A major slowdown in textile exports is on the cards. Or at least that is the indication from the latest monthly trade report card from Pakistan Bureau of Statistics. Per PBS, the industry witnessed a double- digit decline in volume exported across most low to medium value-added segments during 4M-FY23 (July – Oct). In fact, were it not for the wearing apparel segment holding ground, textile export earnings would have already turned red.

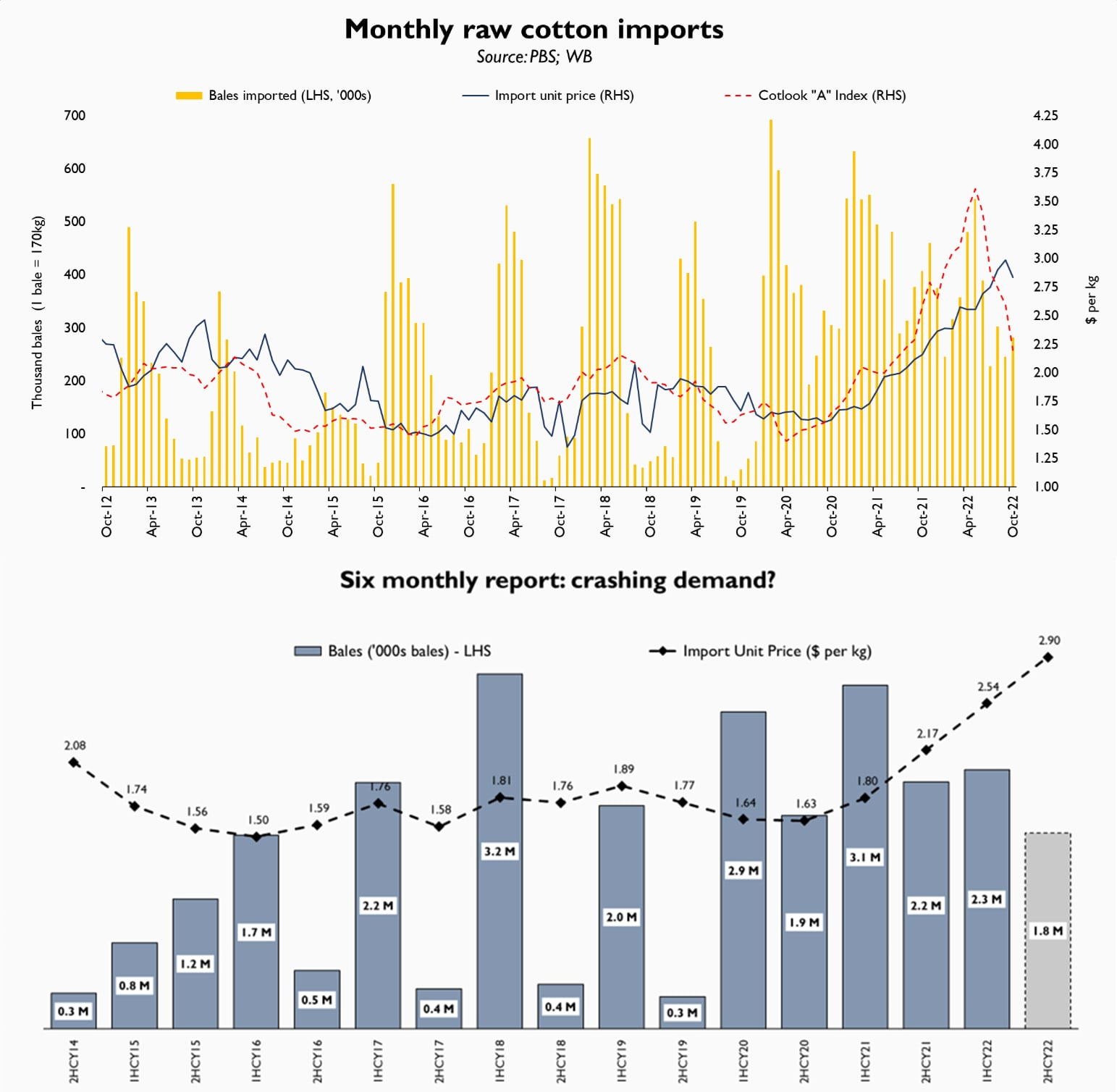

But the slowdown is fast spreading its roots, and it won’t be long before the wearing apparel category surrenders too. Or so it seems looking at the 4M-FY23 profile of raw cotton imports. According to PBS, Pakistan imported a little over one million bales (of 170 kg) during July – Oct 2022, its lowest cotton imports for a four-month period since Sep – Dec 2019.

That, however, wouldn’t be a fair comparison. Back then, cotton imports used to suffer from a very high tariff between July – Dec, that aimed to protect local farmers during marketing season. Excluding the high tariff period, these may be lowest cotton imports in over a decade. This comes at a time when floods have reportedly devastated local cotton, with projected seasonal arrivals falling in the vicinity of 4.5 – 5.5 million bales (of 170kg).

If the current trend of monthly average imports of 0.25 million bales continues, annual imports would be no more than 3 million bales, lowest since FY16 when domestic cotton production stood at 10 million bales. For much of the past decade, cotton consumption by milling segment has averaged between 12.5 – 13.5 million bales, with imports supplying as much as 40 percent of national demand in recent years. However, it looks as though mill consumption may drop precipitously during the ongoing fiscal, as both local production and import are falling.

Of course, both pricing and demand from downstream industry have played a role. First, as world cotton prices have crashed some 50 percent between May and November 2022, the industry is looking for fresh contracts at lower prices. Since August 2022, the average unit price of cotton imported into the country during a given month has exceeded monthly average price in the international market during the same period.

This is a sharp reversal from the earlier trend that manifested itself post-Covid when monthly average prices in the international market were consistently higher than the average unit price of imported cotton during that period. It appears that the local industry had bet big on rising cotton prices in the world market and is now sitting on piled up inventory procured at peak prices, while recession creeps across major exporting destinations. Which may also explain why despite a precipitous fall in overall cotton availability in the local market for rest of the fiscal year, the output figures coming out of the spinning and cloth weaving industry have so far not mirrored the tightening conditions in the raw material (fiber) market.

Come 2023, cotton import may very well pick up once local arrivals fully dry up and winter season is over, offering more clarity on the true scale and extent of recession in the textile exporting destinations. However, even if average monthly cotton import doubles from here on, it would still struggle to top peak import volume 5 million bales witnessed over the last two years.

That textile export volumes will drop significantly on full-year basis during FY23 now seems inevitable. Whether falling demand will also immediately translate into lower selling prices for value-added products, remains to be seen. The last time world cotton prices averaged below 80 cents for a sustained period, Pakistan’s textile export earnings came to a standstill (FY15 – FY20). Will they play out differently this time? Don’t count on it.