U.S. cotton producers intend to plant 13.1 million cotton acres this spring, up 3.7 percent from 2017, according to the NCC’s 37th Annual Early Season Planting Intentions Survey.

MEMPHIS, Tenn. – U.S. cotton producers intend to plant 13.1 million cotton acres this spring, up 3.7 percent from 2017, according to the National Cotton Council’s 37th Annual Early Season Planting Intentions Survey. (see table below)

Upland cotton intentions are 12.8 million acres, up 3.8 percent from 2017, while extra-long staple (ELS) intentions of 254,000 acres represent a 1.0 percent increase. The survey results were announced today at the NCC’s 2018 Annual Meeting in Fort Worth, Texas.

Dr. Jody Campiche, the NCC’s vice president, Economics & Policy Analysis, said, “Planted acreage is just one of the factors that will determine supplies of cotton and cottonseed. Ultimately, weather, insect pressures and agronomic conditions play a significant role in determining crop size.”

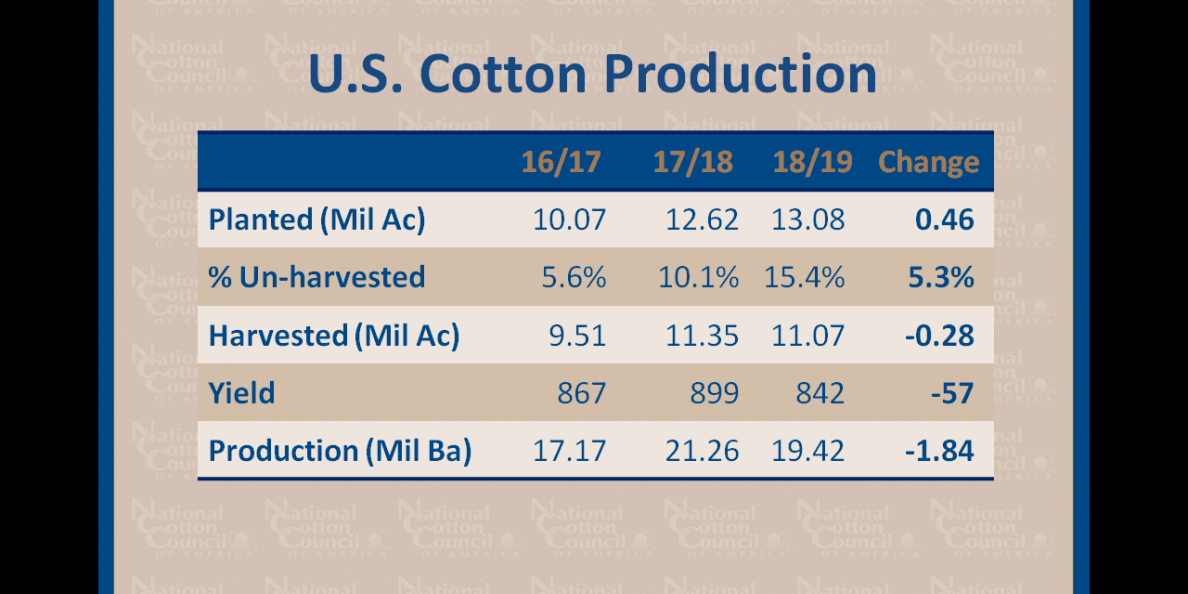

She said that with abandonment assumed at approximately 15 percent for the United States, Cotton Belt harvested area totals 11.1 million acres. Using an average U.S. yield per harvested acre of 842 pounds generates a cotton crop of 19.4 million bales, with 18.7 million upland bales and 744,000 ELS bales.

The NCC questionnaire, mailed in mid-December 2017 to producers across the 17-state Cotton Belt, asked producers for the number of acres devoted to cotton and other crops in 2017 and the acres planned for the coming season. Survey responses were collected through mid-January.

Campiche noted, “History has shown that U.S. farmers respond to relative prices when making planting decisions. During the survey period, cotton futures prices were stronger relative to competing crops. The price ratios of cotton to corn and soybeans are more favorable than in 2017. However, soybeans are expected to provide competition for available acres in 2018, due in part to the lower production costs relative to cotton. While cotton prices have improved relative to other crops, cottonseed prices are at the lowest level since the 2006 marketing year, thus increasing the net costs of ginning.”

Survey respondents in the Southeast indicate a 2.3 percent increase in the region’s upland area to 2.6 million acres. All six states show an increase in acreage. In Alabama, the survey responses indicate 0.8 percent more cotton acreage and less wheat, soybeans, and ‘other crops’. In Florida, respondents indicated more cotton and soybeans and less ‘other crops’, likely peanuts. In Georgia, cotton acreage is expected to increase by 0.6 percent. Georgia growers expect to plant less soybeans and more corn and ‘other crops’, likely peanuts. In North Carolina, an 8.2 percent increase is expected as acreage moves away from soybeans. In South Carolina, cotton acreage is expected to increase by 3.4 percent, while corn acreage is expected to decline. Cotton acreage is expected to increase by 3.1 percent in Virginia as acreage moves away from wheat and ‘other crops’.

In the Mid-South, growers have demonstrated their ability to adjust acreage based on market signals. The relative prices and potential returns of competing crops play a significant role in cotton acreage. Mid-South growers intend to plant 1.9 million acres, a decrease of 0.1 percent from the previous year as some land is shifted to soybeans. Across the region, Louisiana and Mississippi intend to decrease cotton acreage and Arkansas, Missouri, and Tennessee expect to increase acreage. The largest decline was reported in Mississippi with 5.5 percent less cotton acreage in 2018. In Tennessee, cotton acreage is expected to increase by 1.5 percent as land shifts away from corn and wheat. Missouri growers expect to increase cotton acres by 3.8 percent and plant less corn and soybeans. In Louisiana, respondents intend to plant 2.6 percent less cotton acreage, more soybeans, and less of all ‘other crops’. All states in the Mid-South except Missouri intend to plant more soybeans in 2018.

Southwest growers intend to plant 8.0 million acres of cotton, an increase of 5.7 percent. Increases in cotton area are expected in each of the three states. In Kansas, producers intend to plant 55.3 percent more cotton acres, along with more wheat and ‘other crops’, likely sorghum. Kansas growers intend to plant less corn and soybeans. In Oklahoma, a 21.0 percent increase in cotton acreage is expected as wheat acreage declines. Oklahoma respondents report a small increase in ‘other crops’. Overall, Texas acreage is expected to increase by 3.7 percent. Texas respondents expect to plant more wheat acres and less corn and ‘other crops’.

Far West producers are expecting to plant 293,000 upland cotton acres – a 6.8 percent decrease from 2017. Arizona is responsible for the largest decrease, with California acreage down slightly and New Mexico acreage up slightly. The survey results for Arizona suggest a shift from upland cotton to ELS cotton, corn, and ‘other crops’. In California, growers intend to plant more wheat and corn.

Many producers will continue to face difficult economic conditions in 2018. Production costs remain high, and unless producers have good yields, current prices may not be enough to cover all production expenses.

NCC delegates were reminded that these expectations are a snapshot of intentions based on market conditions at survey time. Actual plantings will be influenced by changing market conditions and weather.

# # #

Prospective 2018 U.S. Cotton Area

|

2017 Actual (Thou.) 1/ |

2018 Intended (Thou.) 2/ |

Percent Change |

|

| SOUTHEAST |

2,523 |

2,582 |

2.3% |

| Alabama |

435 |

439 |

0.8% |

| Florida |

99 |

106 |

6.9% |

| Georgia |

1,280 |

1,287 |

0.6% |

| North Carolina |

375 |

406 |

8.2% |

| South Carolina |

250 |

258 |

3.4% |

| Virginia |

84 |

87 |

3.1% |

| MID-SOUTH |

1,945 |

1,943 |

-0.1% |

| Arkansas |

445 |

466 |

4.7% |

| Louisiana |

220 |

214 |

-2.6% |

| Mississippi |

630 |

596 |

-5.5% |

| Missouri |

305 |

317 |

3.8% |

| Tennessee |

345 |

350 |

1.5% |

| SOUTHWEST |

7,578 |

8,007 |

5.7% |

| Kansas |

93 |

144 |

55.3% |

| Oklahoma |

585 |

708 |

21.0% |

| Texas |

6,900 |

7,154 |

3.7% |

| WEST |

314 |

293 |

-6.8% |

| Arizona |

160 |

138 |

-13.5% |

| California |

88 |

78 |

-10.8% |

| New Mexico |

66 |

76 |

14.6% |

| TOTAL UPLAND |

12,360 |

12,824 |

3.8% |

| TOTAL ELS |

252 |

254 |

1.0% |

| Arizona |

15 |

20 |

31.6% |

| California |

215 |

212 |

-1.3% |

| New Mexico |

8 |

8 |

4.8% |

| Texas |

14 |

14 |

2.9% |

| ALL COTTON |

12,612 |

13,078 |

3.7% |

| 1/ USDA-NASS | |||

| 2/ National Cotton Council | |||