February 18, 2022

- Import and Export Prices Higher Than Expected

- China, Vietnam, and Turkey Week’s Highest Buyers

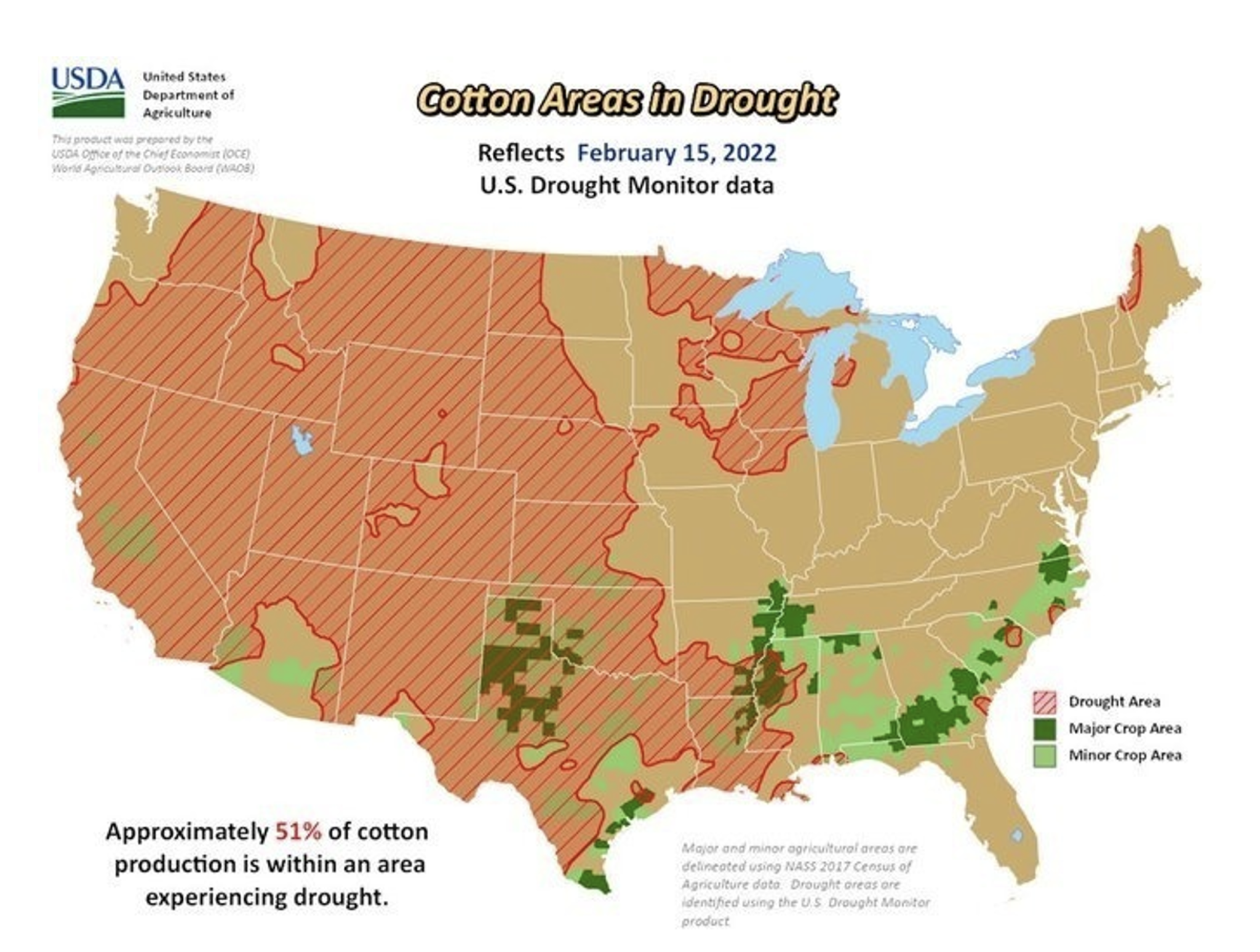

- Drought Conditions May Worsen Before Improving

Futures trended lower since last Friday. From this week until June, we will transfer focus to the May contract given that March futures enter the notice period next Tuesday. May futures fell from last Thursday’s close at 123.20 cents per pound in a sharp drop on Friday. Although prices steadied somewhat early in this week, May futures made their way to the week’s low at 118.76 cents on Wednesday before steadying again. Prices settled at 119.52 on Thursday, down 368 points for the week. Trading volumes fell dramatically as Index Fund rolling finished last Friday. Open interest was also sharply lower, reflecting both March option expiration and traders exiting longs. The total number of open contracts fell 25,196 to 241,893.

Outside Markets

It was a volatile week for outside markets. Friday showed that consumer sentiment sank in January, and on Tuesday data showed that producer prices had also risen more than expected. On the bright side, seasonally adjusted retail sales advanced 3.8% vs December, much more than the 2.0% expected. In fact, January sales were up 13% year over year. Apparel sales were a shining star in the report, with clothing store sales in January up 19% from January 2020 and registering as the best January clothing store sales ever. Unfortunately, import and export prices were also higher than expected, and the release of the Federal Open Market Committee’s meeting minutes confirmed that the Federal Reserve officials are likely to act swiftly and strongly to temper inflation by raising interest rates and selling assets. That news, in combination with the prospect of conflict in Ukraine, continued to whipsaw the markets, leaving the major stock indices down 3-4% for the week.

Export Sales

High prices have still done little to curb demand for U.S. cotton. Exporters were able to book another 158,500 bales of Upland and 3,100 bales of Pima in the week ending February 10. The largest buyers included China (47,800 bales), Vietnam (23,800), Turkey (22,300), and Peru (11,900). Shipments were less than many expected at 270,000 bales, but it is likely that the lower number reflects disruptions caused by the ice storms that swept across the Cotton Belt during that time. Demand for next year’s crop remains healthy as well, with mills ordering 34,700 bales for delivery in the next marketing year.

Weather and New Crop Outlook

While some of the Cotton Belt is getting some relief from the storm that is still moving through, West Texas mostly missed out on the rains. Unfortunately, little has changed in the long-term outlook for our region and many forecasters are calling for the current drought conditions to worsen before they get better. There are a few indications that some lucky rains could sneak through, but the backdrop for the region remains lower than average precipitation and higher than average temperatures through the Spring. Anything can happen from now until the final planting dates, but most pundits are assuming abandonment will be high this year. In any case, drought years like this make forecasting the crop almost as difficult as growing it.

The Week Ahead

Next week’s attention will continue to give a huge share to currently heightened international risks. The lack of certainty about Fed policy is also taking a toll on markets. Cotton market watchers will continue to look at the weekly export sales for any sign of slowing demand or accelerating shipments, as many bears have made the slow pace of shipments a key point of concern.

In the Week Ahead:

- Friday at 2:30 p.m. Central – Commitments of Traders

- Thursday at 7:30 a.m. Central – Export Sales Report

- Thursday at 2:30 p.m. Central – Cotton-On-Call