By Jim Steadman

This might have been easier with a blindfold and a dart board.

Granted, Cotton Grower’s annual cotton acreage survey could/should never be mistaken for true scientific research. We leave that to the National Cotton Council and USDA, and we’ll hear from them soon. But it is based on input and conversations with multiple stakeholders in the cotton industry — our readers, state cotton specialists, economists, and others related to U.S. cotton. It’s a reporting job, and we try to do our best with the information we get.

With that disclaimer out of the way, there was one overriding comment in nearly every response we received — cotton prices in relation to other commodities will strongly influence cropping decisions and acres for 2023. And, of course, that pesky cost of production in inflationary times will certainly have an impact, too.

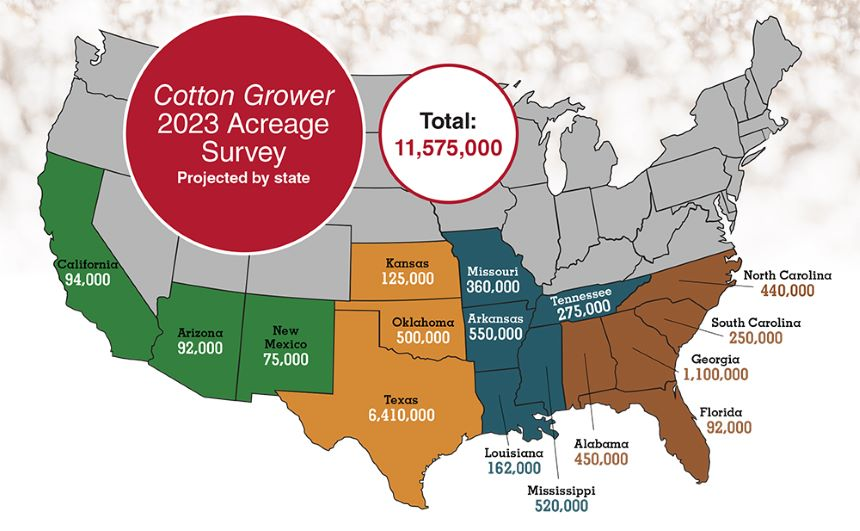

That said — and based on the information in hand as we go to press — U.S. cotton growers are projected to plant a total (upland and Pima) of 11.57 million acres in 2023. That’s a drop of roughly one million acres from USDA’s 2022 reported plantings last June — a 7% decrease. That’s not surprising.

Let’s look at what some of our respondents told us on a regional basis.

Southeast

Overall, sources in Alabama, Florida, Georgia, the Carolinas, and Virginia indicated that they’ll plant 2,412,000 acres of cotton in 2023 — a 4% decrease from 2022. As the number indicates, acreage across the region should hold relatively steady to slightly down — due, again, to market prices and input costs. Only Alabama anticipates an acreage increase.

“Once we reached mid-September 2022, we had great weather for cotton in terms of yield and quality preservation, as well as harvest operations,” reports Steve Brown, Alabama Extension Cotton Specialist. “Overall, we had better– than– expected yields in many areas. Our irrigation capacity is limited even where we have it (less than 10% of our total acreage), and corn was severely challenged in 2022. With such limitations, cotton is a superior alternative to corn.”

“Acres in North Carolina will largely depend on cotton prices and prices of other commodities, mainly corn and beans, as we move into the new year and approach planting season,” says Guy Collins, North Carolina State Extension Cotton Specialist. “Most folks have had two good years in a row, so there are no complaints about cotton at the moment. If cotton prices are low and other commodities are not as we approach planting season, our acreage will likely be less. If prices of all commodities are noticeably lower, the key for cotton success will depend on if production costs decrease proportionately, which looks doubtful.”

“I think that with the price of cotton below what it was this time a year ago and the price of inputs remaining stagnant, growers’ intentions as of right now are probably to plant less cotton than in 2022,” adds Camp Hand, University of Georgia Extension Cotton Specialist. “However, there are very few crops that fit in our rotations as well as cotton. Soybeans and corn will be attractive to growers but only fit on irrigated acres, and soybeans don’t fit our rotation with peanuts.”

Mid-South

Although most Mid-South states are projecting slight acreage decreases for 2023, those losses appear to be offset by slight increases in Arkansas and Mississippi. When totaled, the survey results show 1.86 million acres for 2023 across the five-state region.

“I don’t recall a year with more uncertainty on acreage intent,” says Tyson Raper, University of Tennessee Extension Cotton Specialist. “I believe we will likely have a slight decline in acreage, but I don’t know where the floor might be for 2023. With current input prices, many growers seem lukewarm on cotton. Double cropped wheat and soybeans and full season soybeans will likely take a portion of the cotton acres for 2023.”

“I am expecting cotton numbers to be similar in southeast Missouri for the 2023 compared to 2022,” projects Bradley Wilson, University of Missouri Extension Cotton Specialist. “We had 360,000 estimated acres in 2022, and acreages are likely to remain steady around this number in 2023. Prices are trending lower in 2023 than 2022 but are near 80 cents at this time, which will keep our acres in Missouri for the 2023 season.”

On the flip side, LSU Extension Cotton Specialist Matt Foster expects to see a 20,000+ acre decrease for cotton in the state. “I believe cotton acreage will decrease in 2023 due to lower price and a lower state average yield for the 2022 crop due to adverse weather conditions,” he says.

Southwest

Here’s where projections start to get tricky. After anticipating more cotton acres in 2022, the Southwest states were hammered by drought and heat all season, resulting in a high percentage of insurance claims and abandoned acres. Although most of the region has received recent rains, it hasn’t been enough to reduce overall drought levels. And there are still concerns about how much soil moisture will be available at planting.

Based on our survey input, Kansas, Oklahoma, and Texas acres combined anticipate planting 6,535,000 cotton acres in 2023 — down roughly 16% from planted acres in 2022.

“Because the price of wheat is so high, we might see cotton acres drop 5% to 10%,” explains Dr. John Robinson, Texas A&M AgriLife Extension Cotton Marketing Specialist. “But growers will still go with cotton because it’s the best thing to grow if it’s dry and the best thing to pencil out as an insurance loss. Either way, it’s the most rational thing to do.”

Western

Once again, grower decisions on cotton in California, Arizona, and New Mexico hinge entirely on water availability — or the lack thereof. Water stresses for the region in 2022 were severe. And although recent rains will help, there are still few signs of improvement in place (or sight) heading into 2023.

At press time, respondents were not optimistic about cotton’s chances in the region, with projected acreage decreases of ranging from 20% for Pima to as much as 40% for upland. That pencils out to approximately 261,000 total cotton acres for 2023 across the three states — a 14.7% decrease of roughly 45,000 acres.

Snapshot in Time

Quite honestly, this year’s survey has more uncertainty and trap doors due to uncontrollable market factors than in previous years. Few respondents were fully confident in their projections. This is the best guesstimate we have at this time.

The Cotton Grower survey reflects a snapshot of the market situation and prevailing attitudes in late November and early December as 2023 harvest was still wrapping up in some areas. Many thanks to the growers, ginners, consultants, specialists, and other industry sources for their input.

We look forward to the projections coming from the National Cotton Council in February and from USDA-NASS in March.