The Cotton Grower survey reflects a snapshot of the market situation and prevailing attitudes in late November and early December, as 2023 harvest was still wrapping up in some areas. Many thanks to the growers, ginners, consultants, specialists, and other industry sources for their input.

Source: cottongrower.com