- Typically, domestic cotton prices toe the international trend, which has seen a moderation in the last few months

- Analysts said the cotton price spread, which is the difference between the price of yarn and raw cotton, has fallen from 80-85 per kg in April to 75 in October

Cotton mills may not spin a robust performance in fiscal year 2020. Despite higher crop output in the current cotton season, prices have not eased much. Meanwhile, yarn exports are far from encouraging. As a result, profits of spinning mills will be squeezed between weak revenue and high input costs.

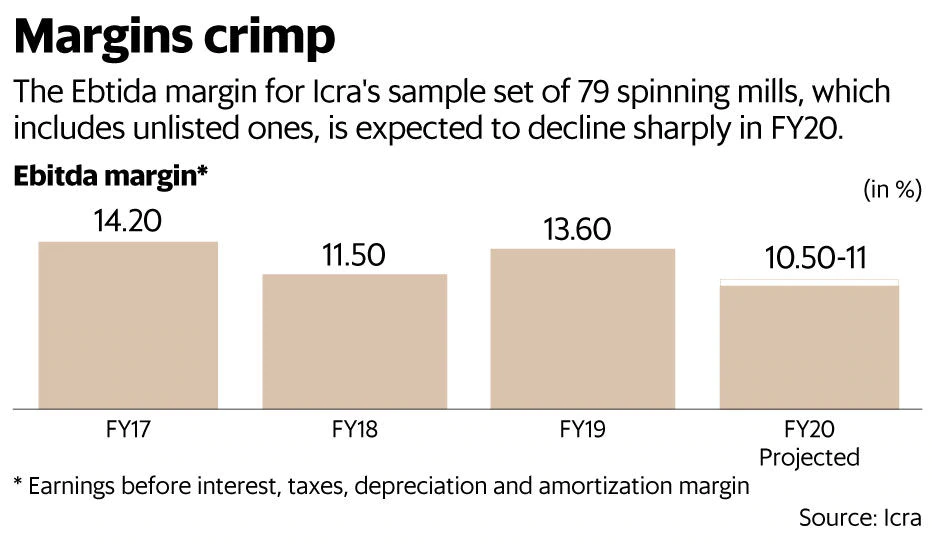

In fact, Icra Ltd estimates the average operating margin of 79 spinning mills to shrink by 200-400 basis points (bps) year-on-year (y-o-y) in FY20. This is higher than the 100-150bps margin contraction forecast in May.

Typically, domestic cotton prices toe the international trend, which has seen a moderation in the last few months. However, this time around, the government’s move to increase the minimum support price for the benefit of farmers has supported Indian prices. So, while international prices have fallen by 15% after a bumper crop in the US and Brazil, domestic cotton prices dipped by about 10%.

Be that as it may, the bigger problem is that demand for textiles and yarn has been weak. The US-China trade war led to a demand slump for yarn in international markets. Apart from China, demand from Vietnam, Bangladesh and other neighbouring nations have not been upbeat. Not surprisingly, cotton yarn exports in the first seven months of FY20 were down by about 40% and prices have been weak.

Cut to the home turf, festive sales (September-October) for textiles inched up slightly, but dropped again, keeping with the consumption slowdown in other sectors.

Analysts said the cotton price spread, which is the difference between the price of yarn and raw cotton, has fallen from 80-85 per kg in April to 75 in October. This signals weaker profit margins in the coming quarters. After all, raw cotton accounts for 65% of the total operating cost of spinning mills.

That said, the drop in cotton prices in November has raised hopes for yarn mills. Profitability of mills may get a leg up in the second half of FY20. “However, this may not be sufficient to offset the steep negative impact on profitability seen in the first half," said Sushant Sarode, associate director, Crisil.

The scenario is tougher for smaller mills. Their working capital costs are higher than large and integrated mills, on account of higher interest cost and inventory.

Larger mills also have superior customer profiles, diverse product mix and the ability to manufacture a wide range of yarn counts. Listed firms, such as Vardhman Textiles Ltd, KPR Mill Ltd and Ambika Cotton Mills Ltd, have therefore maintained profitability in the last few quarters, despite the odds. Yet, the stock prices have fallen 10-30% in the past one year due to the overhang of weak demand for yarn. The gloom among spinning mills is likely to continue unless exports and domestic consumption rev up to improve profitability.