February 25, 2022

May Futures Settled Down 36 Points for the Week

The First Look at the USDA’s 2022/2023 Cotton Outlook

Spinning Mills Continuing to Book More U.S. Cotton

Prices were relatively range-bound until Thursday, when May futures exploded to 125.13 cents overnight as the news of Russia invading Ukraine hit and then plummeted to a low of 118.86 cents later in the day. May futures settled at 119.16 cents, down 36 points for the week. The heavy volume of cotton trading seems to have flowed with the selloff that stocks and other soft commodities faced during U.S. trading hours. Prior to Thursday, cotton’s open interest had lost 3,667 to settle at 238,226 contracts.

Outside Markets

Nothing seems to matter more than Mr. Putin invading Ukraine. The U.S. intelligence community seems to have improved recently, having broadcast the play-by-play months in advance. Mr. Putin ordered a “special operation” to “demilitarize” Ukraine, which involves moving amassed Russian forces across the border, suppressing Ukraine’s air defenses with targeted strikes, shutting off Ukraine’s ports, and moving troops to Kyiv (the capital city) as quickly as possible. As Russia is a large supplier of fuels, oil spiked over $100 per barrel Wednesday night. Both Ukraine and Russia are large grain exporters, so the grain markets flew higher as well. Wheat prices spent the day locked limit up (at the maximum daily price increase).

What comes next is not totally clear, but the West seems fairly united in its reaction to cut Russia off from international trade and to freeze Russian assets in their countries. In fact, the Ruble traded to its lowest level ever versus the U.S. Dollar, which strengthened sharply as the safe-haven currency. International stocks also tumbled on the news, with the S&P 500 falling as much as 2.6% before regaining footing and heading back into positive territory. By contrast, the MOEX Russia Index collapsed 33%, erasing all gains since 2017. Some major banks have even cut the margin values of Russian bonds to zero and are asking investors to cover margin call. Nevertheless, Russian energy firms have, so far, managed to escape sanctions in admission of Europe’s continuing reliance on Russia’s oil and gas, but further sanctions could be forthcoming. The end of this story is not written.

USDA Agricultural Outlook Forum

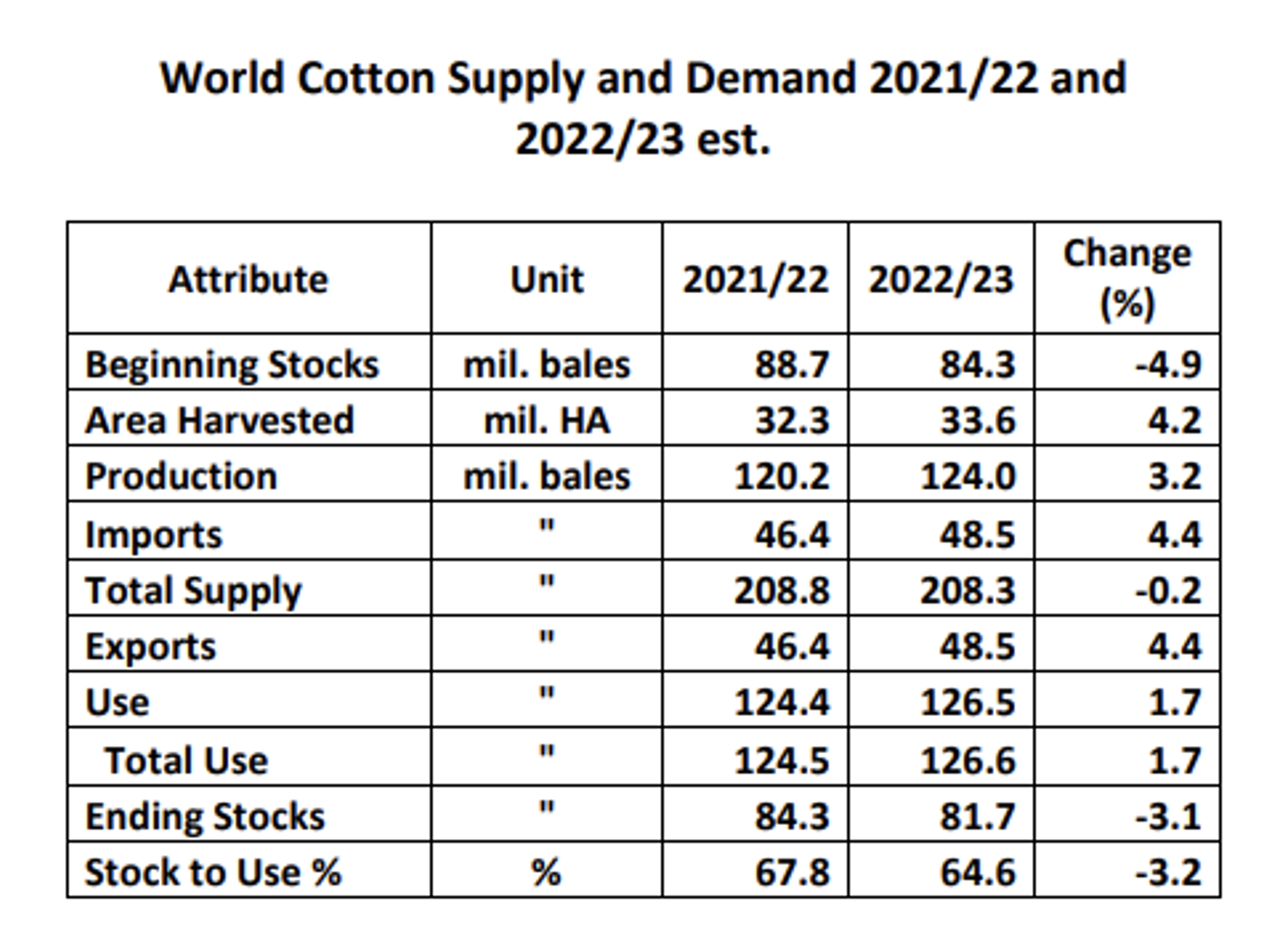

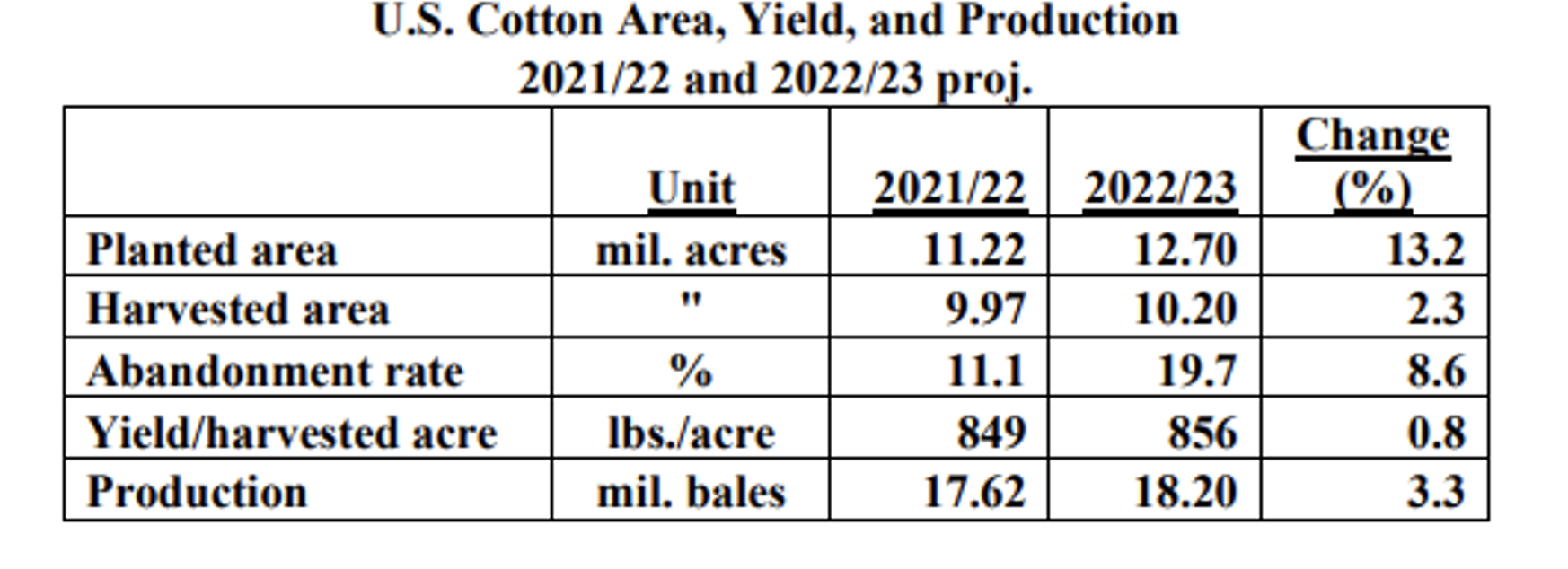

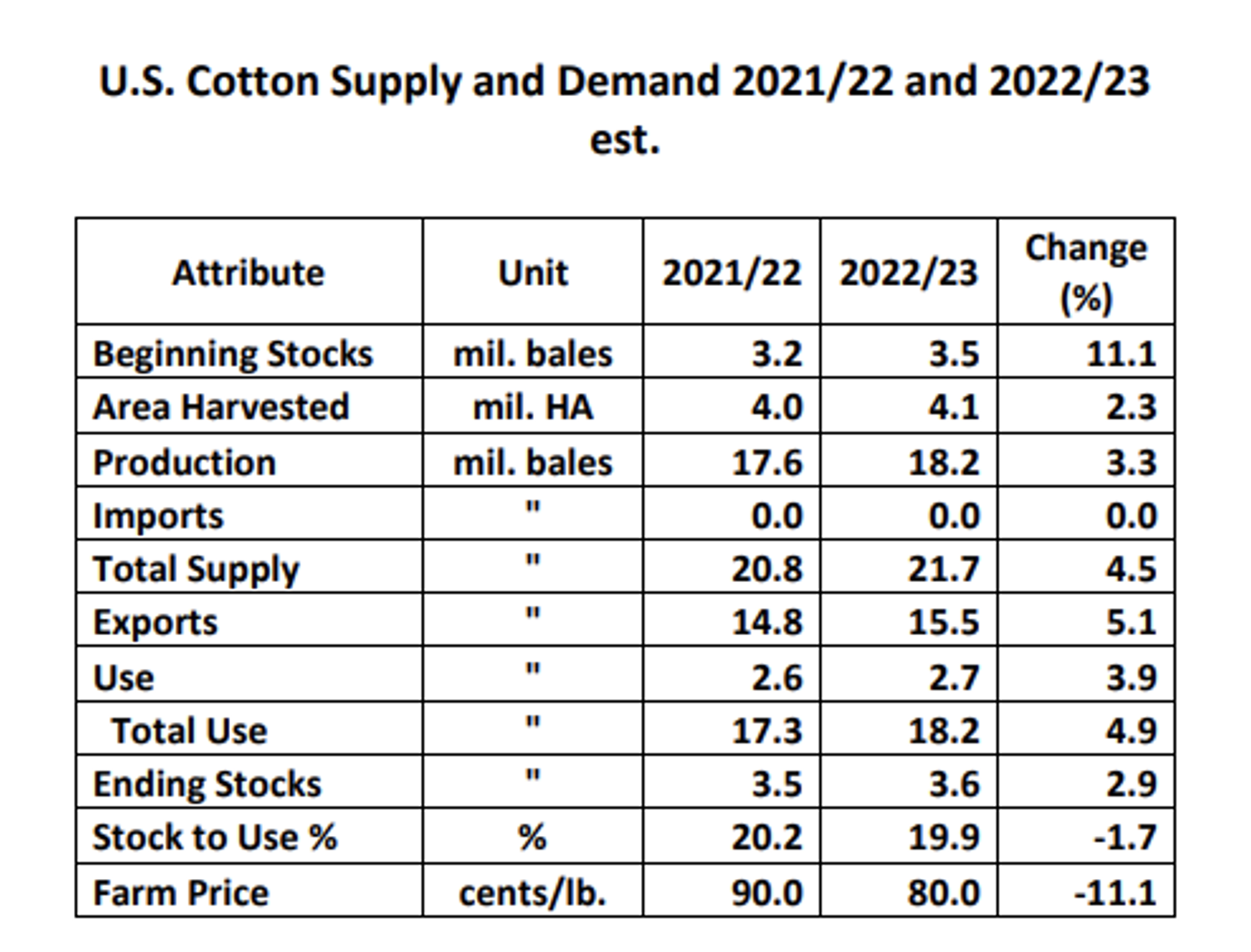

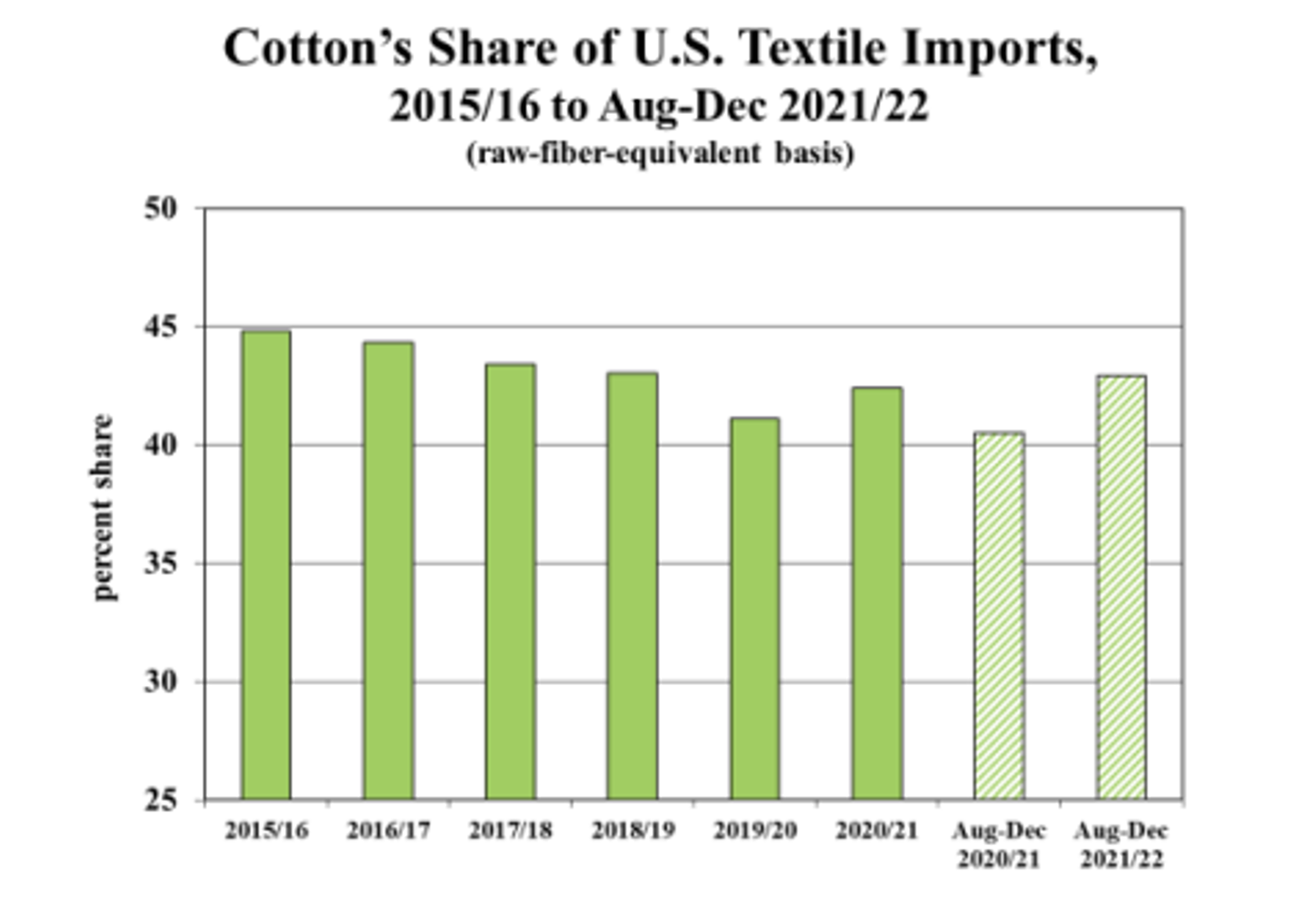

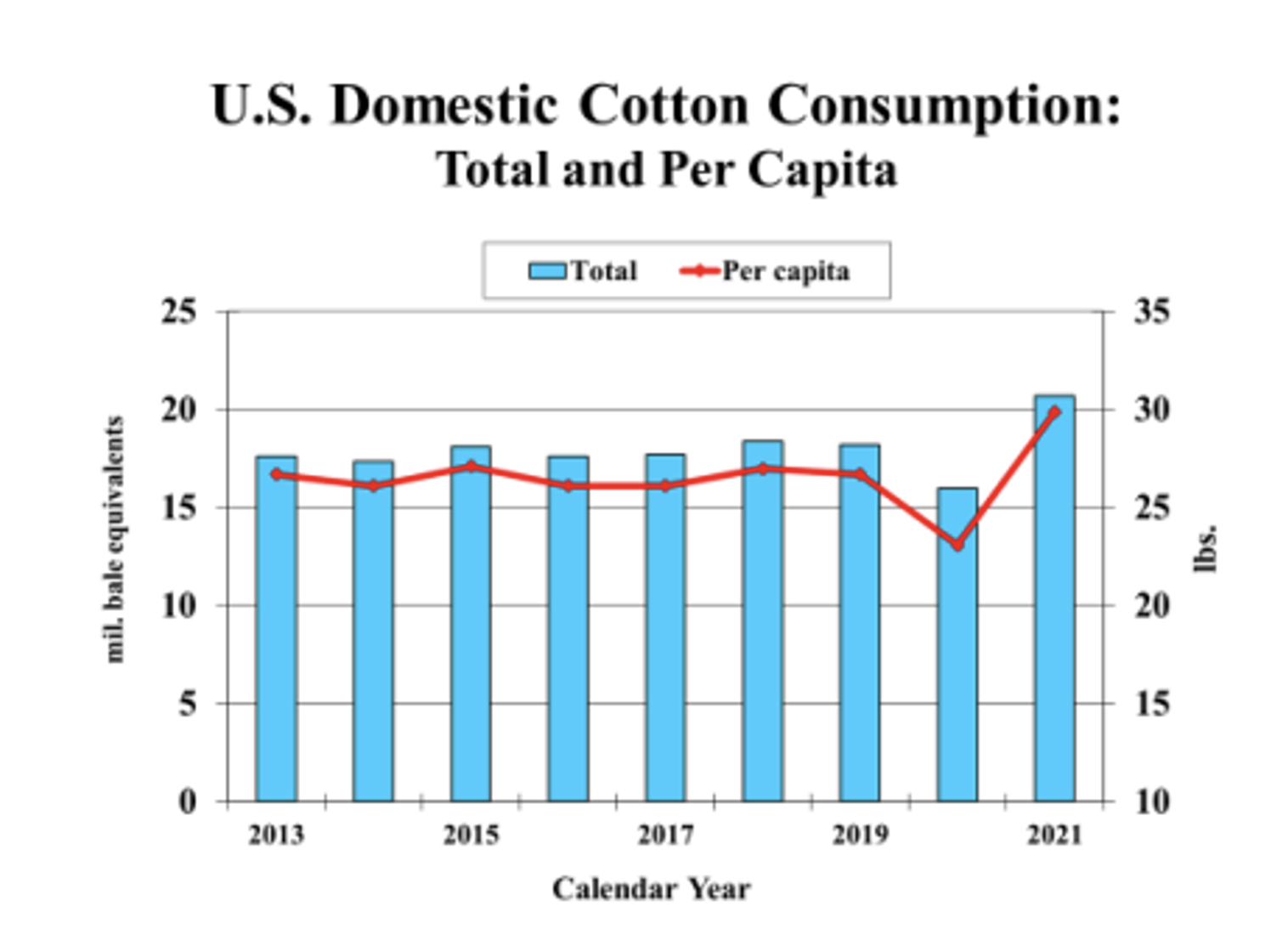

Beneath the rumble of jets and tanks, the cotton market got its first look at the USDA’s 2022/2023 cotton outlook this morning. In short, the USDA expects harvested acreage of cotton to increase 2% for a baseline crop forecast of 18.2 million bales. Planted acres are expected to increase 13% to 12.7 million acres, but the USDA wisely acknowledged that drought in the Southwest is likely to drive abandonment higher. With global consumption forecast at 126.5 million bales, the U.S. is expected to export 15.5 million bales and have 3.6 million bales of ending stocks. The USDA also noted that end-user, retail demand for cotton has surged to its highest level in years, as has cotton’s share of imported textiles’ fiber content. Select charts and tables from the Cotton Outlook are provided below.

Export Sales

The anticipation of war and continued high prices did not deter spinning mills from continuing to book more cotton from the United States last week. A broad range of 22 countries bought a total of 247,200 bales of Upland cotton for delivery this marketing year and 218,200 for delivery after August 1st. Pima sales were also healthy at 4,900 bales. The biggest buyers for the current marketing year were China (92,000 bales), Turkey (24,400), and Vietnam (19,700). Next year’s big buyers were Pakistan (94,700), Bangladesh (43,600), and Indonesia (30,800). To the delight of many traders, shipments have finally begun to pick up. Shippers declared exports of 376,100 Upland bales and 18,000 bales of Pima. The US has now committed more than 90% of the USDA’s export forecast, and supplies are tight.

Weather and New Crop Outlook

The storm fronts that have blown across the cotton belt in recent weeks have brought some relief to Central Texas and the Upper Coast, but West Texas hasn’t had enough precipitation to change anything. Nearly all of the High and Rolling Plains districts have topsoil and subsoil moisture readings that are “short” or “very short”. The precipitation outlook for the next few weeks is the same, unfortunately. West Texas may catch some precipitation from storms that sweep across the Cotton Belt, but it looks like the main benefit will be to Central Texas and eastward. Temperatures will be warmer next week. Additionally, cotton has lost a lot of competitiveness versus grains this week, and it is not clear that expected increases in the Mid-South and Southeast will be able to materialize.

The Week Ahead

Fallout from the conflict in Ukraine and sanctions on Russia are still being watched closely. Whether downstream demand holds up through the conflict and the Federal Reserve will adjust course on planned tightening, is still unknown. Export sales and forward crop prices will be the key data points for fundamental traders, but most traders will acknowledge that importance of fundamentals is at a low ebb.

In the Week Ahead:

- Friday at 2:30 p.m. Central – Commitments of Traders

- Thursday at 7:30 a.m. Central – Export Sales Report

- Thursday at 2:30 p.m. Central – Cotton-On-Call